Spotlight | Dirty vs. Clean tanker freight sentiment

Tanker freight markets continue to diverge, with dirty segments losing momentum, while clean markets retain a firmer undertone.

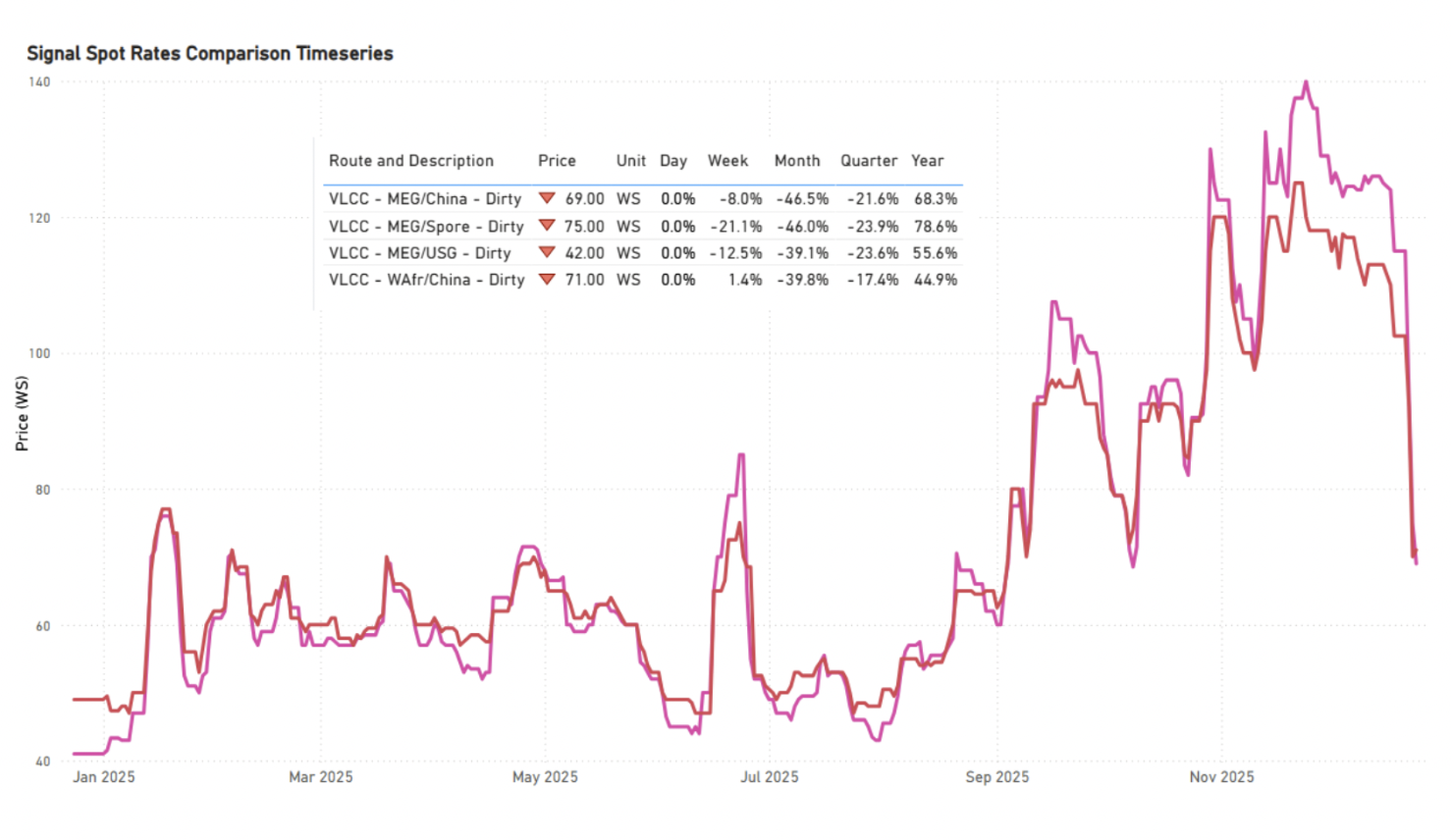

Dirty Freight Market Sentiment

VLCC MEG- China Weaker

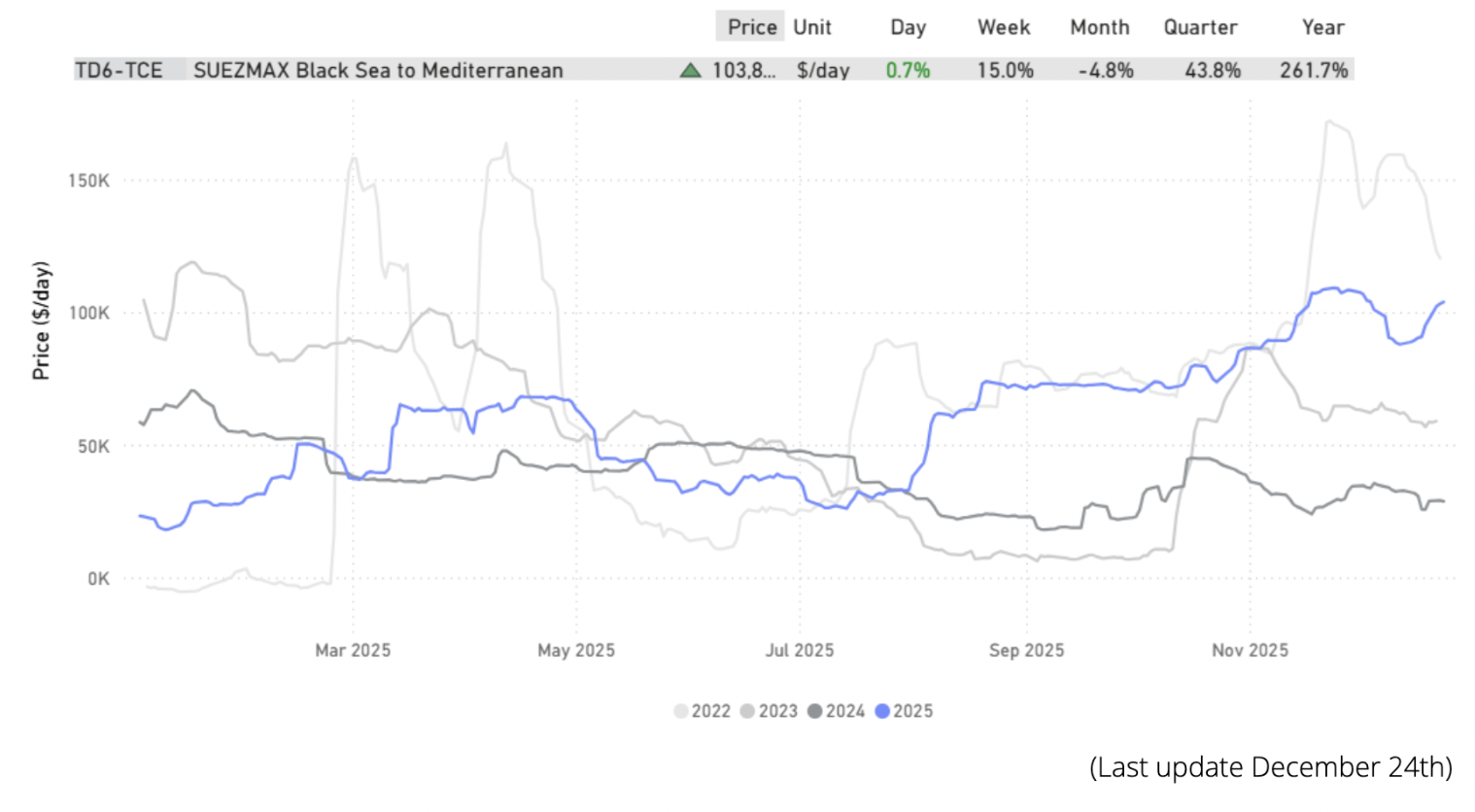

Suezmax Black Sea - Med Firmer

Aframax Cross Med Weaker

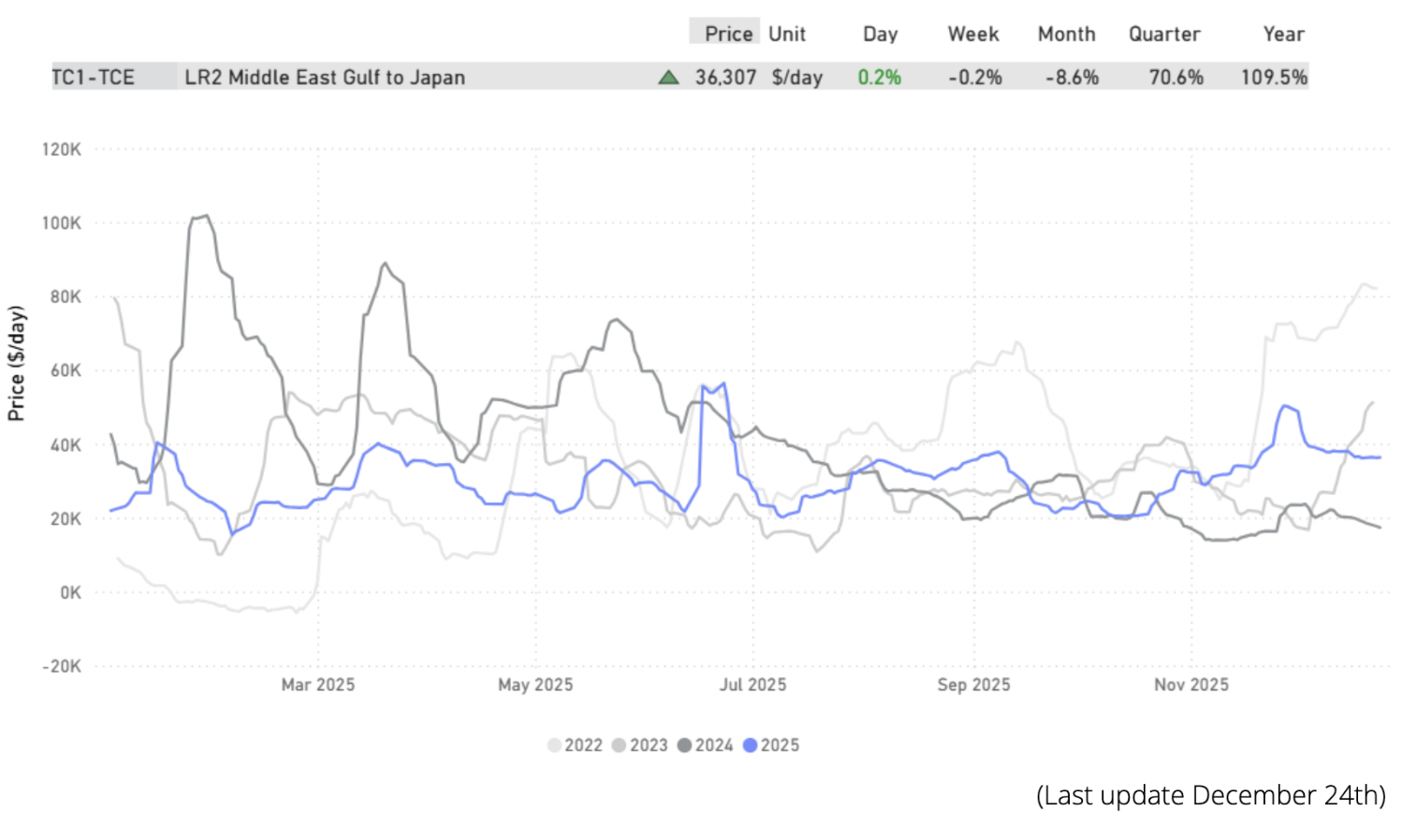

LR2 MEG - Japan Steady

Dirty Market Signals

(WS | Ballast Positioning | Demand Volumes)

What current fundamentals imply for the days ahead

VLCC Weaker

Signal Assessment Overview

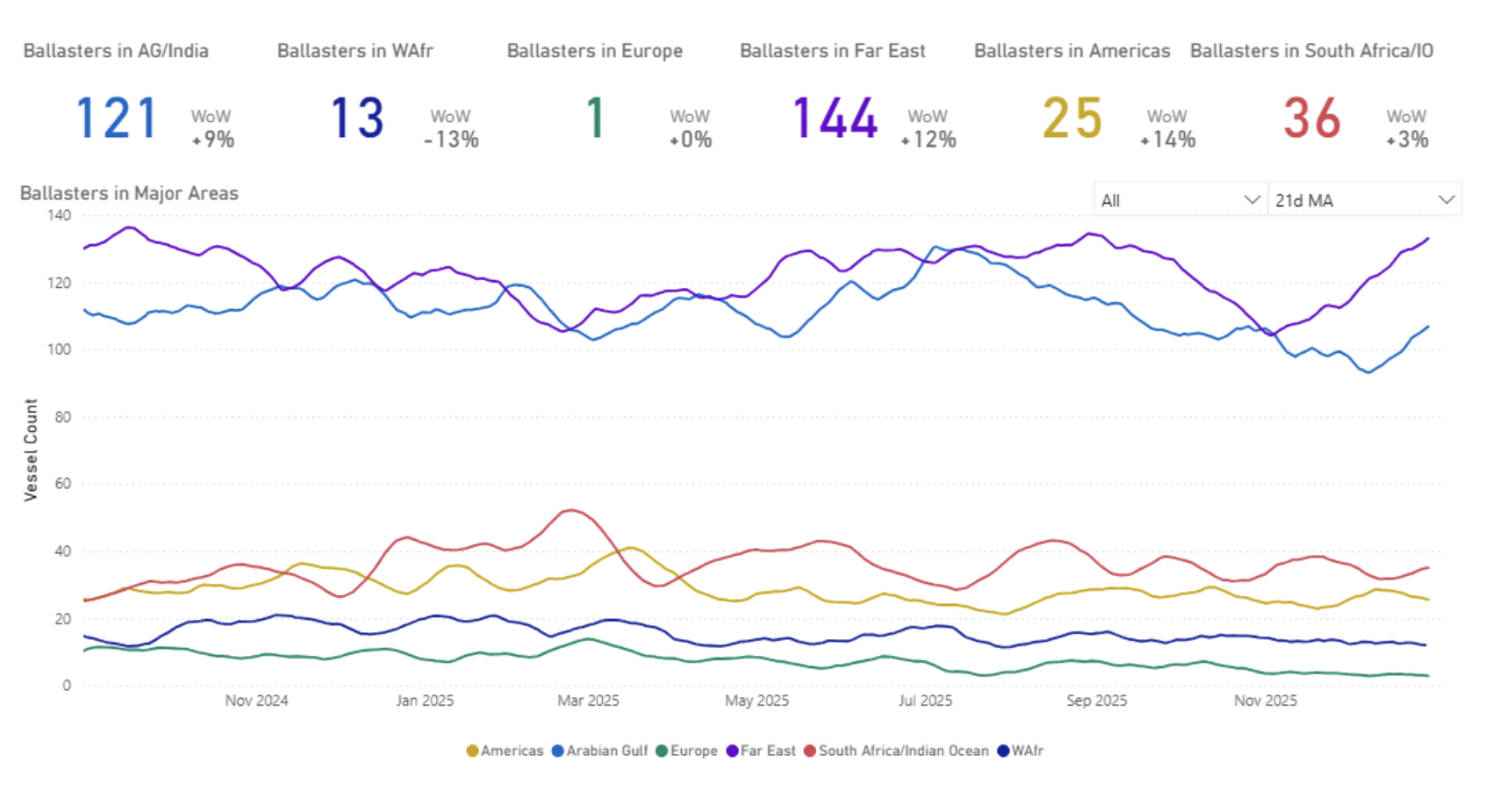

Ballasters| AG & WAFR Supply Building

Bearish for near-term freight

An increase in VLCC ballast availability in AG and West Africa is weighing on freight momentum into year-end, keeping rates under pressure in the near term.

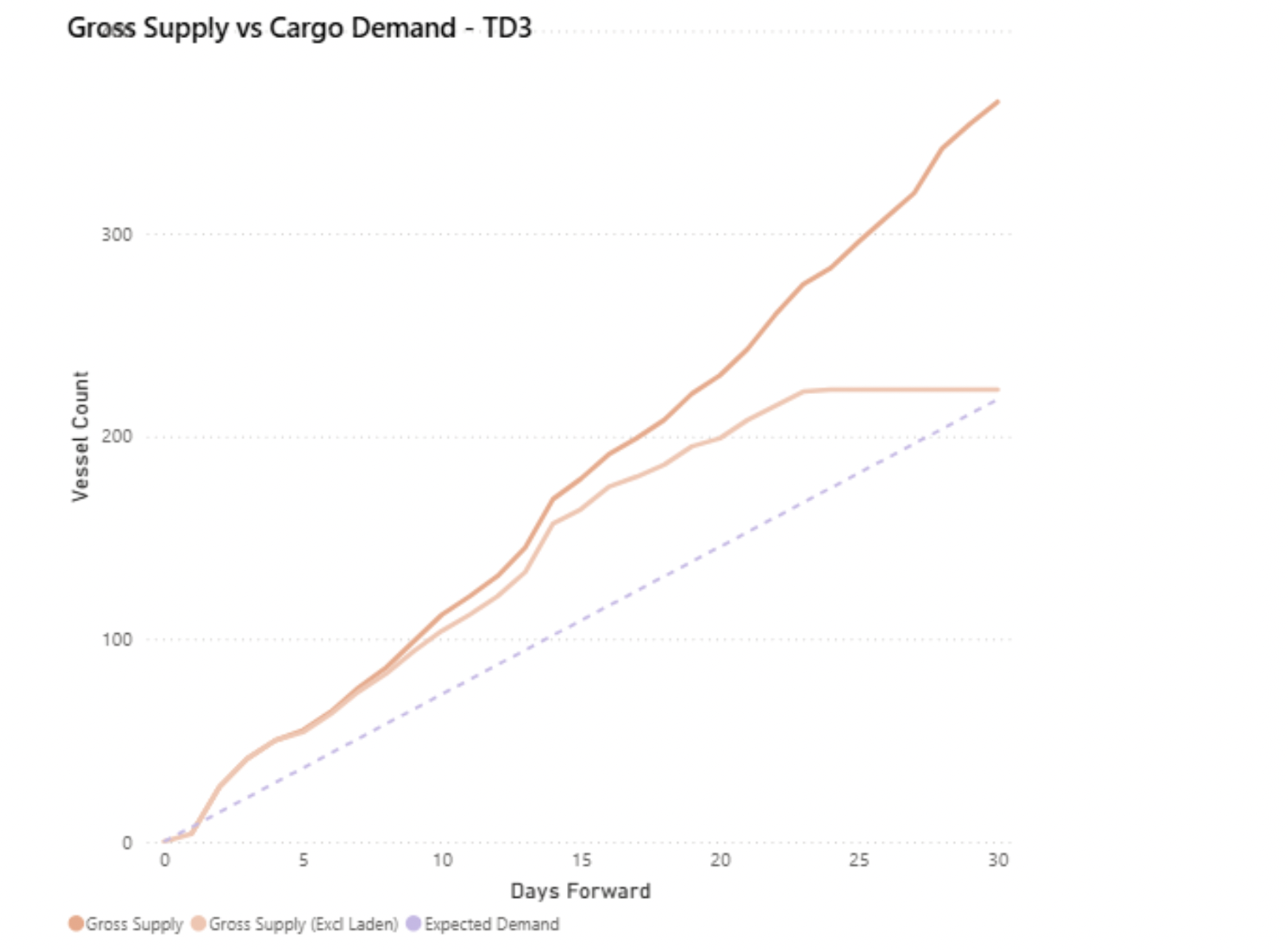

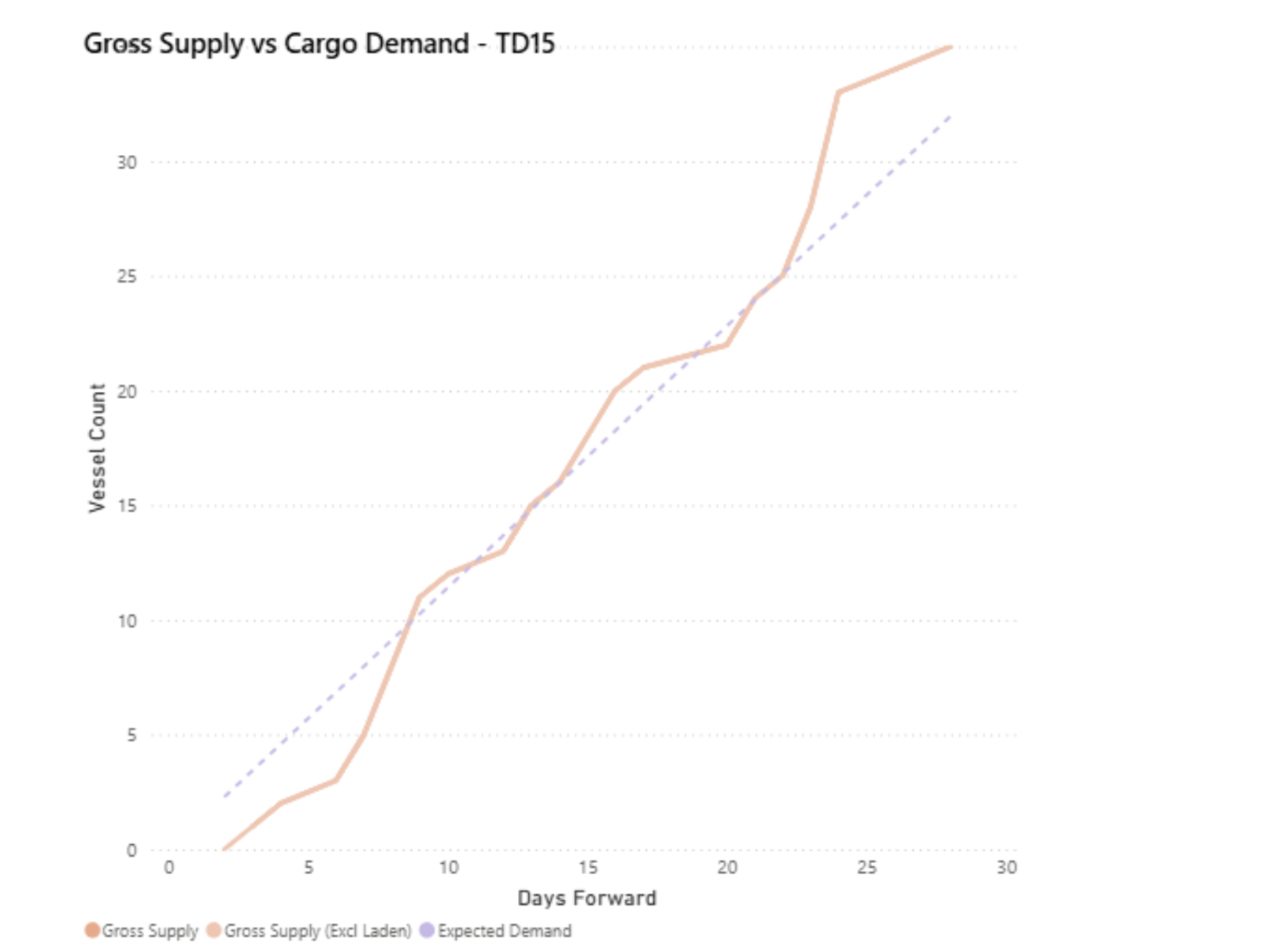

Gross Supply Vs Cargo Demand |TD3 & TD15

The primary concern for the VLCC market approaching year-end is the noticeable disparity between the gross vessel supply and the anticipated cargo demand. Forward curves indicate that the rate of supply growth is expected to outpace demand in the coming weeks, particularly on the TD3C and TD15 routes.

Supply vs Demand

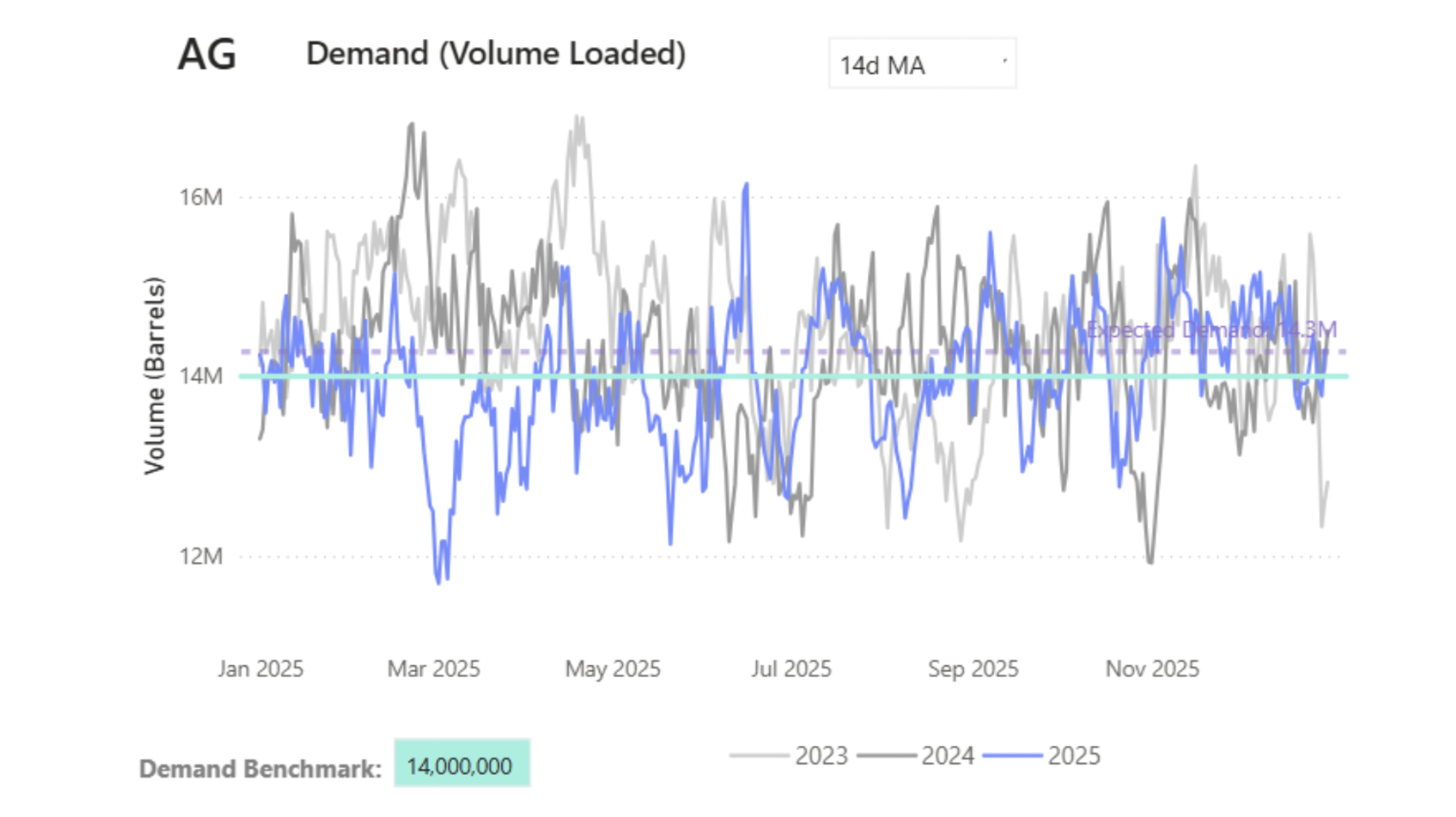

Demand (Volume Loaded) | TD3C

Lack of incremental volume growth caps freight support

TD3C loaded volumes are tracking close to the long-term benchmark (~14.0 mbbl). With 2025 activity yet to show meaningful incremental volume growth, and tonne-day generation gradually easing as voyage durations normalise, the scope for sustained upward pressure on freight rates appears limited.

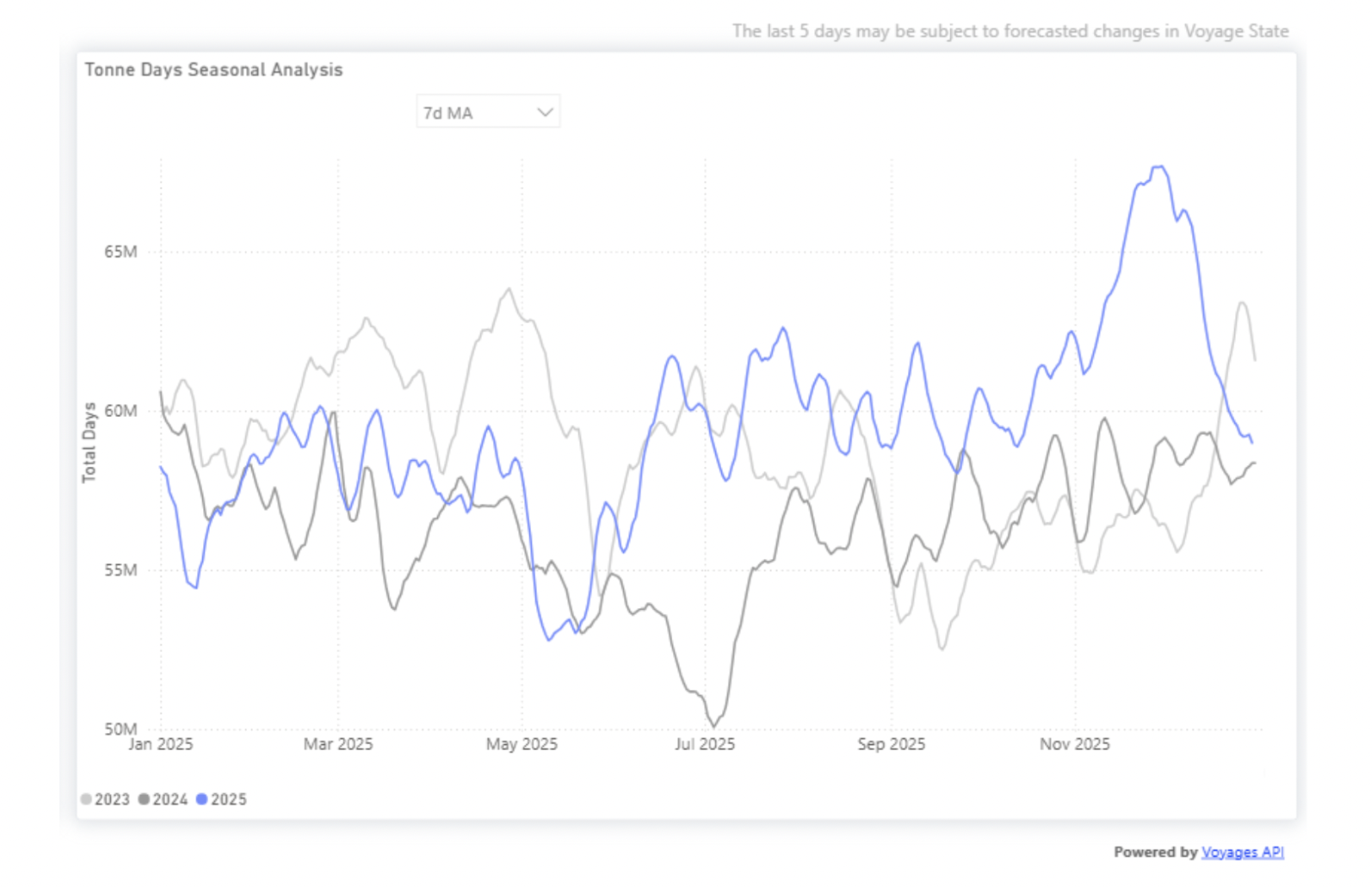

VLCC Tonne Days | AG to Far East

Momentum fading after recent highs

VLCC tonne-days peaked earlier in the quarter and, while still at relatively high levels, have moderated in recent weeks. This easing in momentum has coincided with a softer rate environment toward year-end.

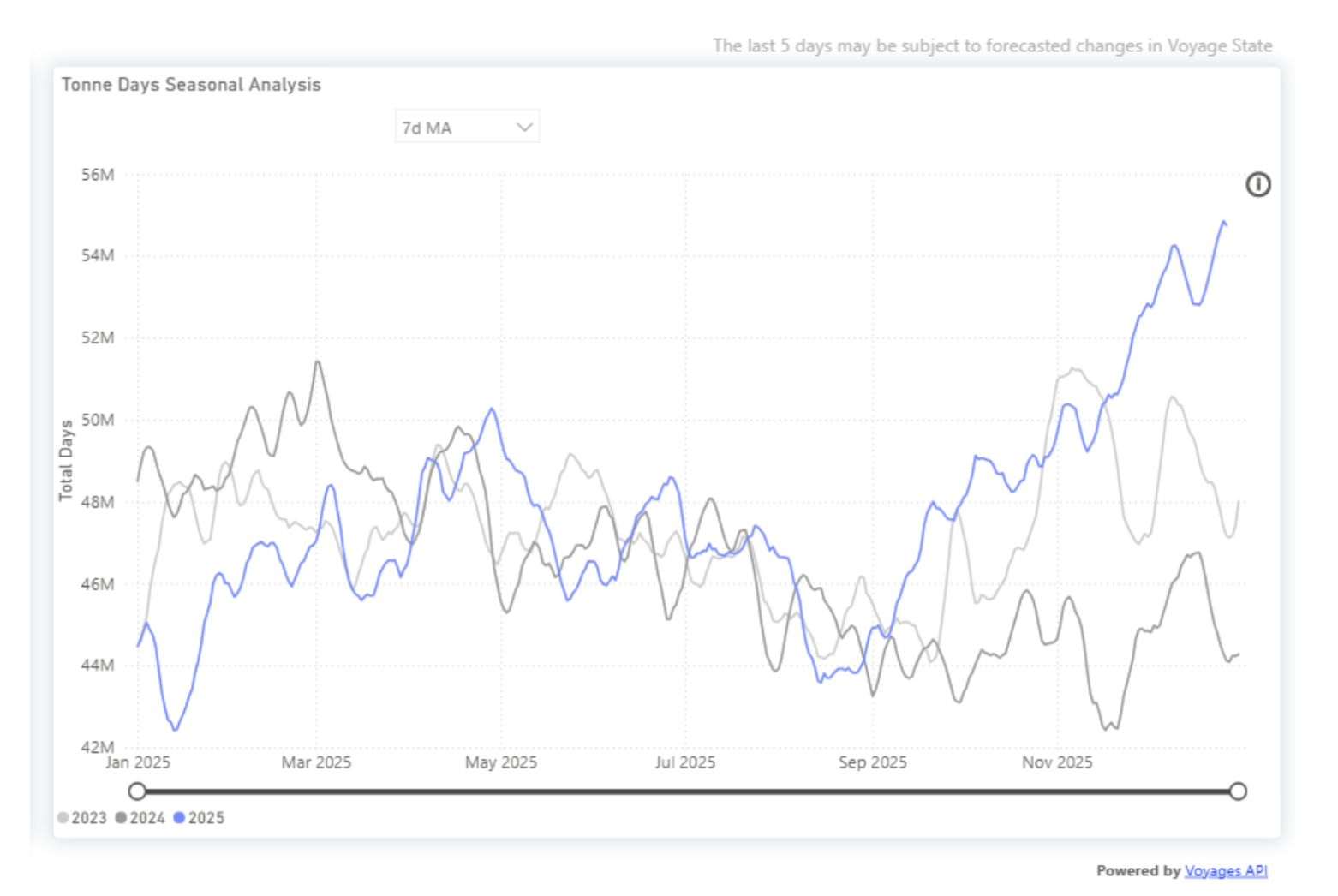

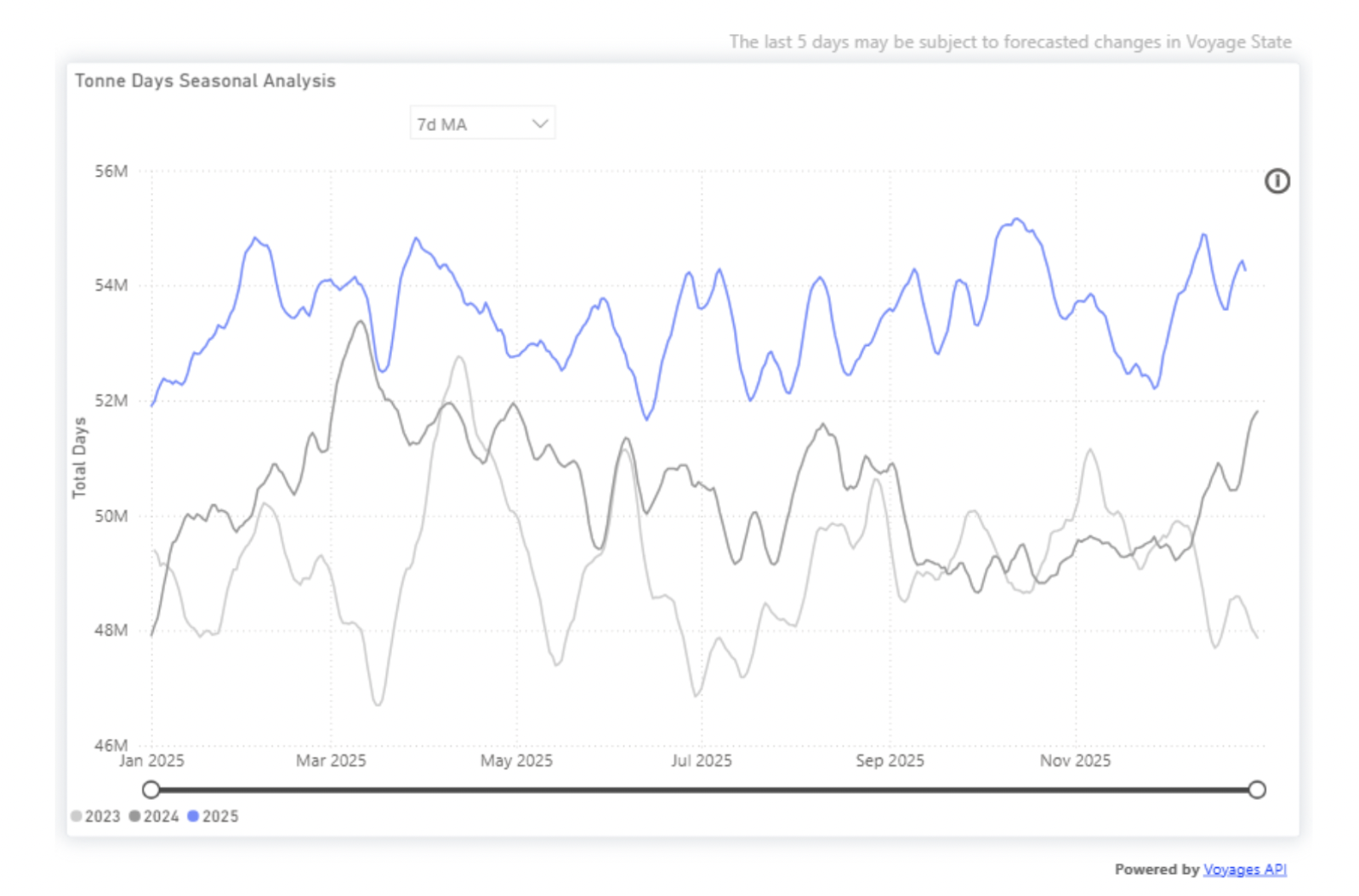

Firmer Tonne-Day Trends | Dirty Aframax & Clean MR

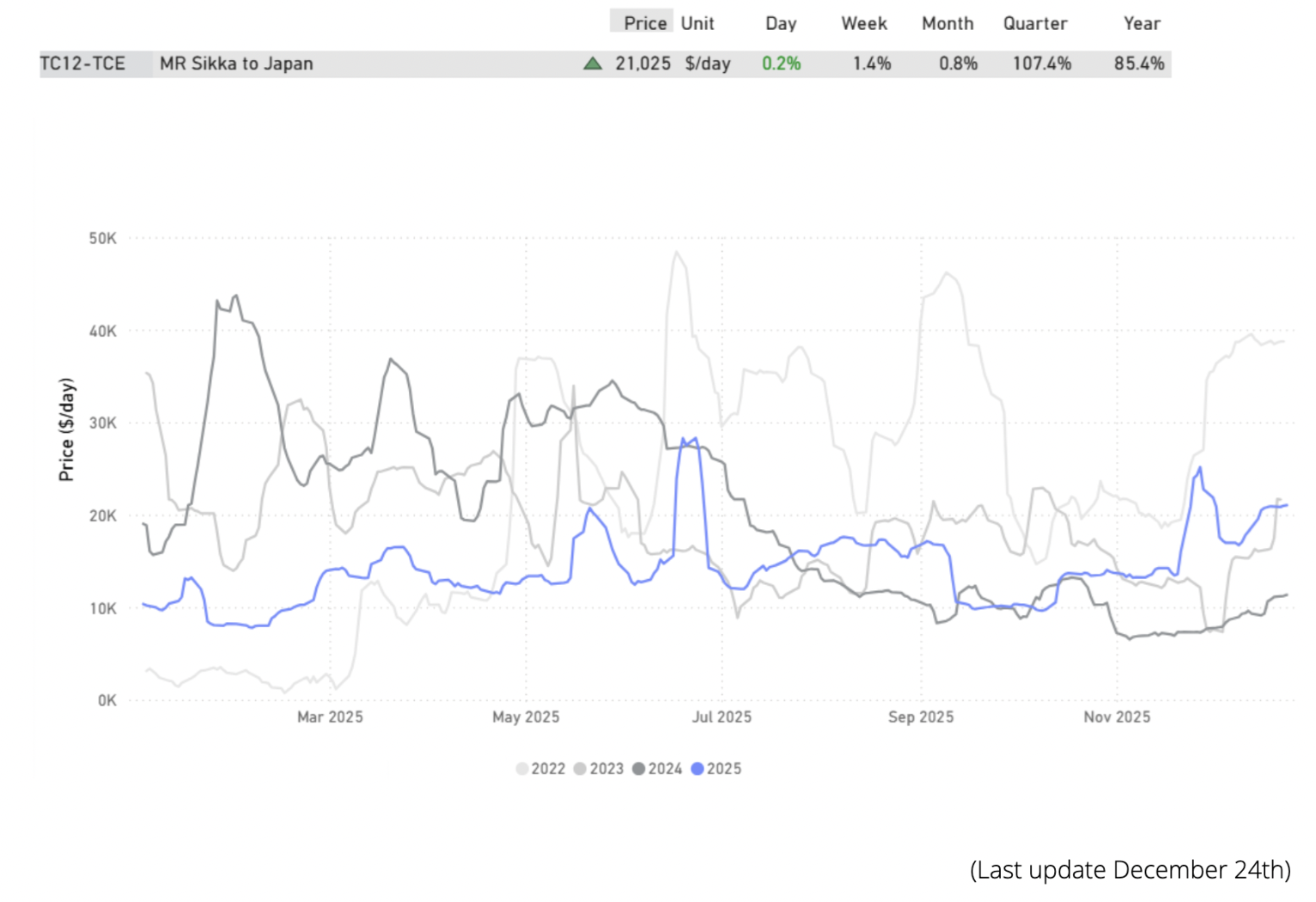

In Dirty Aframax and Clean MR, elevated tonne-days point to improving utilisation and a healthier market balance heading into year-end.

DIRTY AFRAMAX

CLEAN MR

Takeaway

As the year draws to a close, tanker markets are becoming more differentiated. VLCCs are facing near-term pressure amid rising supply and moderating tonne-day momentum, while clean and mid-size segments appear to show fewer signs of near-term softening.

Data Source: Signal Ocean Platform