Iranian strikes on EGA and Alba, combined with the closure of the Strait of Hormuz, represent the most severe supply disruption since 2022. This week, Allied QuantumSea Research examines an alternative angle on the escalation in Hormuz, focusing on its implications for the aluminium industry.

Key Figures

• LME 3M prices are around $3,492/t, with an increase of roughly 6% at the start of the week, pointing to firm short-term momentum.

• Year-to-date performance shows gains in the ~30–35% range, with prices reaching a recent high near $3,545/t in mid-March, indicating a strong upward trend.

• Supply constraints are becoming more visible, with an estimated ~560 kt of capacity curtailed (approximately 8–9% of regional output), contributing to tighter market conditions.

• US all-in pricing is estimated to approach ~$5,000/t in tight conditions, with tariffs and elevated logistics costs driving a meaningful premium over global benchmarks.

Price Environment

Aluminium prices are back at levels last seen in 2022, during the last major period of market tightness. The current range of $3,300–3,492/t reflects pressures that were already building before this week’s escalation, with year-to-date gains of roughly 30–35% driven by steadily tightening fundamentals.

The forward curve tells the same story. Backwardation on the London Metal Exchange points to a market where the tightness is happening now, not something pushed into the future. At the same time, exchange inventories have been drawn down, leaving less of a buffer to absorb sudden shocks.

What’s driving prices at this stage isn’t just positioning — it’s the reality of constrained supply and disrupted trade flows. With less metal available and logistics under pressure, the physical market is doing most of the work.

In the US, tariffs and higher delivery costs are pushing all-in prices sharply higher, with levels in tight conditions moving toward $5,000/t. Physical premiums in both Europe and the United States have risen alongside this, highlighting the growing gap between exchange prices and what buyers have to pay to secure metal.

Supply Disruptions

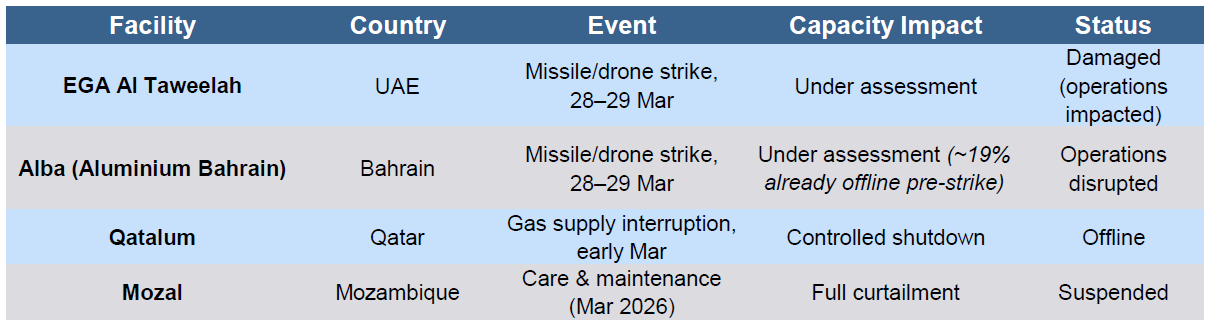

On 28–29 March, Iranian missile and drone strikes targeted two major aluminium smelting operations in the Gulf. Emirates Global Aluminium confirmed “significant damage” to its Al Taweelah site in Abu Dhabi, while Aluminium Bahrain reported that its facilities were also hit, with injuries sustained by workers at both sites. Iranian authorities, including the Islamic Revolutionary Guard Corps, claimed responsibility for the attacks. Full production losses remain under assessment.

Beyond the immediate disruption, additional curtailments were already in place across the system. Qatalum in Qatar had undertaken a controlled shutdown earlier in March due to gas supply interruptions, while Mozal in Mozambique remains under care and maintenance, with production suspended.

In aggregate, these disruptions point to a tightening supply backdrop, with a meaningful portion of regional capacity either offline or operating below normal levels. While the precise scale of production loss is still being quantified, the loss of operational flexibility across multiple assets is already contributing to tighter physical market conditions.

In aggregate, an estimated ~560,000 tonnes of annual capacity had already been curtailed prior to the latest escalation, equivalent to roughly 8–9% of regional output and around 1% of global primary supply. The UAE and Bahrain together supplied roughly 584,000 tonnes to US buyers in the first eleven months of 2025, accounting for around 20% of total import volumes. China’s production ceiling of ~45 million tonnes per year limits its ability to act as a swing supplier. While idle smelter restarts are theoretically possible at sustained elevated prices, any meaningful export response would take months to materialise.

Freight Market Impact

The geared handy and supramax segments are likely among the more exposed vessel classes, given their role in moving alumina and aluminium products from Gulf ports. With Gulf shipping severely disrupted, these vessels face repositioning challenges, idle time, and longer ballast legs. Container shipping also has direct exposure: finished and semi-finished aluminium products moving to the U.S. and Europe are subject to booking suspensions, rerouting, and war-risk surcharges. Hapag-Lloyd’s $1,500/TEU surcharge implies an added logistics cost of roughly $75/t for containerised aluminium ingot, assuming a payload of around 20 tonnes per container. Cape rerouting is extending voyage times and tightening effective vessel availability, while higher bunker costs add to the pressure. West Africa–China bauxite flows are relatively insulated from Hormuz because they bypass the Gulf, but inbound raw-material flows into Gulf refining and smelting systems remain exposed to disruption.

Forward Outlook

The near-term outlook depends on three interlocking variables. First, the full extent of damage at EGA and Alba has not yet been quantified, and restart timelines remain unclear. Second, the geopolitical path remains uncertain: Pakistan hosted de-escalation talks on 29 March with Egypt, Saudi Arabia, and Turkey, while Iran has allowed some Pakistani-flagged vessels through Hormuz, but a broader restoration of commercial navigation remains unresolved. Third, China still operates under a production ceiling of around 45 Mt/yr, which limits its ability to respond quickly with additional primary supply. According to Fastmarkets had already forecast a global primary aluminium deficit of about 360,000 tonnes in 2026 before this week’s escalation; the attacks on EGA and Alba have increased the risk of a larger shortfall if outages prove prolonged.

Data Source: Allied