This week, in the East, we discuss why the fleet operating in the Russia Far East is unlikely to face constraints, and we look at strong intra-China flows and what this means for tankers. In the West, we investigate why TD19 has failed to ignite despite high exports at Sidi Kerir. On the clean side, we explore why Russian diesel is travelling shorter distances.

By Mary Melton

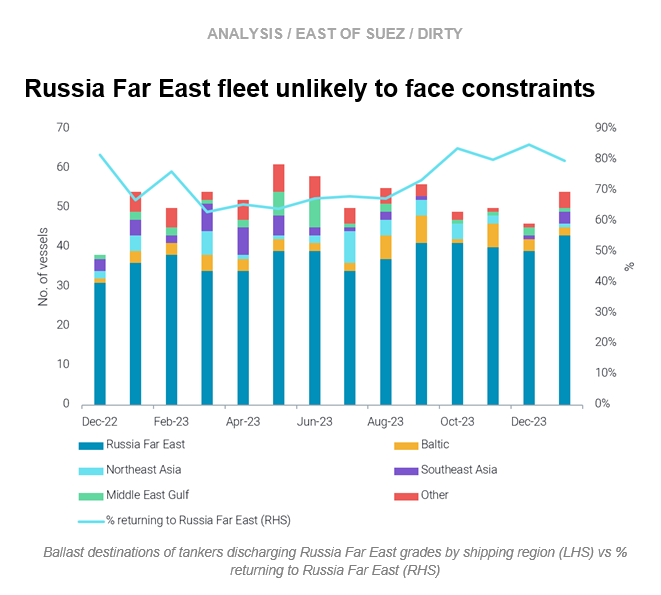

The disruption in Sokol cargoes to India in January due to the sanctioning of entities led to issues with accepting payment for the cargoes. Prior to this, Russia Far East grades (ESPO blend, Sokol and Sakhalin blend) lost market share in terms of tonne-mile demand to India beginning late November 2023. For Jan-Nov 2023, Russia Far East grades average tonne-mile share to India was 43%, whereas in Dec 23-Jan 24 this share dropped to 19%. Currently, Russia Far East grades overwhelmingly end up in China.

When examining ballast destinations for tankers discharging Russian Far East grades, the majority of vessels go back immediately to Russia Far East to load again. This suggests a mostly segregated fleet employed on the Russia Far East-to-China route, which will be unaffected by more stringent sanctions enforcement.

Furthermore, the relatively small involvement of EU operators (11% of all tankers that have loaded since Dec 2022) and high involvement from Russian, Chinese, and low-tax sovereign-linked operators (65%) suggests the same patterns of vessels exiting the trade we have observed for the fleet carrying Urals do not apply in Russia Far East.

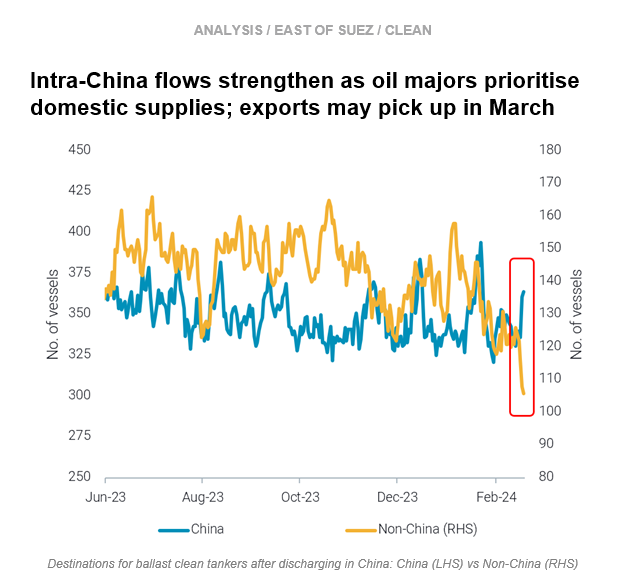

In February, China has witnessed a remarkable upswing in intra-country CPP flows as a direct response to Chinese refiners intensifying fuel production and prioritising domestic supplies to meet the heightened travel demand during the Spring Festival rush.

This is not only evident in loadings data but also in the destinations of ballast clean tankers. Post-discharge in China, an increasing number of vessels are opting to remain within Chinese waters, likely contributing to high vessel supply elevated in NE Asia and cooling MR freight rates in the region (TC7, TC10, TC11).

As the travel season ends in early March and with notable improvements in clean fuel export margins recently, Chinese refiners are likely to ramp up exports in March. Likely in anticipation of this, vessels are increasingly ballasting towards China from elsewhere (up 25% w-o-w), buoying vessel supply.

Prompt Aframax and Suezmax supply in the Mediterranean is relatively high. This is especially notable for Suezmaxes, which are choosing to stay in the Med or Northwest Europe after discharging in Europe instead of going to WAf or the East Coast Americas, where high vessel supply continues to weigh on rates.

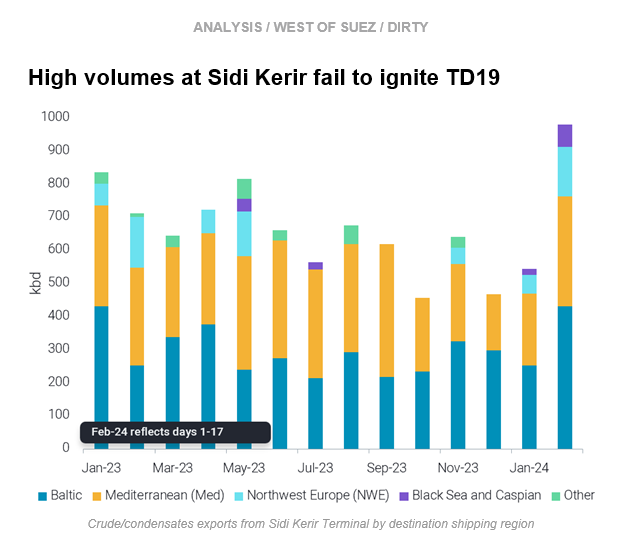

There are clear incentives for remaining in the Med. The return of exports from the Zawia Terminal in Libya following the reopening of the Sharara Field should support Aframax employment. Additionally, Saudi Arabia has increased exports from Yanbu in Jan-Feb, which enables exports to WoS while avoiding the Bab-el-Mandeb. These volumes are then discharged at Ain Sukhna and go to the Med via the SUMED pipeline. Reloading of these volumes at Sidi Kerir is usually by Aframaxes, but our data suggests increased Suezmax loads of these volumes as well.

This competition with Suezmaxes likely explains why Cross Mediterranean Aframax freight rates (TD19) have not risen much despite an 80% increase in volumes exported at Sidi Kerir m-o-m (Feb days 1-17). However, with operators keen to avoid Bab-el-Mandeb transits and long diversions, it is likely that Mediterranean Aframax demand will continue to benefit from high exports at Sidi Kerir.

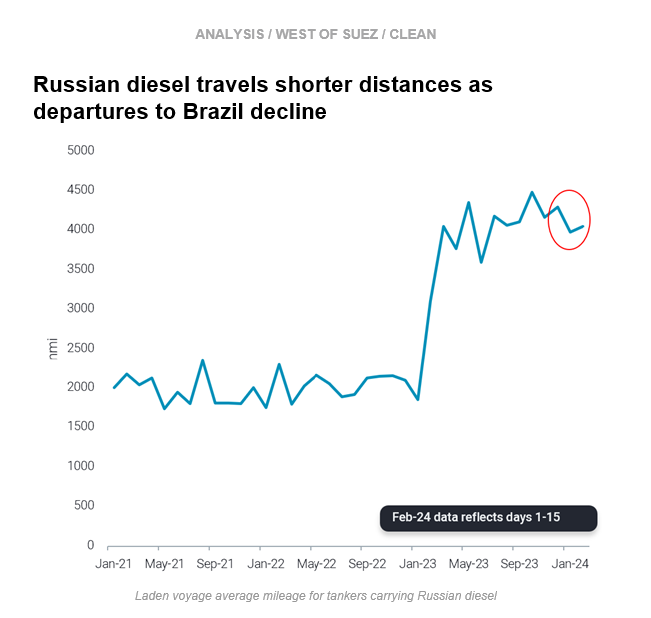

Average mileage for tankers carrying Russian diesel declined about 7% in January and February compared to December 2023. This is largely due to an increase in MEG-origin diesel exports to Brazil and the drastic decline in Russia’s diesel exports to Brazil in January, down 48% m-o-m. Russian exports to Brazil have increased in H1 February but are still down 35% compared to Dec-23.

At the same time, Russian diesel exports to the Mediterranean increased 25% m-o-m in January, and the relatively shorter distance of these journeys contributed to voyage mileage declines.

In January we observed the resumption of Russian diesel cargoes heading to Brazil via STS, the first in a year. This also significantly shortens voyage mileage for involved vessels, and will lead to further reductions in travelling distance if this trend continues.

Data Source: Vortexa