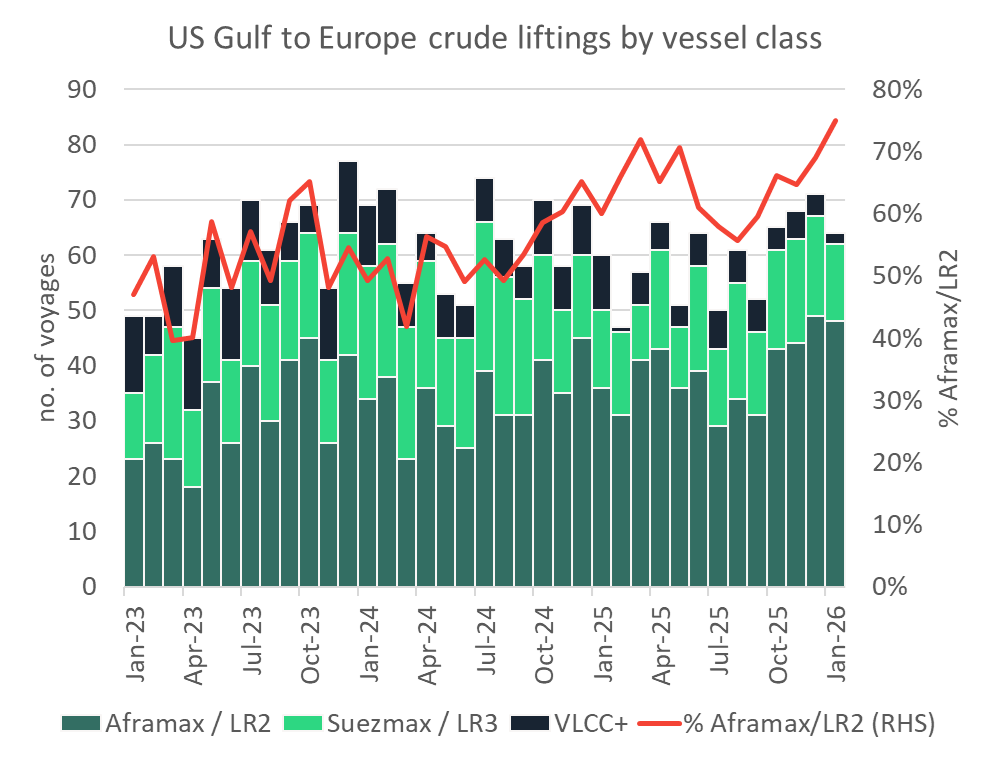

Strong European demand for WTI and a rise in liftings of Venezuelan crude to US Gulf have boosted the region’s Aframax rates to the point where Suezmaxes are now more competitive.

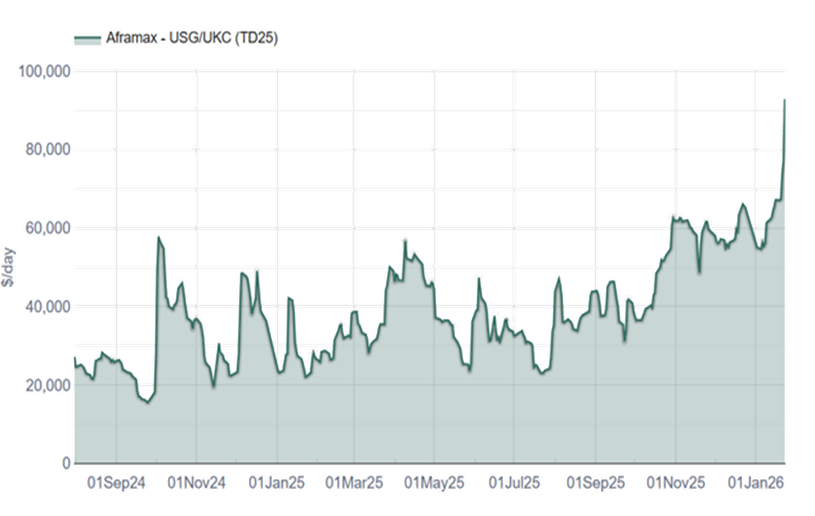

The spot market for TD25 (Aframax from US Gulf to Europe) has risen sharply since the start of last week, up from around $70k/day to over $92k/day today. Rates have increased nearly 50% since the start of January.

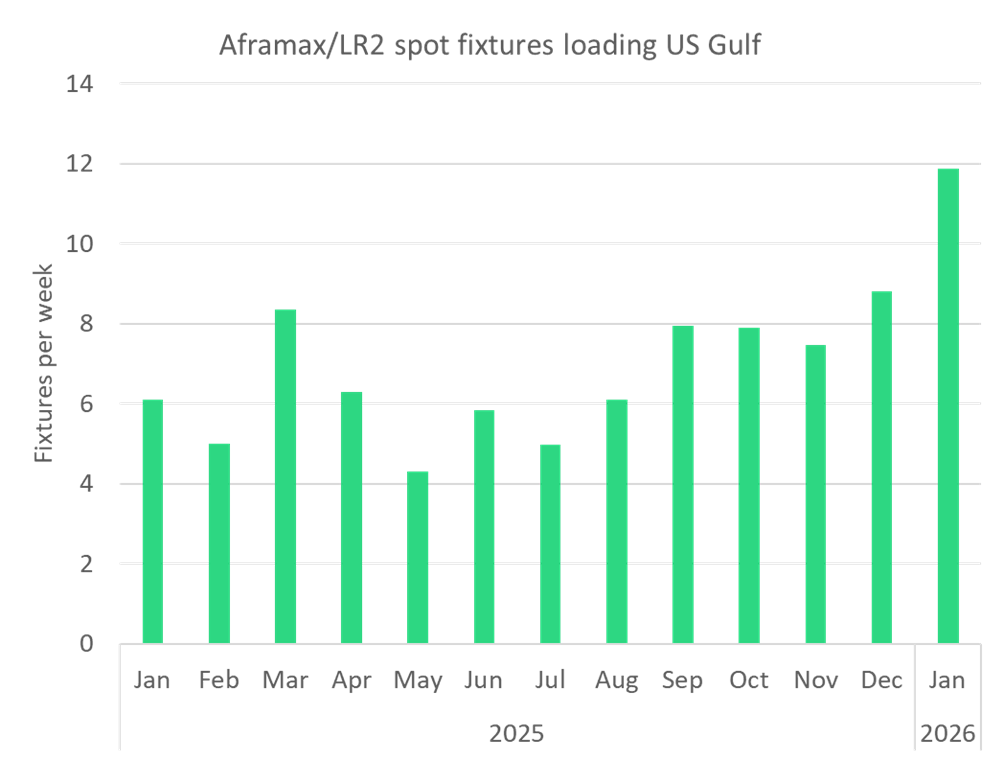

So far in January we’ve seen around 12 fixtures per week out of the US Gulf, up from around 9 per week in December. The strong US Gulf Aframax market is also largely responsible for lifting our assessment of Aframax one year TC rates by $2k/day (to $42k/day) last Friday.

Europe has increased WTI imports after eight weeks of outages at the CPC crude terminal in the Black Sea. Record 1.8m b/d CPC exports – almost exclusively to Europe - in September 2025 have dropped to 0.8m b/d so far in January. The outages followed planned maintenance on one of the SPMs from mid-November and Ukrainian drone attacks. WTI premium to Brent is at a two-year high.

A greater share of those US Gulf and Venezuelan exports have been moving on Aframaxes recently, as larger tankers have been drawn out of the region by the concomitant jump in Asian demand for Atlantic Basin crude. Eastbound flows from the Atlantic (excluding Russia) rose by 664k b/d to 5.87m b/d between Q3 and Q4 last year.

Source: Vortexa

This surge in demand has been compounded by adverse weather on the Europe to US Gulf route since the start of last week, which has slowed ballasting back into the US Gulf.

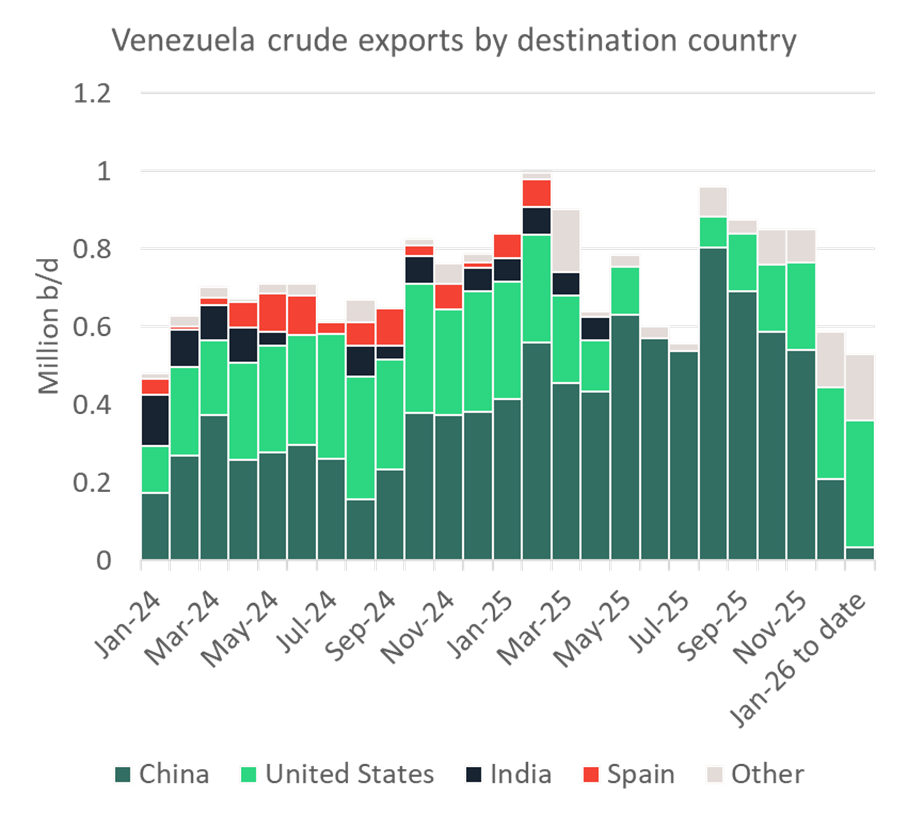

Since the US took over Venezuela’s crude exports at the start of this month, almost all liftings have been handled by Aframaxes. In addition, two VLCCs loaded with Venezuelan crude are moving to storage facilities in the Bahamas. It is likely we will see some Suezmax liftings in light of the high cost of Aframaxes in the region. Despite the recent lifting of the US blockade on Venezuela’s exports, Venezuela’s crude exports have averaged just under 530k b/d so far this month, down by around 58k b/d from December. Oil bound for the US has increased 88k b/d m-o-m.

Source: Vortexa

In the near-term, a rise in CPC volumes to Europe (now that maintenance on one of three SBMs at the CPC terminal has been completed) should dampen European demand for WTI. Europe’s spring refinery maintenance season (March/April) should further calm Europe’s appetite. US Gulf seasonal refinery maintenance in Feb/March could cut US demand for Venezuela crude. This should redirect a share of US and Venezuelan crude to Asia on larger ships. India will welcome WTI as a replacement for lost Russian crude supplies. Furthermore, the recent jump in the premium paid for dirty trading tankers is likely to pull more clean-trading LR2s into the dirty market. Between last November and today the share of LR2s trading dirty has already risen from 50% to 56% of the LR2 fleet.