The EU is considering a major change to its sanctions framework on Russian oil. As reported on the 6th of February, the upcoming 20th sanctions package proposes a full ban on maritime services for Russian crude oil. This would cover shipping, insurance, brokerage, and finance and would fully replace the current price cap mechanism. Under this approach, European shipping companies would be barred from carrying Russian crude regardless of the price at which it is sold. The proposal is limited to crude oil only and does not currently include refined products such as fuel oil or clean petroleum products. UK sanctions are expected to follow the EU’s approach, which would effectively shut Russian crude out of the mainstream tanker market.

Adoption is provisionally targeted for late February but requires unanimous approval. The EU also strongly prefers to align with the G7 before moving ahead with the ban. Internally, Greece and Malta are reported to be the main holdouts, citing concerns over shipping and energy impacts and asking for further clarity on enforcement. On the other hand, some EU member states are concerned that delays to implementation would simply give Russia more time to acquire additional vessels and expand its dark fleet.

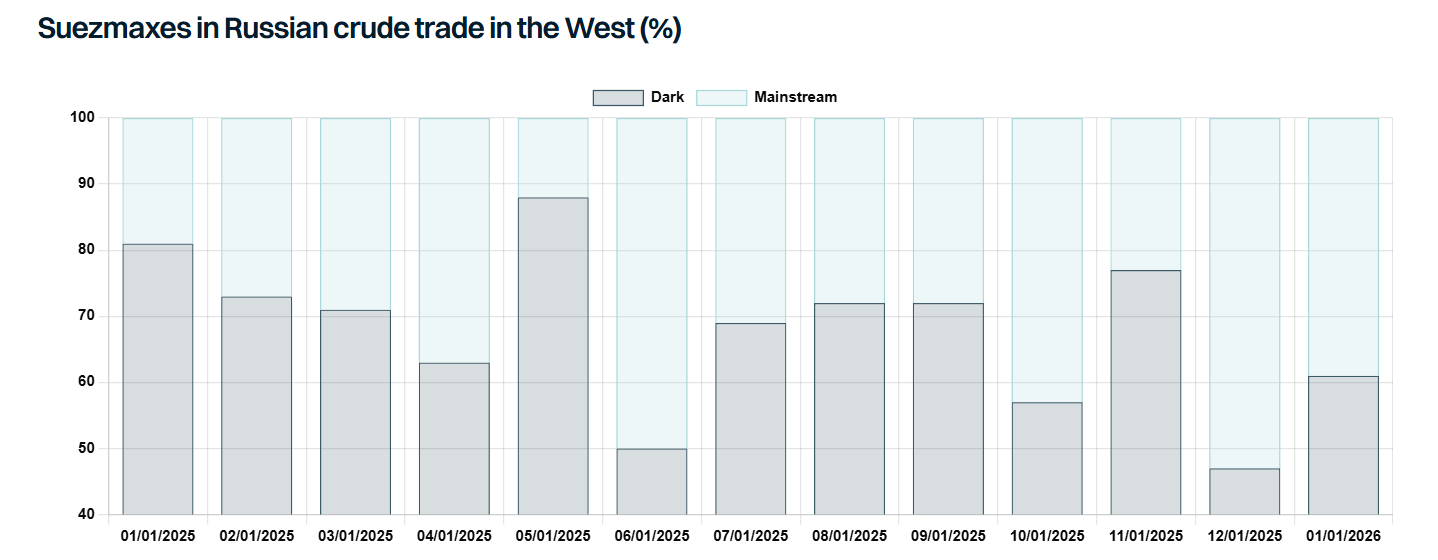

For crude tankers, Russia’s dependence on mainstream tonnage is already limited, with the main exposure sitting in the Suezmax segment. If a full maritime services ban is implemented, around ten Aframaxes and roughly fourteen Suezmaxes that typically load Russian crude in Western ports each month would be pushed back into the mainstream market. However, the return of these ships will have an outsized impact as Russian voyages to India and China are much longer than the typical mainstream trades for these size groups.

Timing of actual implementation will be key. Any delays increase the risk that Russia buys more secondhand tonnage, supporting prices for older Aframaxes and Suezmaxes. The upward pressure is already visible, especially for Suezmaxes, where values for 15‑year‑old ships have appreciated by 17.5% over the past six months. Still, operational risks are rising. Recent vessel detentions by the US and France highlight the growing risk of tanker seizures.

Faced with a ban, Russia will continue prioritising shipments from Eastern terminals, which are closest to China and already running at their maximum capacity. Western crude exports could weaken, although much will depend on Russia’s ability to redeploy dark Suezmaxes and potentially VLCCs previously active in Venezuela’s trade. While VLCCs are currently very rarely used for Russian exports, shortages of Aframax and Suezmax tonnage could lead to more ship-to-ship transfers into VLCCs, whether in the North Atlantic, Mediterranean, or even East of Suez.

Trade flows could also feel the impact, particularly as this comes against the backdrop of declining Russian crude sales into India, a trend discussed in our report last week. If the ban is implemented without any delays, it will limit Russia’s ability to redirect these barrels into China at least temporarily. It may also support short‑haul demand into the Middle East for power generation, although these flows are likely to be limited.

As the proposed ban applies to crude only, Russia has a clear incentive to push more product for export instead. That said, gains may be limited by Ukrainian drone attacks on refineries and the EU’s plans to sanction a number of Russian refineries.

On the clean side, Russian product exports are not currently included in the proposed maritime services ban. This is an important distinction. Any move to extend the ban to products would have a much larger impact on tanker markets. Russia relies far more heavily on mainstream tonnage for its product exports, with more than 50% of its shipments carried by mainstream tankers. A maritime services ban targeting these flows would almost certainly reduce export volumes materially. With limited new refining capacity coming online this year, global refining runs increasing by 800kbd and demand growing by 800-900kbd by the most conservative estimates, the global refining system is unlikely to be able to cope with any substantial cut in Russian product supply.

Data source: Gibson Shipbrokers