The dry bulk market entered 2026 with remarkable momentum, delivering a broadly robust performance across all vessel classes in the first two months of the year. From Capesizes to Handysizes, spot rates trended higher on a year-on-year basis, supported by sustained strength even through the typically quieter Chinese New Year period.

By the end of February, sentiment had turned decisively bullish, with market participants projecting strong earnings across 2Q–4Q 2026. The corresponding futures contracts reflected this optimism: C5TC (basis 180K) FFA contracts were above $30,000/day, while the 2Q26 contract reached a record high of $33,136/day on 3 March.

This bullish trajectory, however, was abruptly disrupted following President Trump’s decision to intervene in the Middle East. In the aftermath, both spot and forward rates declined through March as the market shifted into a pronounced risk-off stance in the face of heightened uncertainty and confusion. In this 1Q26 recap, we provide a comprehensive assessment of the known implications of the ongoing Iran conflict on the outlook for the dry bulk sector.

Iran Conflict – A Systematic shock

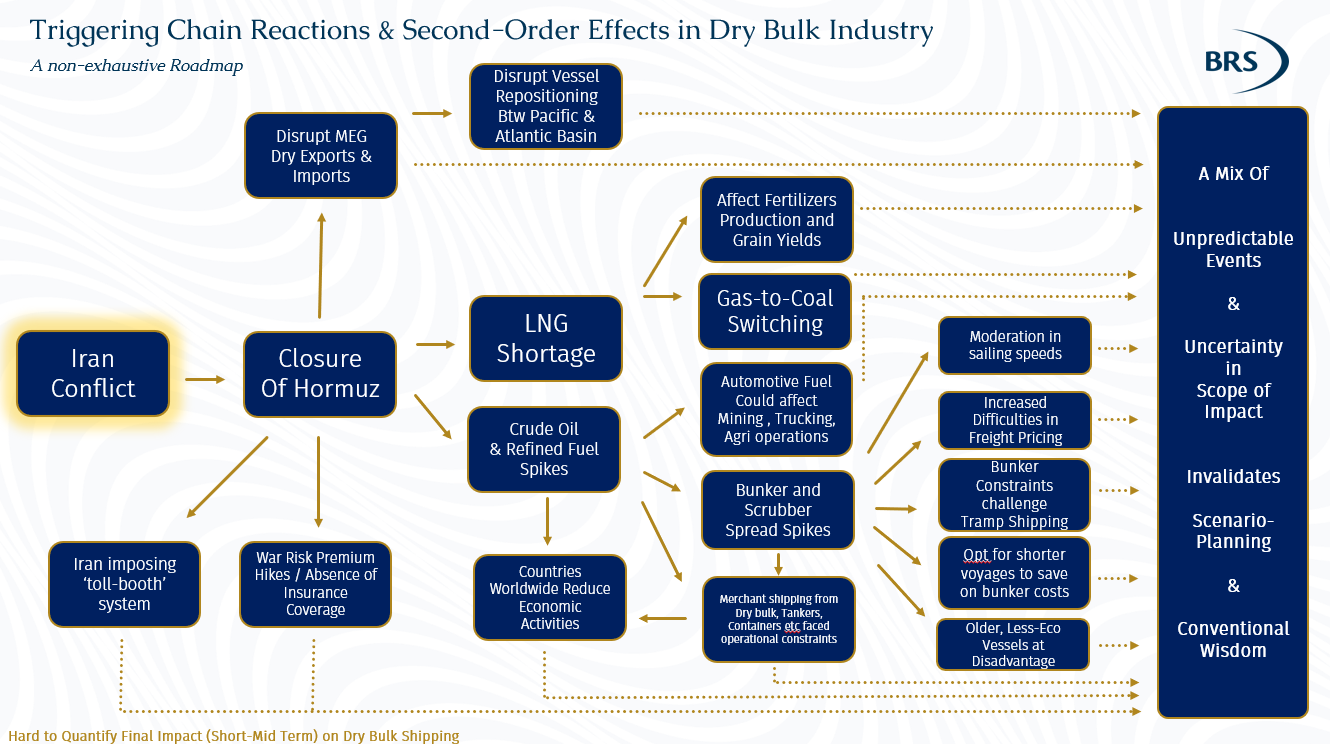

While the “Liberation Day” tariffs announced by President Trump on 2 April 2025 had a significant effect on market sentiment, the effective closure of the Strait of Hormuz represents a far more severe system shock. Its impact has rippled across shipping costs, energy availability, insurance markets, upstream cargo availability and downstream user demand, making it exceptionally difficult to quantify the final toll on the dry bulk sector.

This development illustrates how a localized security event can propagate into a multi-market shock as the dry bulk sector absorbs the consequences of the energy shock through both higher transport costs and downstream demand effects.

The first-order impacts are both operational and financial, with an effective closure stranding vessels and sharply reducing traffic, while shipowners face heightened crew safety and risk management challenges. Furthermore, war-risk underwriting quickly becomes a gating factor that places premiums for Hormuz passage in the mid-single digits (and higher) as a percentage of hull value.

At the time of writing, reports indicate that Iran’s Islamic Revolutionary Guard Corps (IRGC) has effectively established a de facto “toll booth” system in the Strait of Hormuz. Under this arrangement, vessels are required to submit comprehensive documentation, secure clearance codes, and transit through a designated corridor under IRGC escort. It is worth noting that the IRGC is designated as a Foreign Terrorist Organization (FTO) by the United States.

For dry bulk, besides the disruption done towards the Gulf’s exports and imports and its role as a repositioning hub, the most immediate transmission channel is bunkers and the volatility it injects into voyage economics whereby the bunkering cost can range from roughly one-third to more than half of operating costs, depending on routes and conditions. For instance, Singapore VLSFO benchmark prices more than doubled versus the February average, complicating quoting and fixture behavior by both shipowners and charterers, leading to a paralysis in negotiations as relevant stakeholders seek to attain consensus. As a side note, the sailing speeds of the fleet have slowed entering March which have the subtle impact of tightening tonnage availability.

On the commodity sales side, decisions around the allocation of freight responsibility - whether through FOB purchases or CFR sales - and the choice between time charter and voyage charter arrangements introduce additional layers of complexity. Indeed, as freight becomes a more significant portion of delivered cost, it may see market participants increasingly opt for shorter distance voyages, thereby clipping tonne miles.

Elevated bunker costs challenge the tramp shipping model, which fundamentally relies on the assumption that fuel is affordable and readily available at every corner of the earth. The current environment is also creating winners and losers. Fuel-efficient vessels and scrubber-fitted ships gain a structural advantage when VLSFO prices rise and spreads widen, while older, less efficient tonnage faces a significantly higher cost burden. However, as global sour crude supplies plunge, so the potential for 380 Cst supply shortages rise, which could eventually impact scrubber-fitted vessels.

Second-order effects are more ambiguous and are central to why forward visibility deteriorates. For example, LNG tanker traffic through Hormuz has been halted, disrupting roughly one-fifth of global LNG supply. In turn, the supply crunch and associated high prices, should trigger gas-to-coal switching from the Far East to Europe. In particular, across Japan, South Korea, and Taiwan China as this bloc is dependent on imported LNG. Last week, as an emergency measure, Japan proposed suspending for one year its 50% cap (to meet its decarbonization goals) on the capacity utilisation rate of coal-fired power plants with generation efficiency below 42%.

Another second-order pathway links energy disruption to fertilizers and grain. Ammonia production relies heavily on natural gas, with the IEA estimating that over 70% of output comes from gas-based steam reforming. According to the UN FAO, reduced fertilizer affordability poses downside risks to crop yields which should reshape global grain trade. Southern Hemisphere planting seasons - particularly in Brazil, Argentina, and Australia - could be affected later this year if fertilizer prices surge or supply declines. In the US, impacts are more nuanced. Rising nitrogen fertilizer costs are increasing corn production expenses, as corn depends heavily on nitrogen inputs like ammonia and urea. In contrast, soybeans require less nitrogen, as they fix their own, relying more on potassium and phosphorus instead.

Taking a step back, fuel shortages on land can disrupt upstream and inland activities - including mining, trucking, and agriculture (from extraction and processing to transport and harvesting). Any resulting supply chain bottlenecks can, in turn, dampen seaborne demand from gearless to geared units.

Lastly, there’s the hidden costs on overall macroeconomic activity. In the event of eventual bunker supply shortages, if the merchant fleet is unable, over a prolonged period, to provide reliable freight services in a timely and cost-effective manner, the drag on industrial activity will be inevitable. In a worst-case scenario, once factories and plants are forced to shut down because they cannot secure key raw materials, restarting them takes time.

The WTO has already warned that a prolonged conflict could clip global trade and growth in major economies that are dependent on oil imports. In particular, many Asian countries source the bulk of their oil from the Middle East and markets there are beginning to tighten. For instance, fast-growing dry bulk importers like India and Vietnam are cushioning consumers, by cutting fuel taxes to offset rising pump prices. Several Asian economies are revisiting pandemic-era measures such as reduced energy use and shorter work weeks. On the other hand, China’s reduced trade surplus with the US has made it increasingly reliant on exports, whether finished goods or raw materials, to the rest of the world to support its GDP growth. If this system shock proves detrimental to its trading partners, China’s economy will likely be implicated even with its formidable strategic oil reserves Beijing has built buffers the economy better than its Northeast Asian neighbours.

The scramble to secure oil and other critical commodities is driving a renewed wave of protectionism (negative for trade). China has curtailed transport fuel and fertilizer exports, Indonesia plans to impose export taxes on coal and nickel, and Vietnam is prioritizing domestic refineries for its crude. Each move aimed at safeguarding local supply but tightening global markets.Consequently, the net outcome for dry bulk demand is therefore not a single directional forecast but a widening distribution of plausible scenarios. A Hormuz shock “fogs” forward visibility because second-order effects arrive with lags, interact in non-linear ways, and can invalidate conventional baseline assumptions faster than the market can re-establish reliable benchmarks.

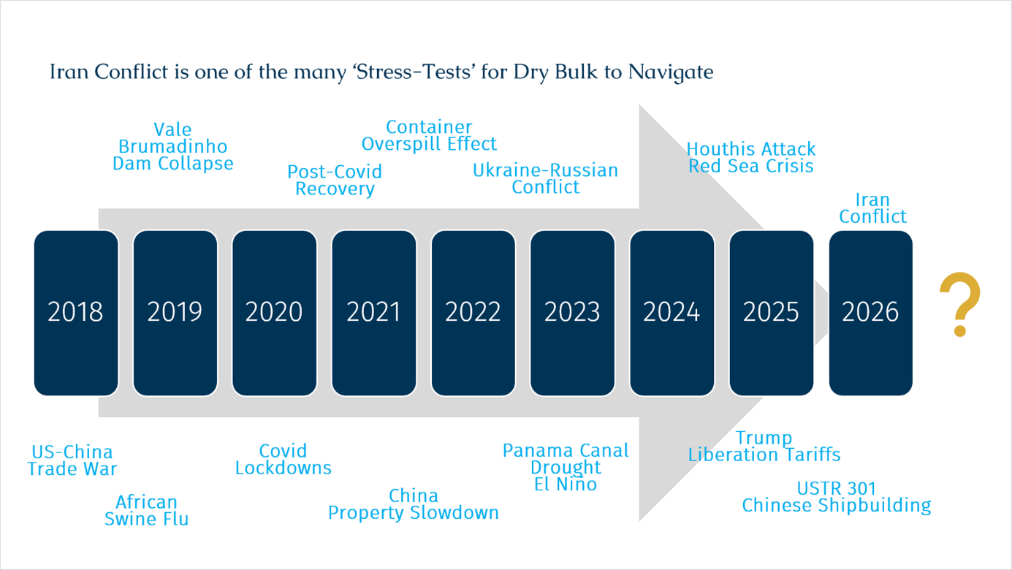

All said and done, the dry bulk market has repeatedly demonstrated resilience through a succession of global shocks - from trade wars and pandemics to geopolitical conflicts and supply chain disruptions - each reshaping demand, trade flows, and freight dynamics in different ways. From a long-term perspective, the ongoing Iran conflict represents the latest in this of stress tests. While uncertainty remains elevated, history suggests reinforcing the importance for market participants to remain adaptable to achieve a new equilibrium.