This week, Allied Quantumsea Research reviews Venezuela’s mounting economic and humanitarian risks under a sanctions regime that threatens to eliminate most export revenues through 2026.

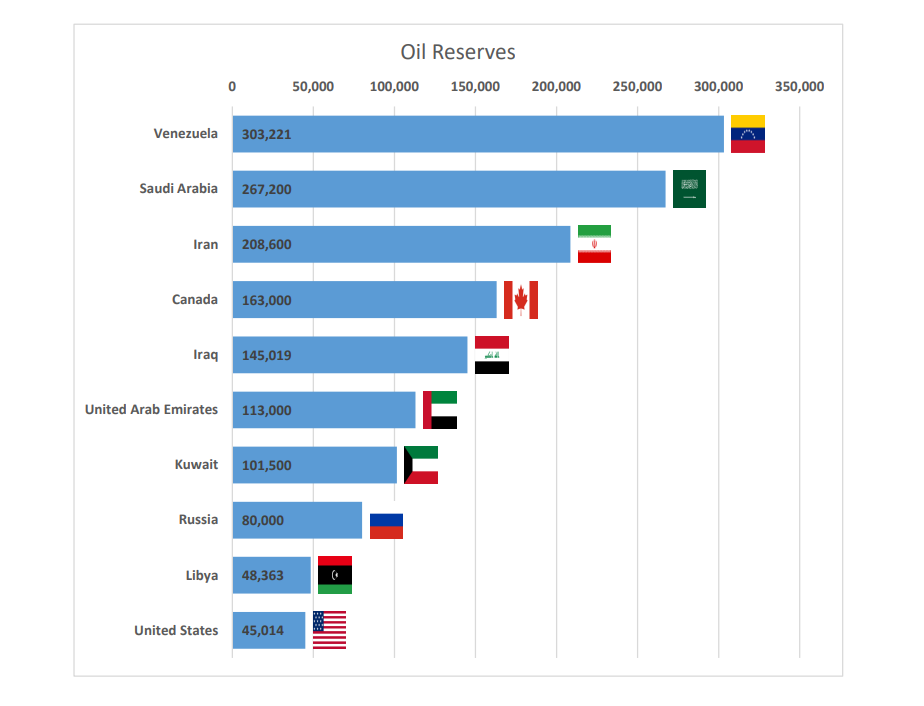

Venezuela risks losing most of its export revenues if the current sanctions and trade restrictions persist through 2026, a situation that could deepen the country’s economic and humanitarian challenges due to its heavy reliance on energy exports for foreign exchange. Despite holding the world’s largest proven oil reserves, around 300 billion barrels, production has collapsed to roughly 1 million barrels per day, a fraction of past output due to underinvestment, infrastructure decline, and limited market access. Venezuela also possesses large natural gas reserves and significant mineral deposits, but extraction and export remain constrained by structural, legal, and market obstacles. Under these conditions, the key question is not whether Venezuela’s resource sectors can recover, but the pace and framework in which any revival might occur.

An Upside, Reform-Contingent Resource Scenario for Venezuela

In an optimistic scenario marked by the establishment of a credible, internationally recognized government and partial reintegration into global markets, Venezuela's resource base enables a range of plausible long-term outcomes if sustained reforms are implemented.

Under these circumstances, Venezuela could potentially:

Progressively restore oil production to near historical peak levels (approximately 3.5 mbpd as seen in the late 1990s), noting that most external analyses regard this as a long-term, capital-intensive scenario rather than a baseline projection.

Position itself as a moderate net exporter of natural gas to regional partners such as Colombia or Trinidad, contingent upon upstream investment, sanctions relief, and the realization of cross-border infrastructure projects that are currently conceptual or only partially developed.

Advance the development of select critical mineral resources in accordance with internationally recognized environmental and social standards, aiming for improved governance compared to recent practices, though not necessarily achieving best-in-class benchmarks.

Gradually re-establish credibility as a steward of globally significant biodiversity, especially when contrasted with the notable environmental degradation experienced in recent years.

Maximizing Oil Revenues: Capital, Reform, and Redirection

To restore Venezuela's oil industry, significant private capital investment is essential, as the government lacks the financial resources to support recovery on its own. This limitation is due to humanitarian challenges, restricted foreign-exchange reserves, and roughly $190 billion in collective sovereign and PDVSA-related claim, figures that vary depending on definitions and assumptions about recovery.

Analyses from various sectors, including industry, multilateral organizations, and investors, generally agree on key prerequisites for sustained reinvestment:

A substantial reform of the legal and institutional systems overseeing hydrocarbons,

Assurance of contract integrity and robust investor protections,

Environmental and operational guidelines that largely comply with international standards,

An inclusive process for restructuring debt, which may be connected to strategies for reviving both the oil and mining sectors,

Exploration of creative financial tools, such as debt-for-climate swaps or methane-reduction initiatives—though these are still at a preliminary stage and not guaranteed.

Near-Term Production Recovery: Scope and Constraints

Several industry and sell-side assessments suggest that, even absent immediate, comprehensive legislative reform, production could potentially recover toward the 1.5–2.0 mbpd range within a two-year window under a best-case operational normalization scenario. Such an outcome would rely heavily on enabling existing foreign operators, rather than launching new greenfield developments, and would likely exceed most current base-case projections.

In this context, incremental gains would largely depend on allowing established operators (including Chevron, ENI, Repsol, and Maurel & Prom) to operate closer to technical capacity, subject to sanctions regimes, contractual clarity, and operational logistics. While this channel offers relatively rapid upside, it remains conditional and insufficient on its own to support longer-term expansion.

Export Rerouting and Revenue Realization

A potentially important near-term lever lies in export destination and pricing dynamics rather than headline production volumes. Current exports, estimated at roughly 800–900 kbpd, are heavily oriented toward Asia, particularly China, often at steep discounts reflecting sanctions risk, logistics, and intermediary costs.

Partial redirection of these flows toward higher-value markets such as the U.S. Gulf Coast could materially improve realized netbacks relative to current arrangements. The magnitude of revenue gains would depend on price differentials, shipping costs, compliance structures, and regulatory permissions, but could be significant even without changes in aggregate production.

Why Venezuela Still Matters for Shipping

Although Venezuela currently represents only about 1% of global crude supply, it continues to matter for shipping because of the distortions its exports create rather than their absolute volume. For much of the sanctions period, Venezuelan crude has relied on opaque logistics, including shadow fleets, elevated insurance and demurrage costs, and unusually long-haul routings to Asia, particularly China, thereby inflating global tonne-mile demand and embedding risk premia in freight markets.

Recent developments involving Vitol and Trafigura suggest a partial shift in trade mechanics, though not yet in geography. Both trading houses have begun marketing Venezuelan crude under authorized and compliant frameworks, replacing irregular shadow movements with documented, licensed shipments. These cargoes are being offered primarily to China, which remains the most commercially viable destination due to refinery compatibility, blending capacity, and established demand for Venezuelan heavy grades. The predominance of China-bound flows reflects market structure rather than regulatory direction, as existing authorizations formalize exports without mandating a redirection toward the U.S. or Atlantic Basin.

From a shipping perspective, this transition is expected to reduce opacity and counterparty risk while preserving long-haul Asia tonnemile demand in the near term. Any future reorientation of Venezuelan exports toward the U.S. Gulf Coast would significantly shorten voyage distances, compress tonne-miles, and favor Aframax and LR1 utilization over long-haul VLCC employment, a shift that would be bearish for aggregate tonne-mile demand but positive for transparency and freight predictability.

Looking ahead, most market assessments converge on a near-term recovery ceiling of roughly 1.5–2.0 million barrels per day over a twoyear horizon under best-case normalization assumptions rather than as a base case. Importantly, adjustments in heavy-crude pricing, blending economics, and diluent availability are expected to precede any material volume recovery, typically providing a six-to-twelvemonth lead signal for shipping and freight markets.

Looking ahead

Venezuela’s crisis is no longer framed by markets as an imminent collapse; much of that risk is already priced. The central question has shifted to reintegration: how, when, and under what constraints Venezuelan barrels re-enter the global system. For oil markets and shipping, Venezuela remains a geopolitical wildcard, with the potential to influence price trends, freight flows, and refinery economics as trade patterns normalize over time.

Data Source: Allied