Iran–U.S. Escalation | Strait of Hormuz Risk | Vessel Incidents | Kharg Island Exports | Alternatives | Oil & Freight Markets

As of 3 March 2026: Transit counts, casualty figures, and insurance notices are time-sensitive and subject to rapid revision.

From Risk Premium to Operational Constraint

The escalation involving the United States, Israel, and Iran has shifted the Strait of Hormuz from a recurring geopolitical risk into an operationally constrained maritime environment, with direct implications for crude and LNG scheduling, tanker availability, and war-risk insurance pricing.

In this analysis, Allied Quantumsea Research maps the situation as it stands today, recognizing that the operating picture is changing rapidly and that near-term conditions will be driven by security dynamics, insurance availability, and traffic-management constraints rather than by legal declarations alone.

Strait of Hormuz: What’s the Current Situation?

Official maritime guidance confirms that no formal legal closure of the Strait of Hormuz has been declared through recognized international maritime notification channels. While members of parliament have publicly referenced the possibility of restricting or closing transit, such political statements do not in themselves constitute a legally binding closure. VHF broadcasts or public announcements are not enforceable unless implemented through applicable domestic and international legal frameworks and formally promulgated through recognized maritime mechanisms.

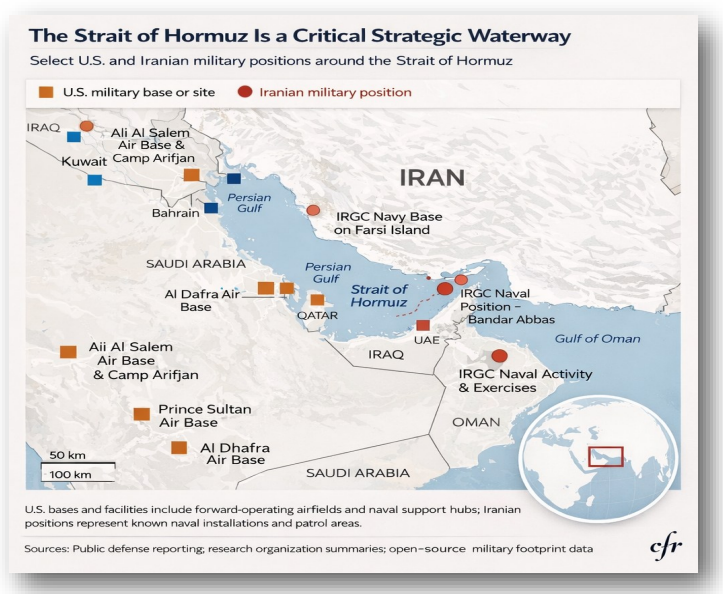

At the same time, the Joint Maritime Information Center has assessed the regional maritime risk level as Critical, citing active kinetic hazards, significant GNSS/GPS interference, and heightened security activity in and around the Strait.

AIS-based transit data reflects a marked fluctuation in vessel movements. JMIC reporting indicated that traffic fell “as low as approximately 28 vessels in a 24-hour period” in late February, compared with a historical average of roughly 138 vessels per 24 hours. A subsequent JMIC update recorded approximately 110 vessels in the past 24 hours, indicating partial normalization, though still below long -term averages.

In parallel, diplomatic statements from the China and several Gulf states, including the United Arab Emirates, Saudi Arabia, and Qatar, have emphasized the importance of maintaining freedom of navigation and ensuring the Strait remains secure and open to international shipping.

Commercial behavior is already reflecting practical constraints. War-risk capacity has tightened, and certain marine insurance providers have issued cancellation or amendment notices affecting specified Gulf and Iran-adjacent waters, including notices effective from 5 March 2026.

As a result, insurance availability and pricing may increasingly act as a determining factor in transit decisions, irrespective of the absence of any formally declared navigational closure.

Transit figures based on JMIC advisories and AIS aggregation; counts subject to rapid revision depending on reporting window.

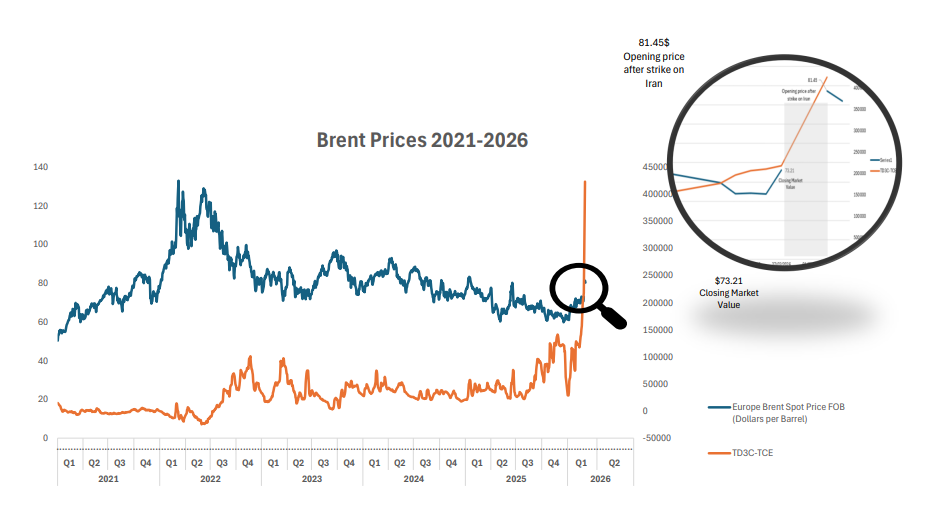

Oil Price Outlook and Scenarios

(As of 2 March 2026 – based on institutional market commentary)

• Base case (near-term disruption / partial restoration):

Market commentary from major financial institutions, including Citi, has suggested Brent could trade in an ~$80–$90/bbl range over the near term, with potential retracement toward ~$70/bbl in a de-escalation scenario.

• Disruption persists (flows not restored quickly):

Industry analysis, including commentary from Wood Mackenzie, has indicated Brent could exceed $100/bbl if tanker flows through the Strait are not restored promptly.

• Severe / prolonged impairment:

Strategists at JPMorgan and other institutions have referenced scenarios where a sustained blockage could push Brent above $100/bbl, with ~$120/bbl cited in more extreme, extended disruption cases.

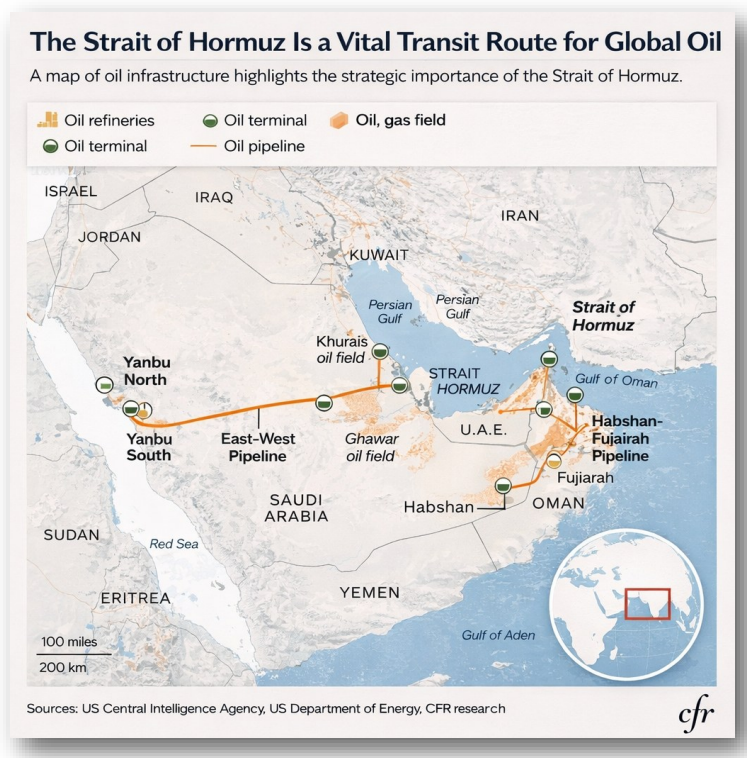

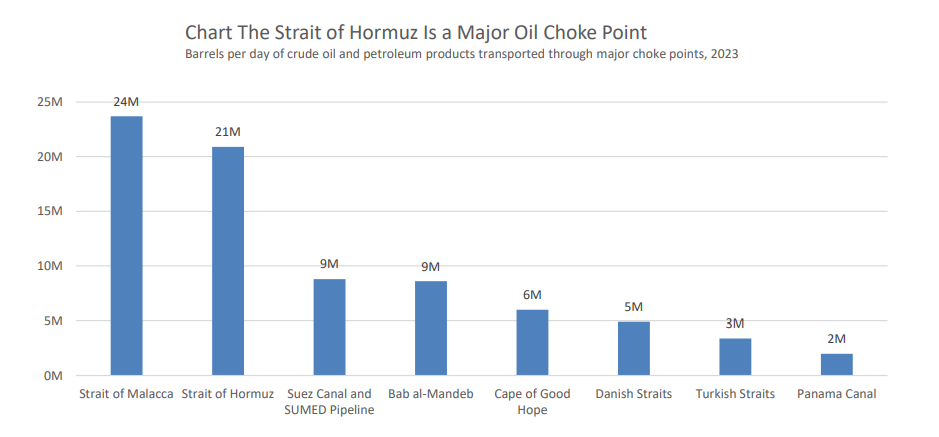

Why the Strait of Hormuz Remains Critical

The Strait of Hormuz is a narrow and geographically exposed corridor through which a large share of globally traded energy must pass. Council on Foreign Relations analysis, referencing U.S. Energy Information Administration (EIA) data, describes the Strait as a crucial chokepoint through which roughly one-fifth of globally traded crude oil and approximately one-quarter of global liquefied natural gas shipments transit. At its narrowest point, the waterway is about 21 miles wide and directly abuts southern Iran. The same assessment notes that Gulf exporters’ access to global markets could be materially constrained during a major regional conflict, which is the core reason that even partial constraints or short-duration disruptions transmit quickly into global pricing and delivered-cost volatility

The Council on Foreign Relations further notes that escalating U.S.–Iran tensions in February 2026 coincided with Iranian live-fire naval exercises and temporary navigation restrictions in or near the Strait. This episode emphasized how disruption need not take the form of a sustained blockade to roil markets. Even short-lived closures, military exercises, or calibrated acts of coercive signalling can inject uncertainty into energy flows.

Maritime Operating Picture — Functional Disruption Without Formal Legal Closure

Operational disruption has emerged despite the absence of any universally recognized, formally communicated suspension of traffic by maritime authorities. Publicly available data indicated that approximately 150 vessels, including crude and LNG tankers, were anchored in Gulf waters beyond the Strait of Hormuz, with additional vessels stationary on the opposite side of the chokepoint and along the UAE and Omani coastlines (counts reflect reporting as of 2–3 March 2026 and are subject to rapid change).

Multiple tanker owners, oil majors, and trading houses suspended shipments through the strait following attacks and public statements by Iranian officials referencing possible targeting of vessels and potential restrictions on navigation in the area. U.S. Central Command, however, stated that the Strait of Hormuz remains open and has not been closed, despite those statements by Iranian authorities.

The Joint Maritime Information Center has advised that no formally recognized international suspension of transit had been communicated as of its latest update, while warning mariners to expect heightened naval activity, congestion near anchorages, and increased insurance volatility.

Security Signalling

The BIMCO Chief Safety and Security Officer has publicly warned that the recent U.S./Israeli strike on Iran materially increases security risk for vessels operating in the Persian Gulf and adjacent waters. He noted that ships with business connections to U.S. or Israeli interests may face heightened exposure, while cautioning that other vessels could also be affected, whether deliberately or inadvertently. Reporting by Lloyd's List indicates that BIMCO expects shipping insurance costs to rise significantly, with war-risk capacity tightening and coverage potentially subject to more restrictive underwriting in certain cases.

Iran’s Export Dynamics Pre Escalation

Crude loadings from Iran’s primary export terminal increased materially during mid-February relative to the prior month, reaching levels equivalent to more than 3 million barrels per day over a concentrated loading window. The acceleration in exports occurred in the days preceding heightened military activity and maritime disruption in the Gulf. While direct causality cannot be established, the sequencing is consistent with precautionary export acceleration during periods of rising geopolitical risk.

Alternatives — Limited Bypass Capacity and Incomplete Substitution

The serious constraint underpinning forward scenarios is limited substitutability.

While some Gulf producers maintain pipeline infrastructure that can partially bypass transit through the Strait of Hormuz, most notably Saudi Arabia’s East–West (Petroline) pipeline to the Red Sea and the UAE’s Abu Dhabi Crude Oil Pipeline to Fujairah, available bypass capacity remains significantly below total seaborne export volumes that typically transit the Strait. Analysis by the Council on Foreign Relations notes that countries dependent on unimpeded passage through the Strait would face significant export disruption in the event of a major regional conflict.

Takeaway

Maritime traffic through the Strait is continuing under heightened risk conditions. War-risk insurance premiums have increased, anchored vessel counts remain elevated, and some operators are adjusting transit timing as a precaution following recent security incidents. Spot tanker rates have risen sharply to levels comparable with previous geopolitical stress periods, reflecting uncertainty around voyage execution rather than confirmed supply disruption.

At present, commercial flows remain active, though at higher cost and with greater operational caution. Historical episodes, including the tanker attacks during the Iran–Iraq War and the 2019 Gulf incidents, show that shipping and energy markets can operate under significant strain, even as freight volatility and risk premiums remain elevated while uncertainty persists.

Sources: Joint Maritime Information Center (JMIC), Council on Foreign Relations analysis referencing U.S. Energy Information Administration data, Lloyd’s List reporting, institutional market commentary (Citi, JPMorgan, Wood Mackenzie), and publicly available ship-tracking data as of 3 March 2026.

Disclaimer: This material is for informational purposes. Forward-looking statements reflect publicly available information as of 3 March 2026 and are subject to change.

Data Source: Allied