Today’s FFA prices suggest VLCCs will outperform Suezmaxes and Aframaxes over the next few years. Could they be wrong?

By Henry Curra

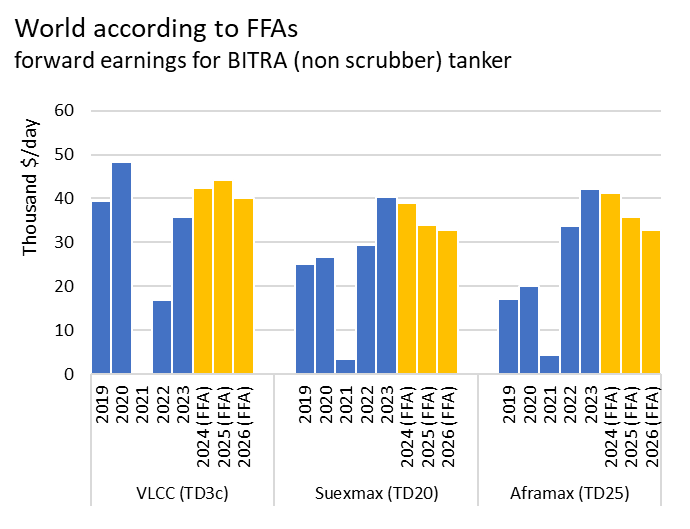

In absolute terms, FFA prices indicate a continuation of strong markets across the crude tanker sector through 2026, and possibly beyond. But while VLCC pricing points to a continued improvement in earnings through 2024 and 2025, Suezmax and Aframax markets are backwardaded.

To some extent a relative over-performance of VLCCs over coming years is to be expected. The unusual events that have allowed Aframaxes and Suezmaxes to buck the long-term trend of bigger ship, bigger earnings over the past few years are either behind us, or temporary. As they fade into the background, charterers can once again expect to pay a premium for economies of scale.

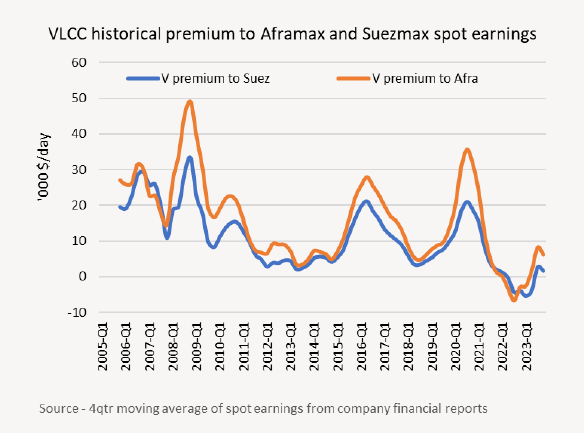

In the 16 years running up to COVID (for which we have comparable company statistics) VLCCs averaged $12.9k/day above Suezmaxes and $18.5k/day over Aframaxes. For several quarters post-pandemic Aframaxes and Suezmaxes were earning a premium over VLCCs – of up to $5,000/day in some quarters. Today the benchmark VLCC, Suezmax, and Aframax routes are trading in the spot market at roughly the same level, but Cal26 TD3c (VLCC) is back to pricing in a $7k/day premium to both TD20 (Suezmax) and TD25 (Aframax).

Relatively speaking, it could be argued that VLCCs have had a run of bad luck since the pandemic. Firstly, they were handicapped by the geographically staggered nature of the post-lockdown economic rebound. VLCCs were left in the starting blocks as China - accounting for nearly half of VLCC demand – delayed relaxing COVID restrictions until the start of 2023. At roughly the same time Europe boosted Aframax and Suezmax demand by banning Russian crude imports. VLCCs were too big to load at Russian terminals, so missed out on the bonanza of Russian crude moving to India and China. More recently still, Houthi militant attacks on shipping in the Red Sea have forced Aframaxes and Suezmaxes to avoid the Suez Canal, adding significantly to their tonne-miles. For VLCCs, little changed.

VLCC prospects now look more promising. For one, fleet growth favours VLCCs over both Afras and Suezmaxes.

Newbuilding orders for VLCC have only recently picked up after several quiet years. As a result, VLCCs will welcome just 5 newbuildings into the fleet up to the end of 2025. They represent 0.6% of today’s fleet. This compares to 80 Afra/LR2s (8% of today’s fleet) and 36 Suezmaxes (6.3% of today’s fleet). 2026 is now a busy delivery year for all three size categories, but again relatively busier for Afra/LR2s and Suezmaxes than for VLCCs.

If tanker earnings remain at least as strong as the FFA forward curve suggests, we are unlikely to see much in the way of removal of older vessels over the next two years. But older ships move less cargo, and as such we can discount some useful capacity. And while Suezmax and Aframax/LR2 fleets have a higher share of older ships than VLCCs (see box), VLCC charterers tend to discriminate more heavily based on age.

——

Box: Without recycling, the 20+ yr. old segment of the VLCC fleet will grow from 97 to 154 ships by the end of next year. Over the same period, the old Suezmax fleet will grow from 76 ships to 120 ships. The old Afra/LR2 fleet will grow from 152 ships to 255 ships. 28% of the VLCC fleet is currently over 15yrs old, and 11% is over 20 years old. 32% of Suezmaxes are over 15 and 14% are over 20. 40% of the Aframax/LR2 fleet is over 15 and 14% is over 20.

——

For instance, a VLCC that is 20 or over (11% of the fleet today, accounting for 8% of all VLCC voyages last year) can expect to do just 40% of the work of an under 20yr old ship when it comes to moving cargoes. This is down from 90% pre-COVID. When storage employment is included, the older ship will manage 60% of the roughly 210 earnings days annually of the younger ship. In today’s market, this is clearly a good enough incentive to put the ship through its 4th special survey. Older Suezmaxes do about 60% of the moving days of a younger ship (and about 70% of the earnings days), while old dirty-trading Afra/LR2s do about 70% of the cargo-hauling work of a younger ship (and 80% of the annual earnings days).

Many of these older ships load in countries that are subject to US sanctions. Export volumes from Iran and Venezuela are expected to plateau this year. Russian output is expected to decline next quarter, nominally because of its OPEC+ pledges. It is therefore hard to see who will accommodate the growing number of older ships - and not unreasonable to assume that the average usefulness of each older ship will decline. For the tanker fleet over 85,000dwt, the overage fleet grows from 13% today to 21% by the end of next year. As useful capacity of older ships is discounted further, VLCCs are likely to benefit most.

On the demand side VLCC prospects look similarly promising. The East’s growing need for crude oil looks set to be satisfied mostly by Atlantic basin producers over the next two years at least. Unless Saudi Arabia grows tired of fellow OPEC members producing more than promised, the Middle East is unlikely to lift exports for the balance of this year – as the IEA conceded last week. Ultra-long-haul crude trade from West to East should therefore benefit VLCCs more than the smaller-sized crude carriers. The ramping up this year of Dangote’s mega refinery in Nigeria might reduce West African crude exports - some of which currently moves east on VLCCs, but Suezmaxes will feel the loss of West Africa’s crude exports to Europe more sharply. Indeed, VLCCs look likely to benefit from extended delays discharging Dangote’s imported crude from outside Nigeria, notably from the USG.

The expansion of crude exports from Western Canada as TMX starts to flow within the next couple of months will certainly see more liftings on Aframaxes. But VLCCs could simultaneously find themselves moving more Alaskan or Ecuadorian crude to Asia as California turns to Canada. A slight reduction in the volume of Canadian crude oil piped into the USG could in theory cut the region’s exportable surplus to the detriment of VLCCs. But more likely the loss of Canadian heavy-sour crude grades, on which USG refineries depend, would need to be replaced by imports. With Mexico’s Dos Bocas refinery threatening Mexico’s surplus of heavy crude, and Venezuelan heavy crude soon to be off limits to most US importers, these replacement barrels are likely to come from further afield, on VLCCs. Meanwhile the region’s sweet light crude exports continue to grow in line with shale production.

For the time being, Afras/LR2s are well supported. This support comes from both crude oil and refined products. Russia has reduced its crude exports in recent months, but Ukraine’s drone attacks on Russian oil refineries has today shut in nearly 800k b/d of refining capacity. This should increase the country’s exportable surplus of crude oil. As US sanctions reduce the number of (mostly Russian) ships that can lift Russian crude, Russia is faced with the choice of selling below the price cap to access European/G7 tonnage, cutting crude exports, or moving crude even longer-haul to countries less fussed with sanctions, like China. China has already seen Russian crude imports rise in recent weeks, much of it moved on Aframaxes.

Russian fuel oil continues to move in volume to Asia on Aframaxes, while LR2s are receiving a significant boost from Red Sea diversions as Russian naphtha and Mid East + Indian diesel/jet re-routes via Southern Africa. Since the first Houthi attacks late last year, CPP tonne miles have risen 16%, and DPP by 15%. Crude oil, which is less reliant on the Suez Canal, saw associated tonne-miles rise by just 4% over the period. The strength of the clean tonne-mile demand has benefitted LR2s more than other coated tankers. It has already led to the cleaning up of several dirty-trading LR2s in recent months - at a time when lifters of Canadian crude are hunting for dirty ships. LR2s are also key beneficiaries of the rise in output from new and expanded Middle Eastern refineries (Al Zour, Jizan, Duqm). CPP exports on LR2s from the Middle East have risen by 28% to 1.78m b/d since November last year, but they are still some way off the circa 1.2m b/d levels achieved throughout most of last summer.

Does size matter?

For Aframaxes and Suezmaxes to maintain earnings parity with VLCCs, or indeed to return to a premium, VLCCs must perform worse than expected, or the smaller ships better. For VLCCs to perform worse, the most likely agent of change would be China. An ailing property market, now in its third year, and high public debt point to another difficult year ahead for China. Protectionist forces in Europe and USA will not make things any easier, particularly if Trump gets his second term in office. China managed 5.3% GDP growth last year despite similar misgivings, and is targeting ‘around’ 5% this year. This still leaves China’s oil demand growth at a healthy (by today’s standards) 3.8% - albeit comfortably off last year’s 11.7% growth, according to the IEA. A short-term benefit for VLCCs could come from Chinese crude stock building. China’s onshore stocks have been allowed to dwindle 11.5% since last summer, according to Vortexa. A partial rebuild can now be expected to join every lull in oil prices.

For Afras and Suezmaxes to perform better than expected the TMX pipeline is the wild card to watch. If the majority of TMX crude heads not to California but to Asia on Aframaxes in the second half of this year, dirty Afra/LR2 markets would tighten. Indeed, that it the main reason we believe it won’t happen.

The path of least resistance leads us to conclude that VLCC earnings should return to a premium over Aframaxes and Suezmaxes over the next couple of years, as FFA forward curves suggest. But that spread is heavily dependent on regional events that are difficult, if not impossible, to anticipate. For instance, a possible (but unlikely, we feel) Chinese military intervention in Taiwan might see the US throttle China’s crude supplies out of the Middle East. This would disproportionately harm VLCC demand. Or weaker economic growth coupled with lower oil prices might encourage the US to further restrict Russian crude exports, hampering demand for Aframaxes and Suezmaxes. One of the world’s many crude pipelines could be targeted in a terrorist attack. An oil spill could re-awaken charterers to the risk of association with older tankers. The possibilities are endless. However, the fact that oil will continue to serve as a tool for political leverage seems almost guaranteed. That is thanks in large part to that tanker fleet’s extraordinary track record for keeping oil moving where it is needed, at tolerable prices. In our assessment, the role that oil plays in global geopolitics presents us with the biggest upside risk of all.