Post US operation to remove Maduro from Venezuela will we revert to pre-Venezuela sanctions trade patterns? Which tanker sector stands to benefit? Can exports quickly increase, or will the region descend into chaos? What will happen to the dark fleet moving Venezuelan crude to China? Which crudes will be backed out if US lifts its Venezuelan imports?

On balance, the next chapter for Venezuelan crude trade should favour Aframaxes over the VLCCs, and compliant ships over shadow tankers.

Source: Vortexa

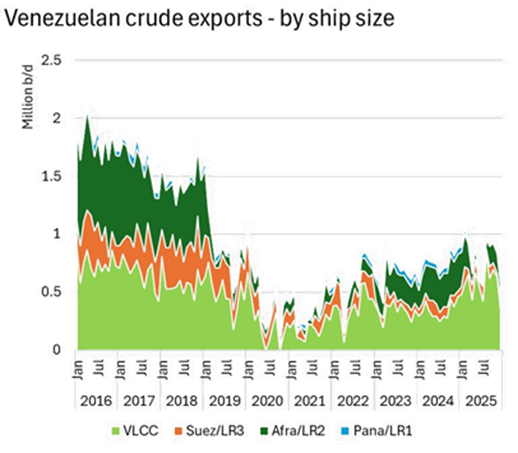

Thanks to the US blockade of Venezuela’s oil exports in December, Venezuela’s crude exports fell from 837k b/d in November to 568 k b/d in December. This was nearly 30% below the 2025 average of 788k b/d. In coming weeks we should see the lifting of this blockade and a rebound in exports back to around 800k b/d. However, the destination of the majority of these barrels would shift.

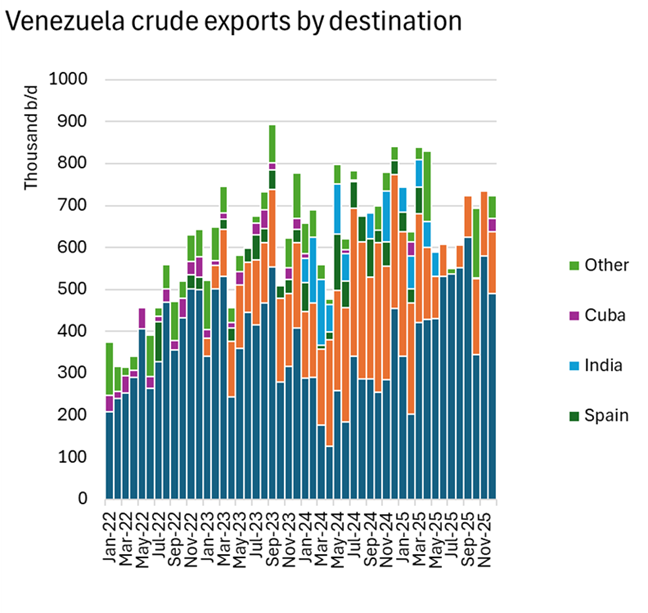

During 2025 China imported between 66%-75% and (458-590k b/d) of Venezuela’s crude exports. The upper limit assumes that the 132k b/d of crude exports with ‘undetermined’ destination went to China. The US took 22% (150k b/d). Exports to India, Italy and Spain were permitted under US sanction waivers until late May. Their combined imports averaged 43k b/d for the year. Cuba imported only around 5k b/d.

Source: Vortexa

Beyond short-term shifts in volume and export destination, Venezuela’s large oil reserves (estimated to be 17% of the world’s total) will take significant time and investment to develop. This would require a stable investment climate. Venezuela’s production infrastructure has suffered under (and prior) the Maduro regime. Kpler sees increases of around 400k b/d to 1.2m b/d by the end of 2026 if investment is forthcoming. JP Morgan predicts a 400k b/d increase could take two years.

The Trump administration expects American oil companies will invest in Venezuelan energy infrastructure. Trump suggested the US government might look to subsidise US corporate investment in Venezuela’s oil infrastructure. Delcy Rodríguez, Venezuela’s interim leader was previously the oil minister. She is seen in Washington and by oil investors as well-placed to usher in outside investment. The cost to realise Trump’s plan to revive Venezuela’s crude production and export infrastructure has been estimated at upwards of $100 billion by US academics. Shares in Chevron, Exxon Mobil and ConocoPhillips rose on Monday. A US hedge fund is now viewed as more likely to buy Citgo and its three US-based refineries from PdVSA – originally forced to sell due to unpaid debts.

Removing sanctions on Venezuelan oil would redirect almost all of Venezuela’s exports (around 800k b/d basis 2025 average) to US Gulf refineries. The US Gulf would be eager to buy heavy sour Venezuelan crude as it allows them to optimise yields and profitability. We could expect Aframax tonne-miles on the Venezuela to the US Gulf run to quadruple from last year’s averages. This translates to about 26 extra Aframax voyages each month, on top of the Chevron’s nine Venezuelan-loading voyages. Excluding lightering, about 43 Aframax voyages terminate in the US Gulf each month.

Higher US Gulf imports from Venezuela will likely displace pipeline flows from Canada. These displaced Canadian barrels would likely load in the US Gulf and head to India, China and Europe.

Until recently most US sanctioned and heavily discounted China-bound Venezuelan crude headed to the independent teapot refiners in Shandong (330k b/d in H2 of 2025, 63% of China’s Venezuelan crude imports). Over the same period, 191k b/d went to Chinese state-owned refineries outside the Shandong region.

Teapot refiners face little pressure to quickly replace lost Venezuelan crude imports given the ample availability of discounted shadow crude sitting in floating storage in East Asia. Around 70 million barrels of shadow crude oil from Iran, Russia and Venezuela is sitting in floating storage. 50m bbls (71%) of it is already in East Asia. This has developed as high exports from Russia, Iran and Venezuela since September (650 k b/d higher than the same period in 2024) coincided with weaker demand from Chinese teapots at the end of the year as import quotas ran out. Since the US imposed sanctions on Lukoil and Rosneft, India has sharply reduced its imports of Russian barrels. China’s teapot refiners have become almost the only outlet for shadow crude.

At some point Chinese state-owned refiners will look to replace the roughly 200k b/d of lost Venezuelan crude. These imports are likely to arrive on compliant vessels, possibly from Iraq (Bashrah heavy would be a good replacement). This would generate three extra compliant VLCC voyages per month. Alternatively Canadian crude could be drawn away from the US West Coast on Aframaxes. This could generate up to 10 additional China-bound Aframax voyages per month. US West Coast crude demand has been cut by the closure of P66 Los Angeles refinery in late 2025 and will fall again in April 2026 as Valero closes its Benicia refinery in Los Angeles.

Newly unemployed dark fleet VLCCs that transported Venezuelan crude to China are likely to move into the Iranian trade. Out of the 76 shadow VLCCs that lifted a Venezuelan crude cargo in 2025, 44 (58%) are free of sanctions. While they remain so, some of the younger vessels can be used to discharge in Chinese terminals. The Shandong Port Group’s ban remains in place for US-sanctioned vessels. Venezuela’s displaced sanctioned vessels could call in Iran. This would enable Iran to increase crude exports. Iran’s crude exports fell in December by around 830k b/d from 1.93m b/d the previous month due to a shortage of tonnage thanks to the buildup of oil on its fleet in East Asia.

Source: Vortexa