OFAC and China port fees shift focus back to VLCCs

Yesterday’s dramatic escalation of OFAC sanctioning on companies, individuals and ships linked to Iran’s oil exports, followed by this morning’s confirmation by China that ships owned by US entities will face escalating fines from Oct 14 for port calls at all Chinese ports, has put the focus sharply back on VLCCs.

China port fees

The wording of China’s port fee announcement is unclear. However, if we are to interpret this (as most of us do) to include US-listed VLCC owners like Frontline, Euronav, Okeanis Eco Tankers, DHT, Navios and International Seaways - this would cover 93 VLCCs (10% of all VLCCs or 13% of VLCCs under 20 years old) – responsible for roughly 528k b/d or 5% of China’s seaborne crude imports. Some of those US listed companies will have less than 25% of shares held by US entities, and may therefore be exempt. None of the exemptions for smaller tankers that apply to USTR section 301 would appear to have been added to the Chinese retaliatory port fees. Therefore, major US listed product carrier owners like Scorpio will be following developments carefully. With no apparent runway to the introduction of these fees, any VLCCs owned by US entities – including those on time charter to third parties - that are currently in transit to China would appear to be caught up, with no charterparty clauses to cover them. Vortexa data suggests that 17 VLCCs owned by US -listed companies will arrive laden in China on or after Oct 14. If Chinese oil companies are forced to resell these bbls we could expect Brent prices to drop.

Amid all this uncertainty, at the time of writing Balmo for TD3c had jumped WS 14 points (to WS95) since 4pm (London) yesterday. The November contract had moved from WS 79 to WS 90, Dec from 78 to 83. Our spot brokers could now see the VLCC market moving to WS 100 this week from WS 72 at yesterday’s close.

OFAC sanctions

Beyond the additional 6 VLCCs (and 1 LR1) targeted by the latest OFAC sanctions for their role in Iran’s exports (in addition to tugs and LPG carriers) the sanctions now extend to a Chinese refinery (Jincheng Petrochemical) and a storage terminal at Rizhau (see notes at bottom). The OFAC sanctions come hard on the heels of the end September ‘Snapback’ of UN sanctions under the JCPOA, which targets Iran’s nuclear programme.

Iran’s total crude exports are down from their peak of over 2m b/d in Q2 this year. However, oil exports on older VLCCs have quietly continued their upward trajectory, from virtually nothing in early 2020 (122k b/d in q1 2020) to around 1.5m b/d today.

For VLCCs, any challenges for crude imports from Iran will help lift demand for compliant tankers, either by pulling older compliant tankers into Iran’s dark fleet, or by requiring a rise in non-discounted crude imports from countries that don’t need to employ shadow tankers. As crude exporters are currently relying heavily on Chinese stockbuilding to support oil prices, any loss of Iranian bbls would likely allow for an acceleration in the rate at which OPEC’s production cuts are reversed. Further down the line, any Chinese refinery that relies on discounted crude to remain profitable may come under pressure to cut runs and eventually close, or more immediately to increased imports of Russian Urals and Venezuelan bbls.

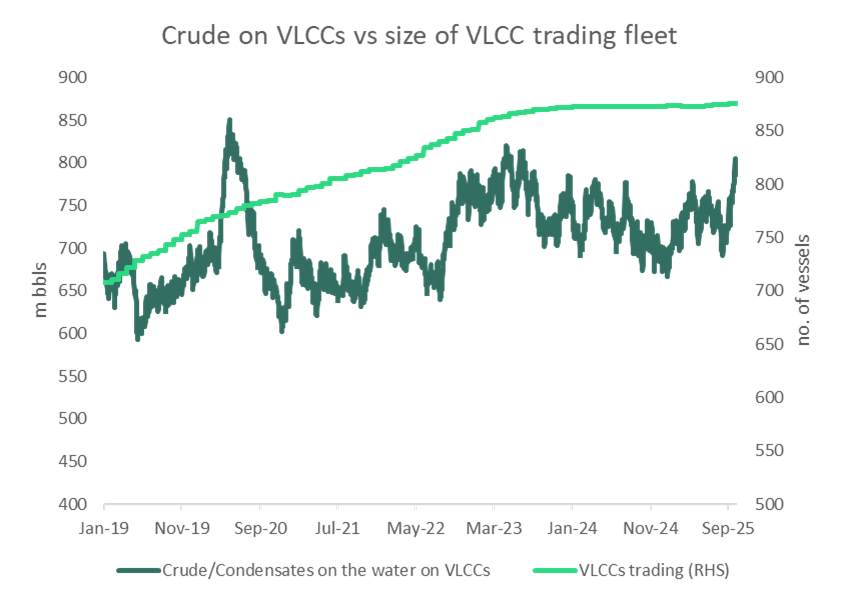

Even before these tighter sanctions were announced, we were of the mind that VLCC demand should remain strong to close out the year. Thanks to the rapid reversal since April this year of the OPEC+ oil production cuts (introduced in phases from April 2023); and thanks also to strong growth in non-OPEC+ production over the same period (mostly in the Atlantic), global oil production has grown by around 5.6 m/bd over the past 2.5 years (IEA). Export growth has not kept pace with production (the startup of major new Middle East and Nigerian refineries over the past couple of years has absorbed some of that production locally and more recently peak summer cooling demand in the Middle East and compensatory production cuts by certain key exporters like Iraq have limited the growth of exports) but in recent months tankers generally, and VLCCs in particular, have seen a surge in demand (see chart).

Total cargo sitting on VLCCs today is already comfortably back to the levels before OPEC first announced its cuts, helped by higher storage employment for Iran’s tanker fleet. Suezmax utilisation is similarly high. Meanwhile the fleet of VLCCs under 20 yrs old has shrunk by 50 units, 46 of which now have since been sanctioned by OFAC.

Any continued reversal of OPEC+ cuts into November and beyond should lift VLCC demand and rates. OPEC announced at the weekend it was unwinding a further 137 k/bd of production cuts in November. This qualifies as a ‘cautious’ target, similar to October’s increase, but well down on the 500+ k/bd increases over the summer months.

But to coax more oil production out of Saudi Arabia and UAE (the only two with meaningful spare capacity), the forward oil price curve would have to remain broadly backwardated. Today’s backwardation is limited to the front of the curve as Chinese stockbuilding mops up spare bbls.

To avoid contango throughout the curve, either Chinese stockbuilding will have to continue at its recent pace, or oil supply will have to be lost from somewhere else in the system. If Saudi Arabia and the UAE are required, once again, to bear the brunt of these losses, VLCC demand for compliant ships should suffer. If losses, however, come from Russia, Iran or Venezuela, compliant VLCCs will benefit. The chances of losing some Iranian crude have just gone up.

Even before the OFAC sanctions announcement, several months of high export volume from Russia, Venezuela and Iran led us to believe we are less likely to see further gains from these key employers of shadow vessels. Russia’s crude export growth in recent months is largely the result of Ukrainian drone attacks on 1/3 of Russia’s domestic refining capacity. If Ukrainian attacks were to disrupt crude exports as well, replacement bbls would be required from Middle Eastern exporters on compliant ships. Alternatively, if the growth of Russia’s shadow fleet does not keep pace with its exports (particularly now that Europe’s lower price cap is enforced and Greek owners have largely exited the Russian oil trade), then the Middle East will be called upon to compensate, with compliant ships.

_________

Tidal wave of cargoes on the water

Crude oil sitting on VLCCs has reached multiyear highs according to cargo tracking data. OPEC+ exports increased in September and along with a high volume of Atlantic Basin crude in transit to Asia, this pushed September crude exports to the highest observed since April 2020. The rate of liftings has fallen 10% since mid-September and until yesterday VLCC rates had cooled as discharges looked likely to outpace liftings this month. However, we were maintaining that crude tanker demand would have remained supported if Brent ranged $65-70/bbl and China could continue to call on discounted crude from Russia, Venezuela, and Iran. There were certainly some questions circulating around storage capacity in China. For instance, observed state-owned commercial storage tanks were recently touching historic high utilisation levels. But China’s geostrategic imperative of ensuring a cushion of crude supply in a time of increasing tension and unfulfilled SPR mandates persuaded us that Chinese stock builds could continue for several months. In the near-term we were expecting to see VLCC rates supported by the high numbers of Atlantic Basin-origin VLCCs heading east. We foresaw supply dislocation and a lack of availability of vessels in the Atlantic Basin. In the unlikely event that Iran drops off the list of discounted crudes available to China, its stock building efforts could slow. But VLCCs would benefit from an increased use of compliant tankers to satisfy Chinese demand, even if overall crude flows to China slowed in the absence of a stock build surplus.

Positive supply fundamentals

The number of VLCCs trading has remained basically flat since April 2023 (+13 ships) when this first phase of today’s OPEC cuts began . Of these, the number of units under 20 years old is down by around 6% (-133 VLCCs), and 16% of the total VLCC fleet is under sanctions. As such, the fleet is older and less compliant, meaning there is less available tonnage to lift increased crude exports from Saudi Arabia and the UAE.

Source: Braemar, Vortexa

China’s stockbuilding outlook

OPEC’s future cuts unwinding decisions will be contingent on China’s demand. China imports 30% of all crude from OPEC+, and with China’s Q4 oil demand forecasted to decline by 200kbd compared to Q3 (IEA), inventory building will be key. Argus is predicting an acceleration in China’s SPR building to 680 k/bd between October and March due to annual SPR fill mandates still unfulfilled. The state-owned refiners have only added around 15% of the mandated annual volume to the SPR since April and have through March 2026 to add the remaining balance – around 120 m bbls.

China’s SPR volumes are difficult to track given the lack of official reporting and the use of underground caverns and not just floating roof tanks visible in satellite imagery. Nevertheless, the large unfulfilled mandate for this year’s SPR storage plus relatively low crude prices indicate China’s buying appetite should continue as a high volume of crude in the supply chain should keep prices favourable for stockbuilding.

Vortexa states that inventory additions of just 50 mb by state-owned refiners could soon reach 71% tank utilisation – a level where historically ports have seen capacity constraints in terms of discharge delay and congestion. Reuters collated public sources and report new storage capacity of around 169 million barrels across 11 sites as planned through next year. Vortexa sees the likelihood of planned new capacity coming online as late 2026 or early 2027, so there could be a limit to how much can be absorbed in tanks until then. Delays in discharge would support rates by adding to voyage length and tightening vessel availability at load ports.

In our view, the possibility of capacity limits in state-owned refiners’ tanks and the remaining mandate to fill the SPR means these volumes are likely to go into underground cavern storage. We see the favourable pricing environment and geostrategic mandate to fill the SPR as indicative that Chinese stockbuilding will continue.

Long-haul crude cargoes surge

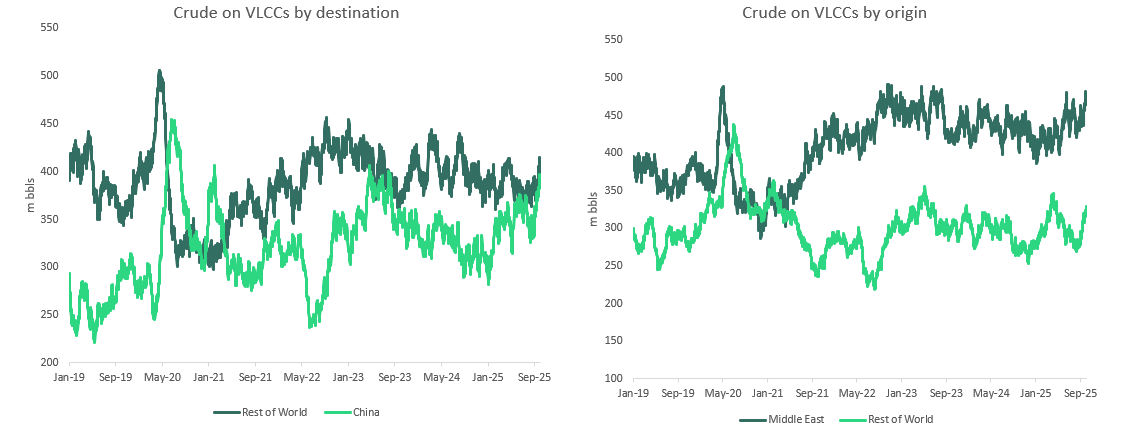

Although the immediate possibility of contango has lessened due to OPEC’s lower than expected unwinding announcement, we see a large wave of crude supplies heading for importers, specifically in Asia. Crude on the water on VLCCs has surged since the start of September, now reaching levels not seen since June 2023. Compounding this is a large volume of Atlantic Basin crude heading to Asia – liftings increased 23% in September - which is lengthening average voyage times while VLCC liftings of Middle East crude heading to East Asia are also15% above the seasonal average.

Cargoes to China have been the cornerstone of VLCC demand throughout 2025. Since January, cargo volumes on VLCCs heading to destinations outside of China have declined, and cargoes carried by VLCCs to China have continued to increase, roughly reaching parity this summer, when nearly 50% of all VLCC cargo volumes were destined for China.

Source: Vortexa

Along with this current surge of cargoes on the water on VLCCs, cargoes destinated for locations outside of China are also surging – because of strong demand from India, South Korea and Japan in September. Usually, cargo on water to China versus the rest of the world is inversely correlated due to the finite supply of VLCCs available (see above left-hand chart). Current surges in both China-bound and non-China bound cargoes on the water could signal future VLCC supply dislocation in the Atlantic Basin in particular. Crude on the water heading to Asia on VLCCs includes an increase of around 1.2 m/bd of crude exports from the Atlantic Basin. This high volume of Atlantic Basin-origin VLCCs going East means upon discharge there will likely be too many vessels clustered East of Suez and a lack of availability in the West, which should support Atlantic Basin VLCC rates as the year winds down.

Yesterday’s OFAC sanctions announcement in brief

Today's announcement designates 33 vessels, 7 of which are crude tankers and the rest are LPG carriers, small chemical/oil tankers and a few tugs. These 7 crude tankers were heavily relied on in recent months due to being free of sanctions, accounting for 20% of all of China's Iranian crude imports in August.

Due to Shandong's ban on OFAC-sanctioned tankers, today's sanctions just make it more logistically difficult for Shandong to import Iranian crude, as now importers will have to find more "clean" tankers to discharge in port.

A shipping agency operating in Qingdao has been targeted, which is interesting considering Qingdao is the port which recently announced a points-based system for older vessels and those vessels missing documents. Qingdao cited compliance and environmental reasons for this announcement, but it can also be read as an exercise to avoid further sanctions scrutiny.

A teapot refinery - Jincheng Petrochemical - was also sanctioned. It utilises a terminal that is responsible for around 20% of all Iranian crude imports in China. I don't know the specific intake of that refinery compared to overall imports, but it is notable to see continued pressure on the importers. The refinery itself can process about 400kbd last I heard.