Yet more compliant tankers could go dark after EU bans maritime services for Russia crude trades

If Russia is to maintain its crude exports at January 2026 levels, Friday’s ban on (among other things) European tankers lifting Russian crude oil will nominally require an additional 17 Suezmax and 22 Aframax/LR2 tankers to be pulled into the shadow fleet from the compliant fleet, we believe. This assumes no overnight releases from Russia’s armada of tankers in floating storage, and the generally longer-haul shipment for Urals into China as India shuns Russian crude. We estimate that Russia’s existing dark fleet can only handle 80% of western Russia’s exports. It is perhaps notable that Russian crude oil liftings are already down to ~2m b/d for the first week of February from an average 3.47m b/d in January.

On Friday the EU announced the 20th sanctions package against Russia, which includes a “full maritime services ban for Russian crude oil.” This will replace the price cap, which was currently sitting at $44.10/bbl, around a $33/bbl discount to Brent. A maritime services ban will preclude the involvement of European-linked ships from lifting Russian crude oil. It also means no European company will be able to provide insurance to ships lifting Russian crude oil. If the UK follows suit, as we believe is likely, almost all IG P&I would be off limits.

From now on - and for as long as it takes to resolve the Ukraine / Russia situation - we can expect more challenging logistics and steeper discounts for Russian crude exports. Russian exporters will have to rely exclusively on the dark fleet, which has already become more reliant on STS from sanctioned to non-sanctioned vessels since the sanctions on Rosneft and Lukoil in late October.

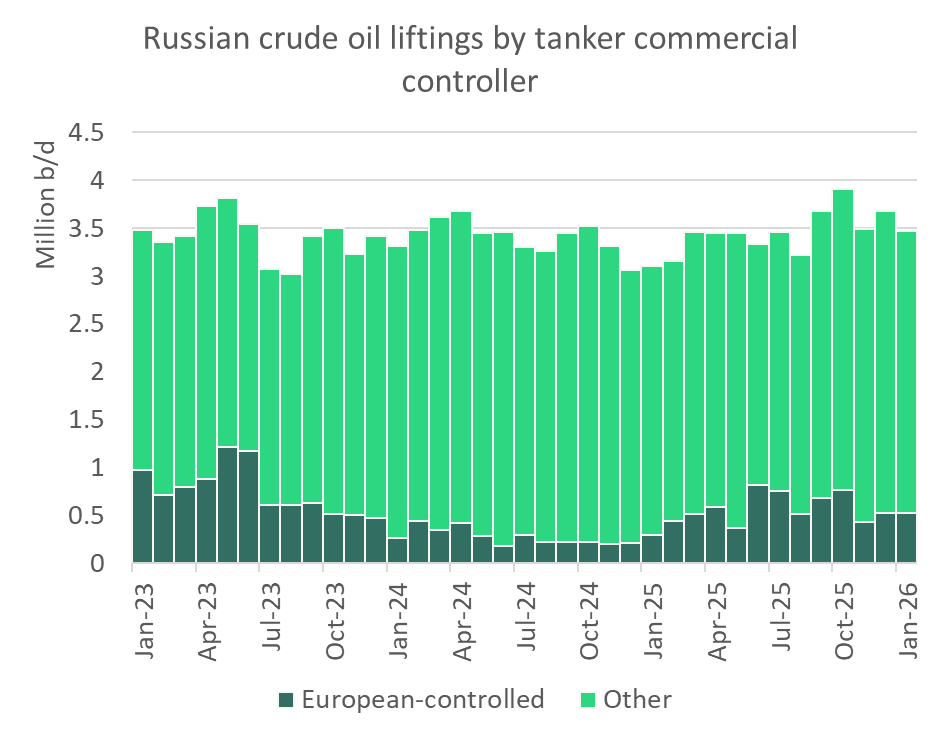

Ships that we list as under European control have lifted on average 14% (493k b/d) of Russian crude oil exports since the Rosneft/Lukoil sanctions hampered Russia’s crude exports to India. This is split roughly 70% on Suezmax and 30% on Aframax sizes. The official reported price of Urals has remained above the pre-existing EU price cap, which between September 2025 and end Jan 2026 was $47.60/bbl. Now with a maritime services ban, to maintain crude exports Russia will need to either take compliant ships into the dark fleet or hope that its existing dark fleet is quickly released from floating storage.

Source: Vortexa

16.7 million bbls of Russian crude oil is currently sitting in floating storage as India and the Chinese state-owned refiners dial back imports. As of yesterday, this was tying up 9 x Aframax/LR2 and 8 x Suezmax, and 1 x VLCC. Floating storage is currently at 16.7 million bbls, having risen by 13.3 million bbls (nearly fivefold) since the beginning of December.

Given the slow start to February, in order to maintain crude exports at January’s levels Russia would need to export nearly 4m b/d for the balance of the month. This would require around 6 Aframax-equivalent liftings (or 4 Suezmax-equivalent liftings a day). The current split of Russia crude exports is three-quarters Aframax and one-quarter Suezmax.

Russia now needs to fill the gap created by around 493k b/d of liftings by European-controlled ships.

Currently, only 17 non-European Suezmaxes and 43 non-European Aframaxes with a recent history of Russian crude cargoes appear to be free of cargo, according to cargo tracking data, and able to load before the end of the month in the Russia Baltic or Black Sea. This would cover only 80% of the export requirement if Jan levels are maintained. While Russia’s Far Eastern crude trades remain adequately covered, tonnage shortages are likely to be felt most acutely for its western liftings.

If we see new entrants to the dark fleet from the compliant fleet, this could further tighten the availability in an already strong compliant Aframax/LR2 market and help to balance out the 75 Aframax/LR2 NBs that deliver this year - 25 of which arrive over the next three months.

The EU statement made no mention of refined products. It would be even more disruptive if European-controlled ships stopped participating in Russia’s CPP trade. By our rough calculation 43% of Russia’s refined product exports (~950k b/d) were lifted on European-controlled ships since the Rosneft/Lukoil sanctions.

The EU expects the rest of the G7 to follow suit with a similar maritime services ban. However, Mr. Trump has a track record of doing things differently, and tellingly he did not lower the price cap in line with the EU and UK. However, the European-controlled ships and European and UK maritime services constitute the bulk of the western maritime services for Russian oil trades.

In further news… another 43 vessels will also be placed under EU sanctions within the EU 20th Sanctions Package, but the identities of the vessels have not yet been released.