Of all countries whose crude oil supply is put at risk by the closure of the Strait of Hormuz, India is probably the most exposed. To what extent does the US intervention to relax its sanctions on Russian exports relieve the pressure?

In February, before Iran started disrupting ships passing through the Strait of Hormuz, India imported 2.81m b/d from suppliers within the ME Gulf (54% of its total imports). That supply has now all but dried up. Opening access to Russian crude oil from sanctioned producers and Russian crude loaded onto OFAC sanctioned tankers before March 5, as the US did last week, looks likely to have given India access to ~65m bbls of Russian crude that was previously off limits. We estimate that this would compensate Indian refiners for the loss of 23 days-worth of ME Gulf crude exports.

Our 23 day estimate assumes all Russian crude cargoes loaded prior March 5 _ that before March 5th were signalling a discharge somewhere other than India - will now head to India, apart from those signalling Turkey and those already at or near berths in China. This includes all Russian bbls in floating storage and in transit. We make no allowance for Indian imports on OFAC sanctioned ships of Russian crude that loaded AFTER March 5, but where the documentation claims it was lifted before March 5th – something we haven’t ruled out.

We estimate about 65 million additional bbls of Russian crude already on board tankers could well end up in India over the next few weeks. This figure includes:

8m bbls of Russian crude in transit since March 5, irrespective of when it loaded, that WAS showing a ‘predicted destination’ (Vortexa) of somewhere other than India, and is NOW signalling destination India.

49m bbls of Russian crude oil lifted before March 5 currently in transit with ‘predicted destination’ currently suggesting heading for East Asia. Of these bbls, 25m have loaded in Western Russia but have yet to pass India and are therefore prime candidates for Indian discharge. The remaining 24m bbls of Russian crude barrels have either already passed India on their way East or have loaded in Eastern Russia prior to March 5 but not yet discharged.

7.6 million barrels of Russian crude oil that is currently sitting in floating storage (mostly Suezmaxes and Aframaxes in East Asia).

Removing restrictions on OFAC sanctioned tankers means India can access about 35m bbls faster than if they had to charter their own ships to move it.

Since the US announcement, two VLCCs and seven Aframax-sized vessels loaded with Russian crude have diverted from their voyages to East Asia and are now signalling for India, while one diverted Suezmax already discharged. One Aframax turned around just as it was approaching Dongjiakou. There are, however, reports that Indian central banks are nervous to work with Russian sellers, despite the temporary OFAC licence.

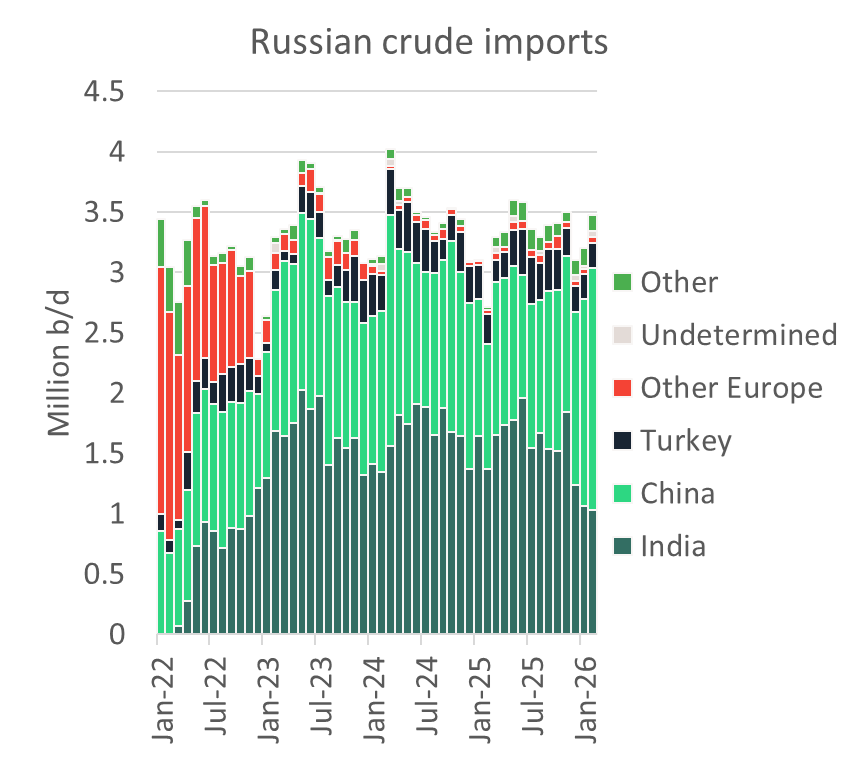

Before the US relaxed its rules, China had emerged as the main market for Russian crude. In February China imported 2m b/d of Russian crude, up from 1.3m b/d prior to the US sanctioning of Russia’s main exporters in October. India’s imports of Russian crude shrank from 1.52m b/d to just over 1m b/d over the same period. China’s 2m b/d of Russian imports are now likely to end up in India as it loses the bidding war for Russian crude - even crude originating from Russia’s East coast. For now, Shandong’s independent refiners – the only outlet for Russian crude in China – can tap into the ~160m bbls of Iranian crude on the water (~20m bbls of which is floating storage), and a trickle of Iranian oil still coming out of the ME Gulf. Iran’s exports in the month leading up to the conflict reached a nearly eight-year high of 2.23mb/d.

Source: Vortexa

India has increased its dependence on Mideastern crude since the US sanctioned Rosneft/Lukoil. More recently, the US-India trade deal and the EU’s ban on CPP refined with Russian crude (from January 21) cemented India’s vulnerability to the Strait of Hormuz. India’s crude stocks (onshore + SPR) provide around 30 days of import coverage. In comparison, China is estimated to have upwards of 130 days of import coverage.

Has India lost its entire 2.81m b/d from ME Gulf?

Since the SoH disruptions, a small volume of Saudi oil has found its way to India via Saudi’s East/West pipeline to the Red Sea port of Yanbu. As of today, one VLCC and one Aframax is moving cargo from Yanbu to India. In addition we have seen three VLCC fixtures, three Suezmax fixtures and one Aframax fixture Yanbu/India that have not yet loaded. Other VLCC fixtures from Yanbu have East options, so could go to India.

Is more US sanctions relaxation on the cards?

Treasury Secretary Scott Bessant said last Friday that more Russian oil could be unsanctioned. Trump reiterated this week that more sanctions relief could be on the cards, but no details have been forthcoming.

India was already bringing in around 1m b/d from Russia, mostly on vessels that were sanctioned by UK or EU, though not on vessels sanctioned by the US. This flow should continue regardless of the temporary US sanctions relaxation.