Tanker - Weekly Market Monitor

Snapshot of Crude and Product Freight Rates, Supply-Demand

Week 19, 08 May, 2025

In the second quarter of 2025, oil flows from Saudi Arabia to China declined sharply. This downturn can be attributed to a combination of seasonal and structural factors. Notably, Chinese refineries traditionally undergo scheduled maintenance during Q2, particularly in April and May. This maintenance period temporarily reduces the country's crude oil demand, decreasing import volumes. Additionally, inventories that had been stockpiled in the first quarter were likely drawn down, as Chinese importers had proactively increased purchases ahead of anticipated market shifts, such as price hikes or supply disruptions. This front-loading of imports occurred just as a key development unfolded in global oil supply. In late April 2025, OPEC+ announced it would begin gradually unwinding its voluntary production cuts, starting in June with an additional 411,000 barrels per day of crude entering the market. The timing suggests that importers may have been positioning themselves ahead of expected changes in supply dynamics. The bloc's leading producers, Saudi Arabia and Russia spearheaded this decision. The move was motivated by a desire to regain market share and stimulate global demand, particularly as oil prices had begun to soften amid economic uncertainties.

Following the OPEC+ announcement, crude oil prices fell significantly. Brent crude experienced its steepest monthly decline since November 2021, dropping nearly 9% in April alone. This brought prices below the key $80 per barrel threshold, reflecting bearish market sentiment. Analysts now forecast that Brent will remain under pressure for the rest of 2025, with average prices expected in the $75–78 range. Looking ahead into 2026, institutions such as Goldman Sachs, JPMorgan, and the International Energy Agency (IEA) project continued price softness due to sluggish industrial growth in China and Europe, rising output from non-OPEC producers—especially U.S. shale—and potential oversupply if OPEC+ compliance erodes.

Despite the Q2 downturn, there is reason to expect a recovery in Chinese crude oil imports in the second half of 2025. Several large refining projects, including Zhejiang Petrochemical Phase II and Shenghong Petrochemical, are scheduled to ramp up operations in the coming months. This will increase the country's crude throughput and necessitate higher feedstock imports. Additionally, the Chinese government is preparing new economic stimulus measures focused on manufacturing and infrastructure, both energy-intensive sectors. These measures are likely to support domestic demand for refined products and, by extension, crude oil imports.

Moreover, if crude prices remain subdued, particularly under $75 per barrel, China may seize the opportunity to replenish its strategic petroleum reserves. While Beijing continues to diversify its sources of crude, increasing purchases from Russia, the UAE, and potentially Iran, it remains highly price-sensitive. Should Saudi Arabia offer competitive pricing and favorable contract terms, Chinese refiners could resume or even expand purchases from the Kingdom in the latter half of the year.

Amid a sustained downturn in global oil prices—Brent crude recently fell below $60 per barrel due to increased OPEC+ output and subdued demand—China may find an opportune moment to bolster its strategic petroleum reserves. However, recent U.S. sanctions targeting Chinese independent refiners, specifically Shandong Shouguang Luqing Petrochemical and Shandong Shengxing Chemical, for importing Iranian oil have disrupted operations and deterred other refiners from similar purchases. Despite these challenges, China's commitment to diversifying its crude sources remains evident, with continued imports from Russia, the UAE, and other nations. Should Saudi Arabia offer competitive pricing and favorable contract terms, Chinese refiners may resume or even expand purchases from the Kingdom in the latter half of the year.

In summary, the Q2 2025 decline in Saudi oil flows to China reflects a mix of seasonal demand reduction, strategic inventory adjustments, and evolving global supply dynamics. The OPEC+ decision to raise output has introduced downward pressure on prices, while geopolitical and macroeconomic uncertainties continue to influence global demand. However, signs point to a possible rebound in Chinese imports from Saudi Arabia later in the year, contingent on refinery utilization, economic stimulus, and the relative attractiveness of Saudi crude compared to other suppliers.

Crude oil tanker freight market sentiment weakened in the second week of May. The Suezmax segment indicated a more pronounced downward trend compared to the start of the month.

VLCC freight rates on the MEG–China dropped to WS 60, reflecting a 12% weekly decrease. Meanwhile, Suezmax rates from West Africa to continental Europe dropped below WS100, showing an 18% weekly decrease. Meanwhile, rates on the Baltic–Mediterranean route dropped to WS110, standing 17% lower than a week ago.

Aframax freight rates in the Mediterranean dropped below WS170, showing 7% weekly decrease.

LR2 AG freight rates dropped to WS110, reflecting a monthly drop of 25%.

Panamax Carib-to-USG rates showed a slight upward trend, reaching approximately WS180. However, these rates are still 10% lower compared to the levels observed a month prior.

MR1 freight rates for Baltic-to-Continent shipments hovered around WS140, representing a 7% monthly decrease.

MR2 freight rates for shipments from the Continent to the US Atlantic Coast (USAC) reached WS125, a 15% monthly decrease. Meanwhile, MR2 rates from the US Gulf to the Continent remained stable around WS110, consistent with the previous week's sentiment and levels observed a month prior.

The upward pressure observed at the close of April intensified in early May, with the first week of the month showing a significant increase from the lows of two weeks prior.

VLCC Ras Tanura: The current number of ships has exceeded the yearly average by 26 vessels. It remains uncertain if this significant rise will persist as we progress beyond the first ten days of May.

Suezmax Wafr: The current ship count (around 120) is double the annual trend, showing a sharp increase that, if sustained, could negatively pressure market sentiment.

Aframax Med: The current number continues with a downward trend, still well below the annual benchmark of 10.

Aframax Baltic: The current number of ships is approximately 30, an increase of nearly 7 vessels compared to the end of last week. This figure is now only 2 ships below the annual average.

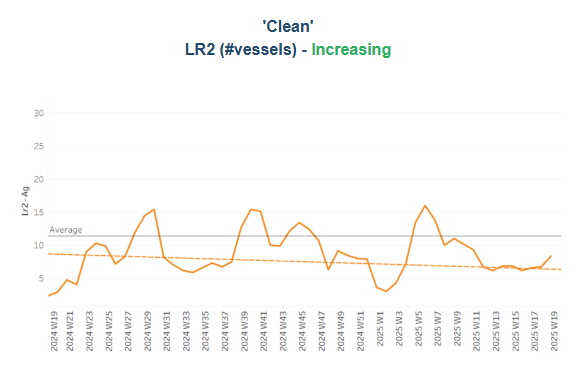

Clean LR2 AG Jubail: Amid levels hovering below the annual average of 11, the vessel count has started to show signs of a soft increase from the end of April.

Clean MR: Skikda, Algeria, experienced a significant increase in MR1 vessel calls, reaching 43, which is over ten more than the annual average. This elevated activity mirrors the previous week's levels. In Amsterdam, MR2 vessel calls continue to trend upwards, exceeding the yearly average of 32 for the third straight week, indicating ongoing growth in vessel traffic this May.

Dirty tonne days: Tonne-day growth is sharply declining in early May, particularly for VLCCs. Aframax tonne days are also trending downwards after a brief recovery two weeks prior. Suezmax tonne-day growth remains near its annual average for over six weeks, with the last peak occurring at the end of week 11.

Panamax tonne days: Over the past seven weeks, the growth rate has remained below this year's weekly average, in contrast to the end of Week 8, when levels were close to surpassing the annual average.

MR tonne-days: The growth rate in the MR segment has been steadily decreasing since the end of Week 5, and this downward trend has continued through the first half of the current month without any indication of recovery.

Data Source: Signal Ocean Platform