In the second week of February last year, Doric’s Weekly Insight focused on the abrupt escalation in global trade tensions following the announcement by U.S. President of a sweeping 25 percent tariff on steel and aluminium imports, targeting approximately 50 billion dollars of trade. The measure was set to affect a broad range of suppliers, with Canada, Brazil and Mexico accounting for nearly half of U.S. steel imports in 2024, while South Korea, Vietnam, Japan, Germany, Taiwan and China provided a further 30 percent. In aluminium, Canada alone represented close to 40 percent of U.S. import volumes, followed by the United Arab Emirates, China, South Korea and Bahrain. At the time, the escalation in trade frictions raised significant concerns about retaliatory measures and the potential disruption of global commodity flows, with direct implications for dry bulk demand. Although China’s steel exports to the U.S. were limited – just 508,000 tonnes, or 1.8 percent of total American imports – the broader risk centred on a possible domino effect of protectionist policies. Such a development would have undermined China’s competitive position in third markets, particularly as its steel exports had surged to 110.72 million tonnes in 2024, the highest level since 2015. This export strength coincided with a 1.7 percent year-on-year decline in crude steel production to 1.005 billion tonnes, reinforcing expectations that output had reached its structural peak.

Twelve months later, the policy landscape appears to be shifting. According to the Financial Times, Washington is reviewing the scope of the tariff regime on metal and aluminium goods amid growing concerns within the U.S. Department of Commerce and the Office of the U.S. Trade Representative that higher input costs are feeding through to consumer prices. The current approach points towards a more selective framework, with product-specific exemptions, a halt to further tariff expansions and the use of targeted national-security investigations. Countries such as the UK, Canada, Mexico and EU member states could therefore benefit from a partial easing of the measures. While this does not signal a wholesale reversal of protectionist policy, it suggests a transition from broad-based trade barriers to a more surgical and politically calibrated system.

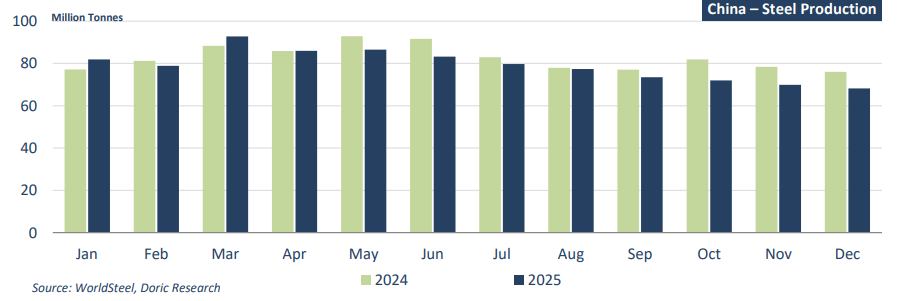

In parallel, the transformation of China’s steel sector has become more pronounced. Data from the National Bureau of Statistics of China indicate that crude steel production fell to 960.81 million tonnes in 2025, a seven-year low and a 4.4 percent year-on-year contraction, as the prolonged downturn in the property market continued to depress construction activity. Equally significant is the shift in the internal composition of steel demand. The share of rebar – the product most closely associated with construction – has declined to 13 percent from 23 percent in 2019, underscoring the scale of the adjustment taking place in China’s traditional steelintensive sectors and the gradual pivot towards manufacturing and higher value-added industrial output. Despite the contraction in domestic production, Chinese steel exports have continued to expand, reaching a new record of more than 119 million tonnes. Profitability has improved accordingly, with Mysteel estimating that 54 percent of mills operated in the black in 2025, compared with 36 percent in the previous year. Crucially, this recovery has not been driven by a rebound in internal demand but by a combination of cost rationalisation, product upgrading and the aggressive placement of surplus output in overseas markets. Looking ahead, forecasts point to a further, though more moderate, decline in output, in line with Beijing’s commitment to strict capacity controls and carbonreduction targets for the remainder of the decade. In effect, China is entering a phase of managed contraction in crude steel production while maintaining its position as the marginal supplier to the global market.

Against this backdrop, global steel demand dynamics are becoming increasingly differentiated. According to the World Steel Association, total steel consumption remained broadly unchanged at 1.75 billion tonnes in 2025 but is projected to increase by 1.3 percent in 2026, reaching 1.773 billion tonnes. The key feature of this recovery is its regional diversification. China’s steel demand is expected to continue declining, albeit at a slower pace – from a contraction of 2.0 percent in 2025 to around 1.0 percent in 2026 – as the housing market approaches a floor. However, the outlook remains subject to downside risks stemming from a more challenging external trade environment and the persistent financial constraints facing local governments, which could limit the scope for infrastructure stimulus. By contrast, the developing world excluding China is set to become the primary engine of incremental demand, with consumption forecast to grow by 4.7 percent in 2026. India stands at the forefront of this expansion, with steel demand expected to increase by around 9 percent, supported by broad-based growth across construction, manufacturing and infrastructure. Southeast Asia, led by Vietnam, continues to benefit from industrial relocation and export-oriented investment. In the Middle East and North Africa, large-scale development programmes in Egypt and Saudi Arabia are generating strong steel-intensive activity. Africa is also entering a new phase. After nearly a decade of stagnation at around 35-40 million tonnes, demand has begun to recover, reaching approximately 41 million tonnes in 2025. Over the past three years, consumption has expanded at an average annual rate of about 5.5 percent, driven primarily by northern and eastern regions. Central and South America are expected to record growth of roughly 5.5 percent in 2025, although the region’s consumption remains below its 2013 peak, highlighting the long-term impact of deindustrialisation. In the developed economies, steel demand is projected to return to modest growth of around 1.5 percent in 2026 as both the U.S. and the E.U. bottom out. Japan and South Korea, however, are likely to remain on a subdued trajectory.

The cumulative effect of these developments is a fundamental shift in the structure of the steel cycle. The market is moving away from a China-centric, construction-driven model towards a multi-regional growth framework in which incremental demand is generated across a wider geographical base. This may temper the pace of growth in traditional long-haul trades, yet it opens new avenues for tonne-mile generation. Against this backdrop, the strong start to the year in the Baltic indices is underpinned by a cautiously constructive mediumterm outlook, with future strength increasingly tied to trade reconfiguration rather than sheer volume expansion.

Data source: Doric