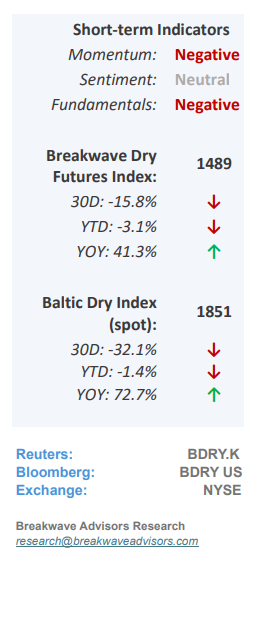

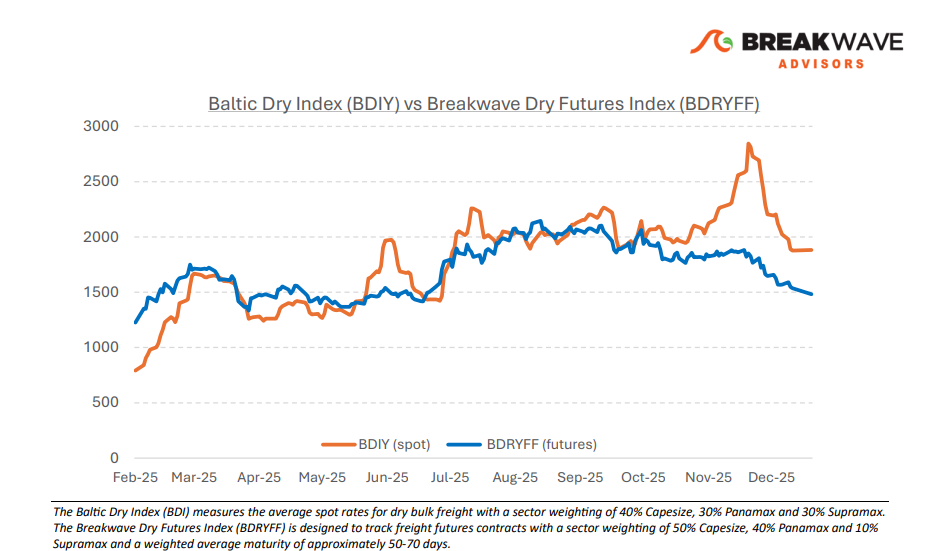

• New Year Brings Optimism – Despite a relatively long holiday break, spot indices have shown little movement. While Capesize rates are drifting lower, this trend is anticipated and well-priced into the futures curve, though Panamax rates remain weak and Supramax rates are currently underperforming in a catch-up phase. Futures remain backwardated for the Capesize market and flattish for other sectors as near-term optimism balances seasonal headwinds. We anticipate further softening, with Capesize rates likely to break the 20,000 mark and move toward the mid-teen range soon. While the potential for a strong spring recovery following a weak first quarter remains a primary unknown, the dry bulk market is supported by structural shifts in iron ore trade and the emergence of bauxite as a major growth element. Consequently, we maintain that the potential for a sharp recovery in the spring is significant, and the risk-reward profile supports a positive outcome for our base scenario over the next few months despite near-term seasonal weakness. However, as in every investment, the entry point is crucial, and thus we would need more physical evidence regarding market balance, something that we anticipate developing over the coming week.

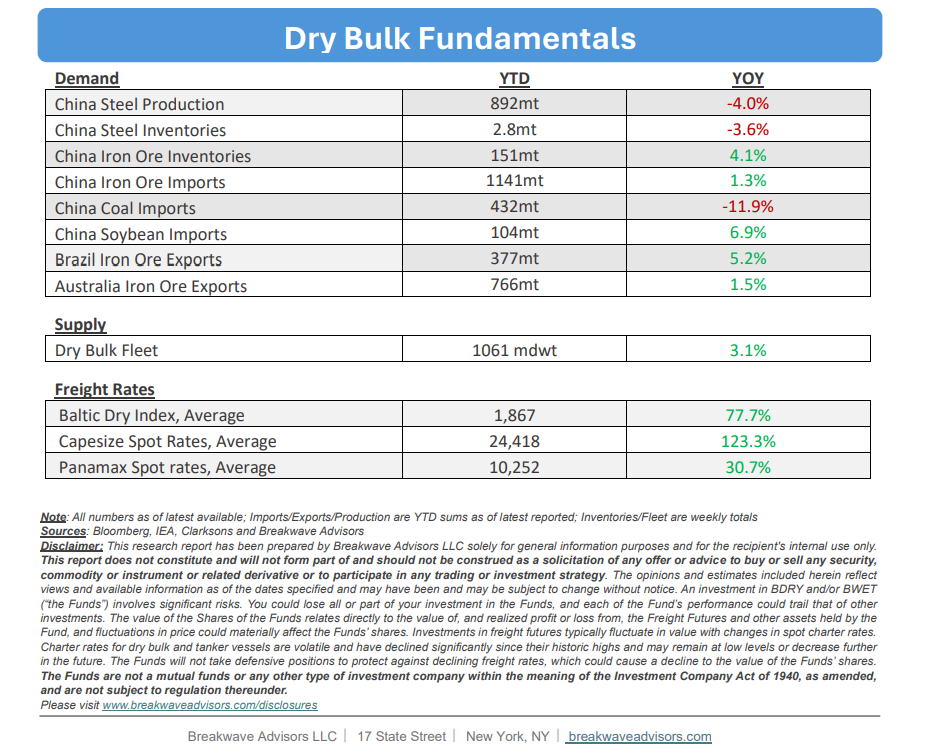

• Iron Ore Drifts Higher as Global Metal Prices Boom – Despite the recent surge in global metals markets, iron ore has experienced limited momentum due to high portside inventories, robust supply, and modest demand. Unlike more speculative mainstream metals, the industrial focus of the iron ore market has insulated it from the broader price frenzy. Our outlook remains cautious, as current supply and demand fundamentals suggest a weakening market balance. While prices have maintained stability for several months now, a correction is always possible, leading our focus toward external catalysts, such as weather disruptions or geopolitical shifts, that may create short-term trading opportunities. Absent such unexpected events, we see little reason to be involved in what seems to be another dull year for the steelmaking material.

• Our Long-term View – The last few years have been characterized by increased geopolitical uncertainty. Going forward, we expect such events to continue to affect global trade and have a meaningful impact on effective vessel supply. Combined with the potential for a multi-year cyclical rebound in China’s economic activity following the recent economic turmoil, dry bulk shipping should experience higher volatility on top of a secular tightness driven by stable bulk commodity demand and a slower fleet growth owing to a relatively low orderbook.

Subscribe: