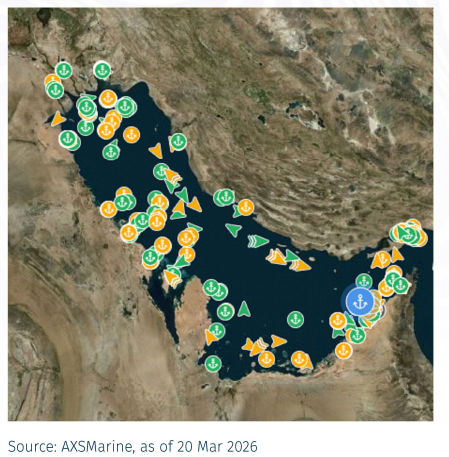

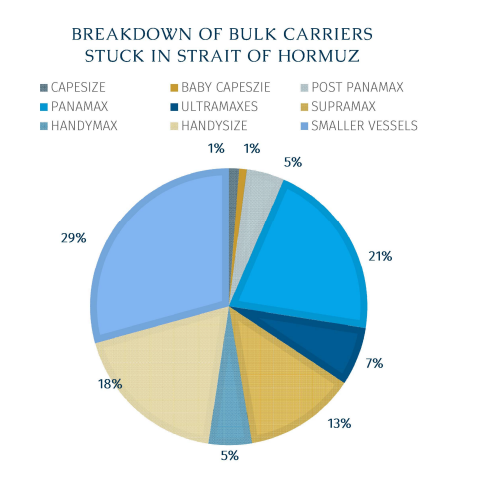

According to AXSMarine data, a total of 338 bulkers has been recorded in the Middle East Gulf. This includes 4 Capesizes, 3 Baby Capesizes, 15 Post-Panamaxes, 71 Panamaxes, 23 Ultramaxes, 44 Supramaxes, 17 Handymaxes, and 62 Handysize units, as well as 161 small bulkers. This situation is contributing to a tightening in vessel supply. As of writing, only one attack on bulkers has been reported, involving a 30,000-dwt vessel.

Immediate Impact

Much like the post-pandemic recovery in 2021, which stretched global supply chains beyond conventional assumptions, the ongoing Iran conflict is exposing new vulnerabilities in the dry bulk fleet- and in shipping more broadly.

This time, the pressure point is bunkers, specifically both price and availability.

Disruptions in a key energy corridor have affected around 20 mb/d—about 20% of global oil traded—especially disrupting heavy and medium-sour crude flows. With major export terminals impacted, crude prices have surged, pushing ICE Brent above $100/bbl. The shock has spread to Asia, where countries are seeking alternative supplies while some companies are issuing force majeure notices.

At the same time, marine fuel availability is becoming an emerging concern. Some operators have already reported difficulty performing on contracts due to challenges in sourcing fuel. In parallel, disputes over Bunker Adjustment Factor (BAF) clauses are creating additional friction in the spot market.

Meanwhile, this is particularly problematic for tramp shipping, where dry bulk vessels typically operate with minimal fuel buffers. In such a system, even short-term disruptions in bunker supply can quickly translate into operational constraints, particularly for larger ocean-going vessels that traverse longer distances.

Broader Impact

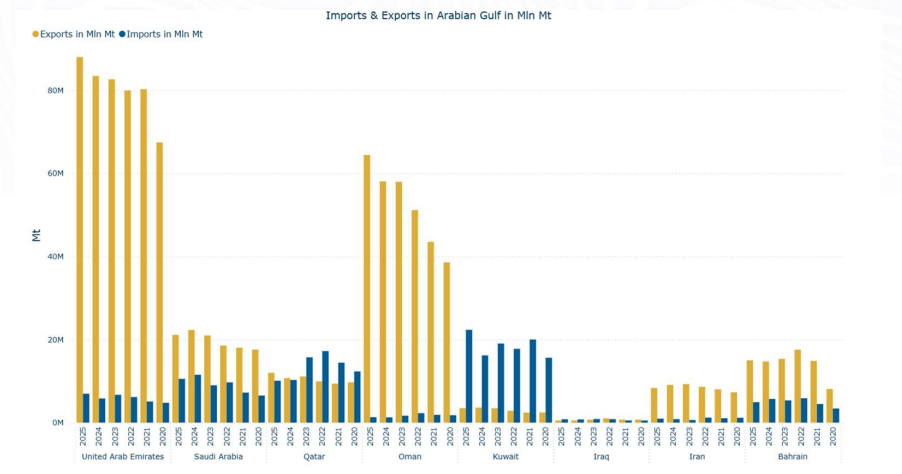

While headlines tend to be fixated on crude, followed by petroleum products, Middle East Gulf (MEG) has played a substantial role in the dry bulk sector with increasing activity. Overall, according to AXSMarine data, in 2025 Middle East shows an increased activity with imports and export totalling approximately 190 mln mt and 214 mln mt, respectively.

As a side note, the MEG is a vital repositioning region for vessels, connecting the Pacific basin to Atlantic, and vice versa. So, this will indirectly add some systematic inefficiencies to fleet positioning.

Should the situation in the Strait persist, the first in the firing line will likely come be UAE exports of limestone and aggregates. The UAE and Oman collectively account for around 75% of global seaborne limestone shipments in 2025.

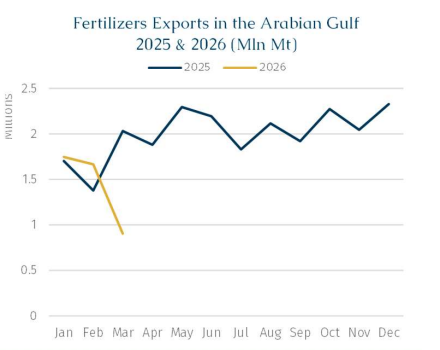

Fertilizers and grains should be the next markets affected. Countries in the MEG are among the world’s key suppliers of fertilizers - especially nitrogen, but also phosphates. Moreover, global energy and agricultural markets are closely interconnected through several channels:

Fertilizers: Natural gas is a critical input for nitrogen fertilizer production.

Fuel: Farming operations depend heavily on fuel for machinery, transport, and processing.

Biofuels: Crops such as corn, soybeans, and sugar are tied to energy markets through ethanol and biodiesel production.

If energy prices remain elevated, these linkages could transmit the shock across agricultural markets. In particular, farmers are facing higher agricultural production costs. As a result, these price spikes are adding further pressure on producers in the Southern Hemisphere, particularly when purchasing inputs.

Nitrogen fertilizer production is primarily associated with natural gas while certain biofuels are derived from crops such as soybeans, corn and sugar. In the biofuel sector, the RME index for biodiesel has recently been assessed around $299/t in the physical market, with paper market levels trading between $460–470/t, highlighting the link between geopolitical tensions affecting the agricultural sector and increased emphasis on biodiesel production.

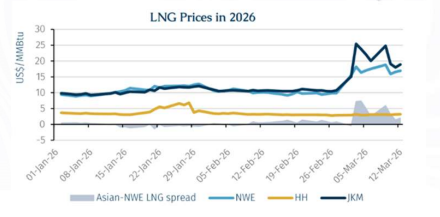

Potential Gas-to-Coal Switching?

Natural gas production disruptions in the region propelled natural gas prices sharply higher. As of writing, the JKM has risen to $25.39/MMBtu from $10.70/MMBtu pre-conflict, while NWE prices have reached approximately $18.93/MMBtu, up nearly 90% over the same period. Considering that 90% of crude exports from Hormuz head eastwards, the impact has been most pronounced in Asia, particularly in China (19.68%), India (11.83%), and Taiwan, China (8.37%).

In response to tightening energy supply, both European and Japan- South Korea- Taiwan, China markets have begun shifting away from gas and towards alternative energy sources, notably coal. Several countries have already reconsidered coal usage despite long-term decarbonization commitments. This has helped to propel coal process upwards given that it comes soon after the introduction of Indonesia’s RKAB policy aiming to manage production levels there. However, considering the conflict in the Middle East Gulf, the country just announced alterations in their policy in order to response to energy market turmoil. Additionally, Indonesia is planning to imply taxes to exports in order to boost their revenues, followed by the surge in demand.

Conclusion

From a pessimist’s perspective, container ships, bulk carriers, and tankers all rely on oil-derived bunker fuels to move goods across oceans.

If disruptions persist and the merchant fleet, from dry bulk to containers, continues to face operational constraints, the resulting headwinds experienced by various economies could eventually weigh on global demand for dry bulk commodities, atop of the drag imposed by the recent US tariffs and trade frictions.

For instance, in a scenario where persistently high energy prices persist, global industrial activity, particularly in China, could slow. A decline in manufacturing and construction would reduce steel output, weakening demand for iron ore and coking coal.

Conversely, from an optimist’s perspective, if the closure of the Hormuz strait was to de-escalate swiftly, within the next two weeks, for instance - the outlook could improve modeslty. A normalization in bunker markets may provide a modest recovery to dry bulk demand heading into the rest of 2026, as cargoes previously deferred or cancelled due to elevated voyage costs and bunker constraints return to the market and attempt to catch up.

Ultimately, duration risk aka the potential for political tensions, conflicts, or policy shifts to persist over an extended period, are invalidating the ability for “scenario planning” and will reward players who had operational resilience to withstand stresses.