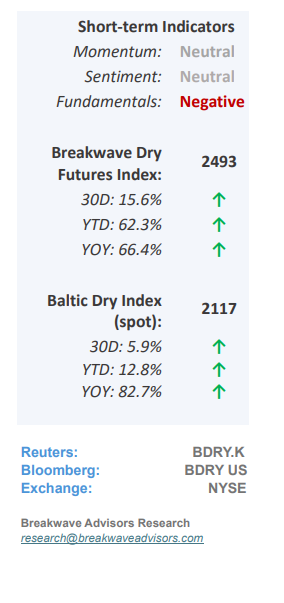

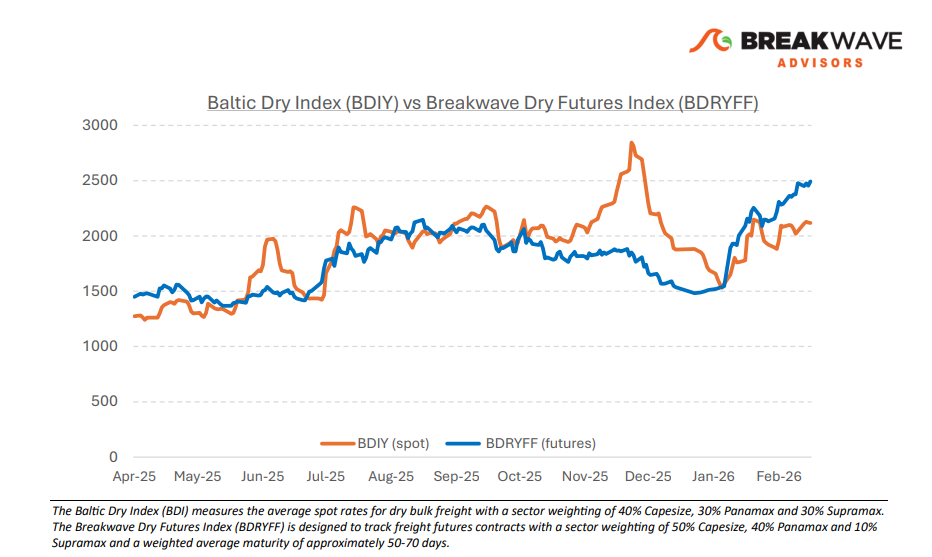

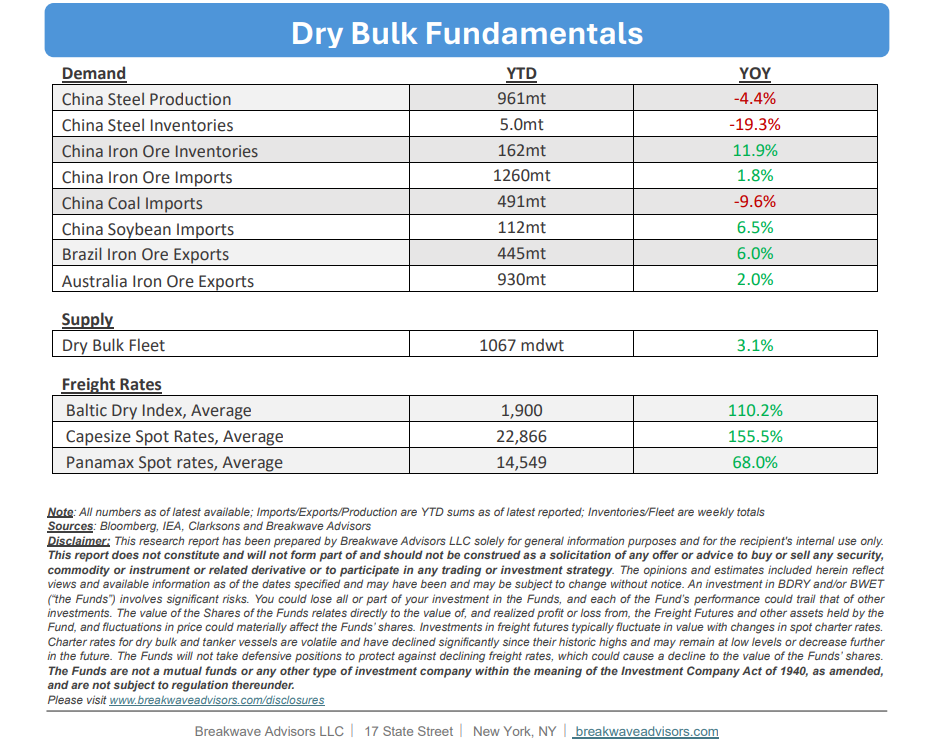

• Positive Sentiment Supports Rates Despite Dark Macro Clouds – The dry bulk chartering market has finally reached a phase of institutional maturity where freight derivatives increasingly dictate spot market trajectory, mirroring the evolution of other global commodity markets. With daily Forward Freight Agreement (FFA) volumes now exceeding physical transactions by several orders of magnitude, a predominantly bullish futures curve continues to anchor physical spot rates. This is a structural shift that has especially transformed Capesize chartering over the past decade. While the broader shipping industry is experiencing historic strength across multiple segments (especially tankers), this positive spillover has suppressed dry bulk spot rate volatility and allowed sentiment-driven futures to decouple from immediate physical realities that seem at best lukewarm to us. Such a development should be welcomed by the industry since it shows the transition of the sector to a mainstream commodity. However, such maturation also introduces the risk of a severe correction under particular circumstances; unlike past instances when dry bulk was isolated from broader economic headlines, should a macroeconomic shock occur, dry bulk's correlation with broader commodities will likely intensify, thus exposing the vulnerability of the underlying frail supply/demand balance. Despite weakening fundamentals, characterized by declining Chinese steel production, record-high iron ore inventories, and sluggish coal imports, the prevailing freight rate trend remains dominant. Consequently, the current divergence between bullish sentiment and lackluster physical demand will likely persist or maybe even intensify further until an external shock forces a market recalibration.

• Ample Iron Ore in China Amid Weakening Steel Sector Demand – Iron ore stockpiles in China have now reached a record 162 million tonnes, eclipsing the previous peak established in 2018. Despite this surplus and generally sluggish steel demand, prices remain resilient, hovering just below the $100/mt mark, stabilized by the centralized procurement strategies of the China Mineral Resources Group (CMRG). Much like its strategic management and increase of crude oil reserves, China’s continued aggressive acquisition of iron ore despite high inventories remains an enigma; however, this activity has so far provided a significant tailwind for the dry bulk shipping sector. While current iron ore prices may seem excessive relative to the cooling domestic steel market, CMRG’s oversight provides a stabilizing mechanism capable of maintaining price equilibrium for both domestic mills and global mining operators.

• Our Long-term View – The last few years have been characterized by increased geopolitical uncertainty. Going forward, we expect such events to continue to affect global trade and have a meaningful impact on effective vessel supply. Combined with the potential for a multi-year cyclical rebound in China’s economic activity following the recent economic turmoil, dry bulk shipping should experience higher volatility on top of a secular tightness driven by stable bulk commodity demand and a slower fleet growth owing to a relatively low orderbook.

Subscribe: