Two years ago, Doric Weekly Insight opened on a distinctly euphoric note, observing that the dry bulk market had concluded February at 2,111 points – a level last recorded during the same trading window in 2010. Twelve months later, the benchmark for bulk carrier activity ended the month at 1,229 points, having spent a considerable part of the first two trading months in three-digit territory. Over the past seventeen trading years, end-February readings above 1,000 points have been the exception rather than the rule, while prints north of the 2,000-point threshold have been extremely rare. In fact, setting aside the pandemic-distorted 2022 and the front-loaded rally of 2024, one must go back to 2010 to encounter a similarly firm seasonal starting point.

Against this historical backdrop, the opening phase of 2026 has been notably vivid. The Baltic Dry Index closed today at approximately 2,140 points, re-injecting a tangible sense of optimism into the market. By segment, Capesize led the advance, settling at $27,714 per day, up 34.7 percent year-on-year. The Panamax market followed with equal conviction, balancing at $17,481 per day, almost $8,000 higher than the last closing of February 2025. In a similar vein, Supramax and Handysize earnings, at $16,915 and $13,976 per day respectively, remained consistently supported throughout the month, standing $5,600 and $4,100 above year-ago levels. While a higher seasonal floor had been widely discussed across the market, the magnitude, breadth and persistence of the recovery were anticipated by very few.

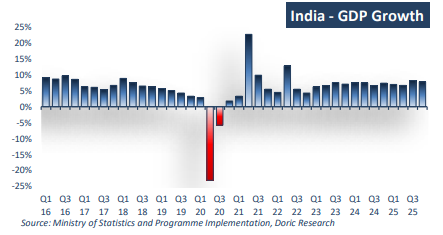

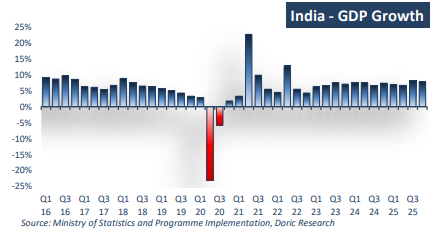

On the macroeconomic front, India dominated this week’s headlines, confirming its position as the fastest-growing major economy despite a modest sequential slowdown. GDP expanded by 7.8 percent in the October-December quarter, exceeding market expectations of 7.2 percent, while the previous quarter’s growth was revised to 8.4 percent under the new statistical series. The full-year growth estimate for FY 2025/26 has been raised to 7.6 percent from 7.4 percent, while projections for FY 2026/27 now stand in the 7.0-7.4 percent range, compared with the 6.8-7.2 percent previously indicated. The latest print follows a comprehensive overhaul of the national accounts framework aimed at improving accuracy and better capturing the evolving structure of the economy.

For much of the current financial year, India has had to contend with tariff-related uncertainty, which has weighed on exports and clouded the external outlook. In response, the administration of Prime Minister Narendra Modi accelerated domestic reforms, including the reduction of consumer taxes across a wide range of goods and renewed progress on long-delayed labour market changes, with the objective of strengthening the internal growth engine. Earlier this month, New Delhi reached an interim agreement with Washington that lowers effective tariffs to 18 percent, easing trade tensions, although the deal has yet to be formally signed. At the same time, the U.S. Supreme Court’s decision to strike down the previous global tariff regime could improve India’s negotiating position in the forthcoming round of discussions. Nevertheless, the announcement of a temporary 10 percent duty on all trading partners – with the prospect of an increase to 15 percent – serves as a reminder that the external environment remains fluid.

Private consumption continued to act as the principal driver of growth, expanding by 8.7 percent year-on-year in the OctoberDecember quarter, accelerating from 8.0 percent in the previous period, supported by festive demand, tax rationalisation measures and a gradual improvement in rural conditions. Government expenditure rose by 4.7 percent, moderating from 6.6 percent, while gross fixed capital formation increased by 7.8 percent, slightly below the 8.4 percent recorded previously, pointing to continued – albeit more measured – investment activity. Overall, domestic demand continues to display notable resilience despite a slower agricultural cycle.

On the supply side, manufacturing once again stood out, with gross value added rising by 13.3 percent year-on-year, marginally above the already strong 13.2 percent recorded in the prior quarter. The sector continues to benefit from robust domestic order books, capacity expansion and supply-chain diversification, while services activity – particularly financials and hospitality – remains firm. In contrast, agricultural growth slowed to 1.4 percent from 2.3 percent, highlighting the persistent divergence between the industrial and rural economy and reinforcing the increasingly urban and investment-driven nature of the country’s expansion.

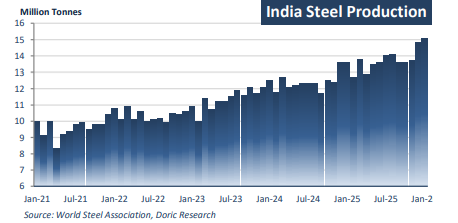

This double-digit industrial performance is increasingly reflected in the steel sector, where output continues to follow a structurally rising trajectory. India produced approximately 140-145 million tonnes of crude steel in FY 2024/25, with capacity expanding beyond 170 million tonnes, while utilisation rates at the major integrated mills have remained in the mid-80 percent range. Strong demand from infrastructure, construction and capital goods continues to provide a durable foundation for further growth, with finished steel consumption still recording high single-digit year-on-year gains. This dynamic underscores both the depth of the current industrial cycle and the visibility of further expansion over the medium term.

Whether India alone can sustain a broader upward trend in the freight market remains open to debate. Nevertheless, its consistent economic expansion, accelerating industrial base and rising steel production are becoming an increasingly important stabilising force within the global demand matrix, reshaping regional trade flows.

In this context, this February’s market levels remained comfortably above long-term seasonal averages, offering a clear degree of resilience. Ultimately, the trajectory of the market in the coming months will prove far more significant than the strength or weakness of its early-year performance, as the first quarter has rarely set the tone for the full year ahead. That said, the current sense of euphoria appears to be more deeply embedded in market psychology than in previous cycles and, provided that the macroeconomic backdrop remains broadly supportive, it carries the potential to extend well beyond the seasonal window and shape sentiment in the months to come.

Data source: Doric