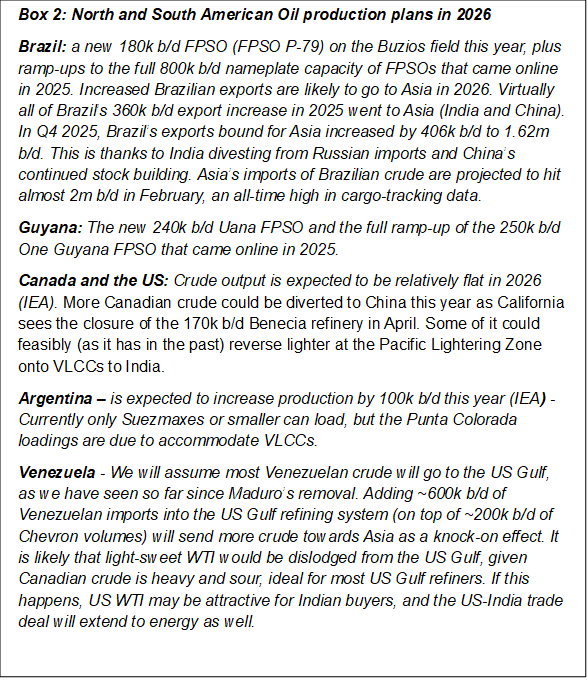

Will India-US trade deal support the large tanker market?

On Monday Trump cut India’s tariffs on exports to the US from 50% to 18%. Trump stated that Modi, for his part, had agreed to stop his country’s refiners buying Russian oil. We’ve yet to get confirmation from either India or Russia on the matter, but if this turns out to be true, we see this as a bullish development for compliant shipping generally, and VLCCs and Suezmaxes specifically. India’s crude imports would continue their shift away from (mostly older) Aframaxes loaded with Urals, potentially to longer-haul VLCC and Suezmax trades from the Atlantic Basin. But much depends on which countries pick up the slack.

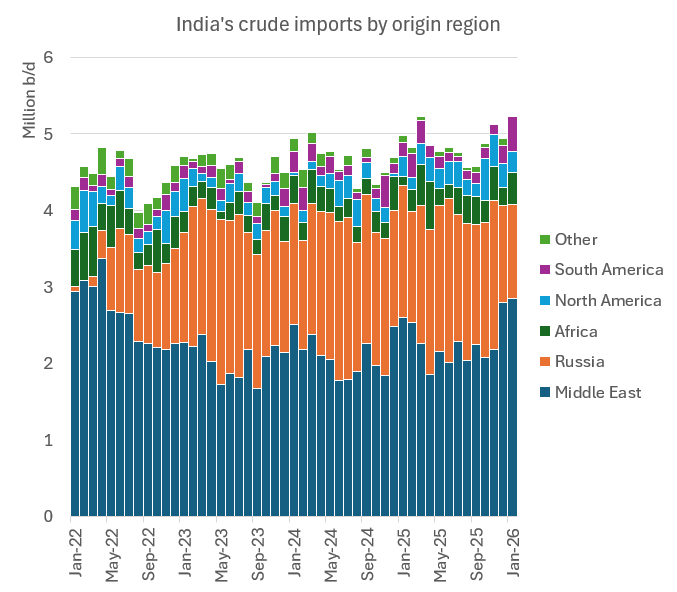

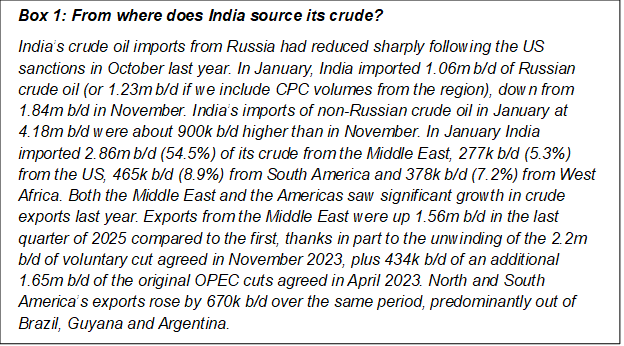

Since last October India has been a key growth market for compliant oil from both the Middle East and the Atlantic. The replacement of Russian crude imports lost to sanctions has been shared almost evenly between the Middle East and South America. While Russia’s (incl. CPC) share of India’s imports fell by nearly 13 percentage-points between Q3 2025 and January 2026, the Middle East’s share of Indian imports grew by 7.2 percentage-points (mostly increases from Saudi Arabia, Qatar and Iraq), while Latin America’s grew by 6.6 percentage-points (mostly from Brazil – compensating for declining volumes from the US after a post-tariff surge in October last year).

Source: Vortexa. Volume from Russia includes CPC blend.

In theory we could now see India drop a further 1m b/d of Russia crude imports. This assumes the EU/UK sanctioned Nayara stops taking approx. 400k b/d of Russian crude (for which no obvious alternative sources are available). If the slack was once again picked up in roughly equal measure by the Middle East and South America, and allowing for the growth in India oil imports since Q3 2025 averages, this could see an extra 520k b/d arriving from the Mid East, and 480k b/d from South America.

This time Latin America may have to share some of those gains with the US. Trump stated on Truth Social that Modi had agreed “to buy much from the United States and, potentially, Venezuela”. Last Thursday, the US sanctioning body OFAC lifted most restrictions on who could buy Venezuelan crude.

If that 500k b/d of extra crude oil to India (50% of the 1m b/d gain) is shared equally between the US and Latin America this could double the number of VLCC liftings to around 8 per month out of the USG, and to about 9 per month out of Latin America. The 500k b/d extra crude to India from the Middle East (the other half of the 1m b/d gain) would lift VLCC-‘equivalent’ liftings (in reality MEG to India volumes are 62% VLCC, 35% Suezmaxes) by 9 per month to around 32 per month. Given the respective voyage lengths this would require an extra 13 VLCCs to service the new US trade, another 9 to service South America and an additional 4 to service the Middle East.

However, it could be that Latin America’s could eat into the Middle East’s share. This year Latin America will add 600k b/d to its oil production (Brazil +300k b/d, Argentina +100k b/d, Guyana +180 k b/d) according to the IEA, not far shy of the growth it expects to see in global oil demand. If there are no supply changes elsewhere, Middle Eastern exporters are likely to give ground to accommodate Latin America’s increase. However, the recent abundance of medium and heavy sour crudes resulting from OPEC’s reversal of cuts last year has increased the competitiveness of Middle East’s generally heavier grades versus Brazil’s mostly medium sweet crude.

If this competitiveness allowed the Middle East to make up 80% of India’s shortage of Russian bbls, this might require an extra 7 VLCCs for Middle East/India, 6 for US/India and 4 for Latin America to India.

The case for the Middle East

If the Indian market now needs to replace its remaining Russian crude imports, the Middle Eastern will be gunning to fill the gap.

OPEC has reluctantly paused its unwinding of cuts from January as evidence mounts that weak demand growth is forcing oil into stocks. Until this US/India deal, analysts broadly expected the group to extend their freeze on production cuts, or even increase cuts beyond March.

For India, the Middle East has a shorter supply chain in its favour compared to the Americas. At today’s freight rates, that matters. A voyage from the Middle East to India is roughly 35 days shorter than from the US Gulf and at today’s rates between $9m and $11m cheaper depending on which side of India it discharges.

The case for the Americas

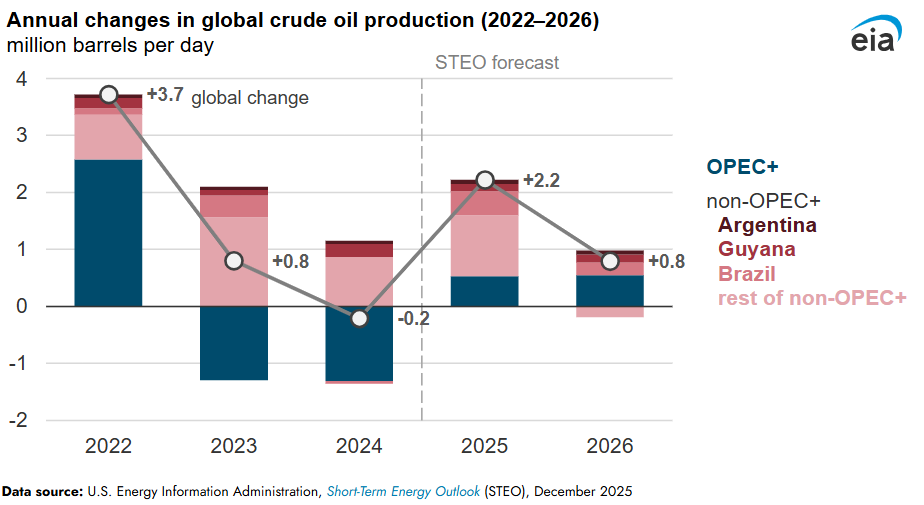

Following a huge increase in oil production (including NGLs) last year, both North and South America are expecting to lift production significantly again this year. The Americas accounted for three quarters of global oil production growth last year, and this year are expected to account for around 40% of all growth, according to the IEA. North American oil production grew 900k b/d in 2025 and is expected to grow by another 300k b/d this year, though only 110k b/d of that will be crude oil. Latin America will continue last year’s growth rate of +600k b/d, driven by Brazil, Guyana and Argentina.

In 2025, Guyana’s crude exports were 717k b/d in 2025 (+106k b/d yoy), Brazil’s were 2.04m b/d (+360k b/d yoy), Canada’s were ~764k b/d (+250k b/d yoy) and Argentina’s were 204k b/d (+84k b/d). The US exported ~3.65m b/d of crude oil, a small y-o-y decline of 191k b/d. About 40% of North and South America’s crude exports went to Asia last year, up from 35% in 2024.

Given the benefit of economies of scale on long-hauls to India, VLCC ability to load in Guyana and Argentina will be the limiting factor. Since Guyana’s crude exports started in 2020, VLCC liftings have generally been restricted in Guyana from late-autumn through January each year thanks to high waves. During that period Suezmaxes traditionally loaded all cargoes, and they tend to stay in the Atlantic. However, in Q4 of 2025, seven VLCCs moved Guyanese crude to Asia. Argentina only recently started loading Suezmaxes at Puerto Rosales last August, before which all exports were limited to Aframax and Panamax. Argentina’s VMSO pipeline to a new deepwater port at Punta Colorado will add180k b/d of export capacity in late 2026, rising to 550k b/d in 2027. This comes on the heels of the Puerto Rosales expansion in 2025, which saw exports increase by nearly 150k b/d.

Trump’s announcement leaves several questions unanswered. Is the Indian government now going to restrict the 647k b/d of Russian crude imported by state-owned refiners in January? Where does this leave the EU/UK-sanctioned Nayara refinery, which is solely reliant on Russian crude (circa 400k b/d of Russia imports)? Will the Indian government insist on full compliance by its private refiners other than Nayara? Reliance and HMEL have already cut their Russian crude imports to zero in January following Europe’s Jan 21st ban on CPP refined from Russian crude oil. Commentators have expressed some scepticism that India would stop all Russian imports. They have suggested that the US-India deal could be more about pressuring Russia than a real desire to end India-bound Russian flows.

Nevertheless, while any import restrictions remain in place, a battle is shaping up between the Americas and the Middle East for market share in India. Compliant tankers should benefit. The question is the extent to which average haul length rises, and which ship sizes will be favoured.