The past few days have seen the conflict extend beyond chokepoint disruption into direct strikes on production and refining infrastructure across the Gulf. Following Israel’s attack on Iran’s South Pars gas field on Wednesday, Iran retaliated with drone and missile strikes on energy facilities in Qatar, the UAE, Saudi Arabia, and Kuwait. Qatar’s Ras Laffan industrial complex was targeted, and Abu Dhabi’s Habshan gas facility and Bab oil field were shut down. Drone strikes caused fires at Kuwait’s Mina Al-Ahmadi (346 kbd) and Mina Abdullah (454 kbd) refineries, with the former being struck repeatedly, forcing a shutdown of the refinery. The SAMREF refinery in Yanbu and Haifa refinery in Israel were also struck, with damage still being assessed. After a brief pause over the weekend, attacks on vessels continued this week, as a ship was struck off Ras Laffan, and another off Khor Fakkan. Since 28 February, the UKMTO has reported a total of 19 attacks on commercial vessels.

The Yanbu developments merit particular attention. Saudi Aramco briefly halted crude loadings at the port on Thursday following the SAMREF strike and the interception of a ballistic missile in the vicinity, before resuming operations. Yanbu is currently Saudi Arabia’s only functioning crude export outlet, and any sustained disruption there would remove the principal bypass route that the market has been relying upon since Hormuz closed, with VLCCs most exposed. The strike illustrated the acute vulnerability of oil exports via the Yanbu terminal.

Separately, Iran appears intent on formalising its grip on the Strait rather than relinquishing it. Reportedly, the IRGC is routing vessels through Iranian territorial waters between Larak and Qeshm islands, with passage subject to vetting and, in at least one case, a reported fee of $2m. Elsewhere, leading European nations and Japan have signalled readiness to support efforts to ensure safe passage through the Strait of Hormuz, though few details were reported.

The most notable policy developments came from the US administration. Treasury Secretary Bessent stated that the US may, in the coming days, lift sanctions on approximately 140 million barrels of Iranian crude currently stranded on tankers. If implemented, sanctioned Iranian crude, carried by dark fleet VLCCs, would become available to a broader set of buyers. Further, the previously rumoured lifting of the Jones act was confirmed this week, as Trump issued a 60-day Jones Act waiver on Wednesday 18 March, allowing foreign-flagged vessels to carry energy products between US ports. For MRs especially, this supported further strength in MR rates out of the US Gulf over the past week.

On a more constructive note, Iraq and the Kurdistan Regional Government agreed on Tuesday to resume Kirkuk crude exports to Ceyhan via pipeline. Initial flows of 170 kbd are projected to gradually ramp up to 250 kbd. The volume does little to address the broader shortfall, but Suezmaxes and Aframaxes loading in the Mediterranean stand to benefit.

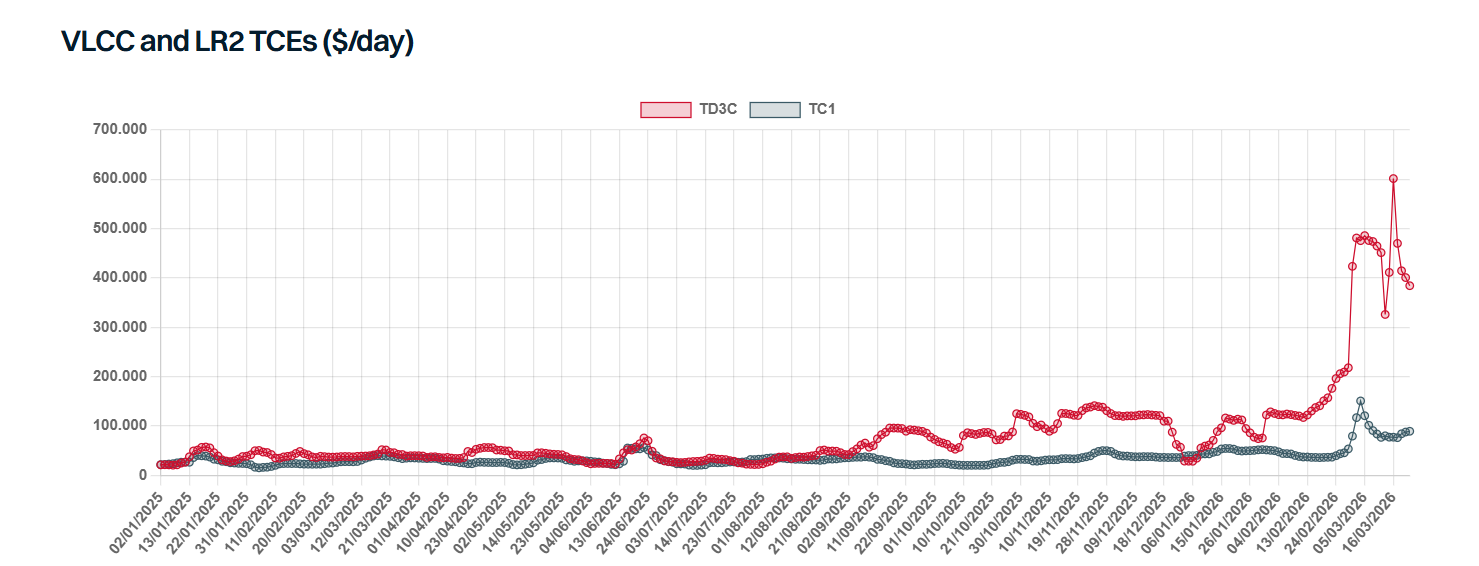

Oil prices remained highly volatile this week, with sharp moves in both directions. At the time of writing Brent is up 7% week on week. Notably, the WTI-Brent spread widened to extreme levels towards the latter half of the week, briefly reaching over -20$/bbl before declining to -14$/bbl, making WTI by far the cheapest crude globally and contributing to sharp increases in TD25 and TD22. Refining margins also continued their inexorable rise, as especially gasoil and jet pricing extended their gains. As a result, arbs are shifting rapidly, with clean barrels out of the UK/Continent and the US Gulf the most attractive globally. Crude exports out of Yanbu have picked up significantly, with March so far averaging over 2.5mbd of Arab Light vs. circa 800 kbd in February, with potential for further gains judging by volume of spot VLCC fixtures for loading this month.

Oil on water levels have declined sharply this month, with crude/DDP down to its lowest since Sep-25 and clean since Jun-25. Volumes held on larger LR2s and VLCCs have seen the sharpest correction (down to their lowest level since May-21 and Nov-24 respectively).

So, what’s next for tanker markets? There is some hope that the increased escalation we saw this week marks the top in attacks on oil infrastructure. Over the last 24 hours a few de-escalatory statements have been reported from the US and Israeli administrations, though no such statements have come from the Iranian side. However, even if the crisis ends, damage incurred on infrastructure could take a significant amount of time to repair, and thus for flows to return to normal. A continued standoff or further escalation are likely to have a bearish impact on the tanker markets overall, due to heavily restricted clean and dirty flows. If refinery output declines and protectionist efforts continue, especially in the East, flows could shrink further. Any further disruptions of the Yanbu export terminal will make VLCCs even more vulnerable. On the other hand, as outlined in our report last week, a stabilisation of the situation in the Middle East offers a more positive outlook in the longer run, with incremental flows and pent-up demand offering support.

Data source: Gibson Shipbrokers