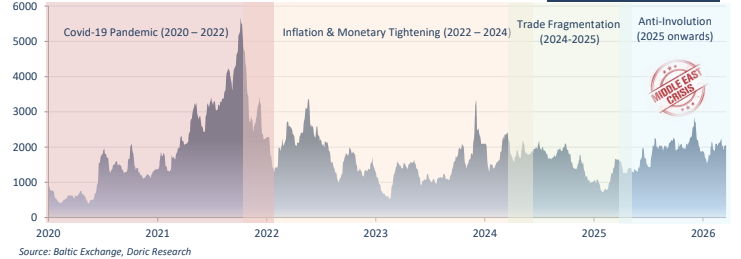

The global economic landscape has undergone a profound transformation over the past five years, shaped by a succession of defining phases that have fundamentally altered market dynamics, policy direction, and trade behaviour. From the abrupt dislocation of the pandemic to the inflationary surge and subsequent monetary tightening, and more recently to increasing geopolitical fragmentation, the global economy has transitioned into a more complex and less predictable environment.

The first phase, marked by the outbreak of Covid-19 in early 2020, triggered an unprecedented shock to the global economy. Supply chains were abruptly disrupted, labour mobility collapsed, and demand for key commodities declined sharply, reflecting the steepest contraction in activity since the Great Depression. The crisis exposed the deep interdependence of global trade networks, with disruptions in one region rapidly cascading across continents. For the shipping industry, the immediate impact was severe, with cargo volumes declining and uncertainty dominating market sentiment. However, as economies gradually reopened, a powerful rebound in demand emerged. This recovery was characterised by strong restocking activity and a surge in consumer demand, which in turn drove freight rates sharply higher. At the same time, persistent congestion and logistical bottlenecks across major ports and trade routes contributed to rising costs, laying the groundwork for the inflationary pressures that would define the next phase.

By 2022, the global economy had entered a second distinct phase, characterised by persistent inflation and an aggressive shift in monetary policy. What was initially perceived as a transitory imbalance between supply and demand evolved into a more entrenched inflationary environment, driven by elevated commodity prices, supply chain inefficiencies, and robust post-pandemic demand. Central banks responded decisively, implementing the most aggressive tightening cycle in decades in an effort to anchor inflation expectations. Policy rates were raised rapidly across major economies, while liquidity was withdrawn from financial systems. Despite these significant headwinds, the global economy demonstrated a notable degree of resilience. Consumption remained relatively firm, labour markets proved more robust than anticipated, and trade volumes continued to expand, albeit at a more moderate pace. Within the shipping sector, this resilience translated into sustained demand for both commodities and manufactured goods. The period highlighted the sector’s adaptability, as it navigated tighter financial conditions while continuing to facilitate global trade flows.

The third phase has been defined by increasing fragmentation in global trade and a rise in geopolitical tensions. What began as targeted tariff disputes between major economies has evolved into a broader reconfiguration of global supply chains. Efficiency-driven models, which had previously prioritised cost optimisation and scale, are increasingly being replaced by strategies focused on resilience and security of supply. This shift has led to a reorientation of trade patterns, with a growing emphasis on regionalisation and diversification of sourcing. Commodity flows have become less predictable, as traditional trade routes are supplemented or replaced by alternative corridors. For the shipping industry, this has introduced both challenges and opportunities. While uncertainty has increased, the reconfiguration of supply chains has also generated new tonne-mile demand in certain segments, as cargoes are routed through longer or less direct pathways.

Looking ahead, the global economy appears poised to enter a new phase shaped by two key themes: structural adjustments within China and evolving geopolitical risks in the Middle East. In China, the introduction of the “anti-involution” policy marks a significant shift in industrial strategy. After decades of rapid expansion, many sectors are now characterised by excess capacity and weak profitability, leading to intense price competition. The government’s response has been to promote consolidation, enforce stricter regulatory oversight, and encourage a transition towards higher value-added production. In the near term, these measures may result in tighter capacity and, consequently, a moderation in demand for certain raw materials. However, over the longer term, a more balanced and sustainable industrial framework could support greater stability in commodity demand and trade flows.

At the same time, geopolitical developments in the Middle East are emerging as a critical variable for global trade and shipping. Recent tensions have already begun to affect vessel movements through key chokepoints such as the Strait of Hormuz. While the direct exposure of the dry bulk sector to this route is relatively limited – particularly when compared to the tanker and LNG markets – the indirect implications are potentially far more significant. In the event of a prolonged escalation, higher energy prices, particularly for oil and LNG, would have broad-based effects on the global economy. Increased fuel costs would raise production and transportation expenses, potentially delaying the pace of monetary easing and weighing on industrial activity. Under such a scenario, the resulting tightening of financial conditions and moderation in economic growth could exert downward pressure on commodity demand. Conversely, a more contained or short-lived disruption could generate a different set of dynamics. Higher bunker costs may encourage slower steaming, effectively reducing available vessel supply, while logistical disruptions and regional inefficiencies could create dislocations in trade flows. Historically, such conditions have tended to support freight markets, as inefficiencies translate into increased tonne-mile demand and tighter vessel availability. Ultimately, the magnitude of the impact will largely depend on the duration and the intensity of the conflict as well as the nature and duration of disruptions.

In this increasingly complex environment, the defining characteristic of the global economy is its heightened exposure to unexpected shocks. As the Managing Director of the IMF aptly noted, “we live in a world with more frequent, more unexpected shocks. Most of the time we cannot predict exactly what they will be – but we can always strive to be prepared.”

Data source: Doric