As the year concludes, China is reaffirming its commitment to strengthening raw-material security by accelerating domestic iron-ore development. The China Iron & Steel Association (CISA) has issued directives urging producers to speed up mine construction and modernization to expand long-term supply capacity. The policy objective remains clear: reduce structural dependence on imported ore. In this week’s review, Allied Quantumsea Research assesses the implications of these measures and outlines future scenarios, including the rising influence of bauxite on tonne-mile demand and Capesize utilization.

Policy Directive and Domestic Production Performance

Despite sustained policy initiatives aimed at improving domestic resource security, China’s iron-ore industry continues to fall short of official production objectives. Between January and October 2025, output of iron-ore concentrate totalled approximately 851.7 million tonnes, representing a year-on-year decrease of 3.2 percent. This decline underscores persistent challenges, including diminishing ore grades, fragmented industry ownership, and slow rates of capital investment. These factors collectively constrain the sector’s capacity for increased production, further widening the gap between strategic targets and operational outcomes. As a result, it is unlikely that domestic mining will substantially influence China’s iron-ore supply outlook in the foreseeable future.

Import Dynamics and November 2025 Developments

Between January and November 2025, China imported approximately 1.14 billion tonnes of iron ore, maintaining its trajectory for another record-breaking year. According to the General Administration of Customs, November’s arrivals reached 110.54 million tonnes, a 0.7 percent decline from October, marking the second month in a row of decreasing imports. While November’s figure dipped from October’s 111.3 million tonnes, it remained substantially higher than the 101.86 million tonnes brought in during the same period last year.

The slowdown in November was mainly due to reduced purchasing appetite, as more steel mills undertook equipment upgrades and furnace maintenance to adjust to shrinking profit margins. Nevertheless, the overall volume of imports continues to feed the supply chain. By Week 49 of 2025, portside inventories have climbed to more than 153 million tonnes, the highest since 2018 and well above the mid2025 low. This accumulation highlights the limited contribution of domestic mining to China’s immediate iron-ore needs and underscores the country’s ongoing dependence on seaborne imports to maintain supply.

Drivers of Continued Import Dependence

China’s iron ore imports are driven primarily by grade requirements. Australian and Brazilian iron ore grades typically in the 62–65% Fe range. This high-grade material aligns with the needs of China’s blast furnaces and underpins efficient, stable steel production. In contrast, China’s domestic iron ore resources contain much lower iron content, averaging only 30–40% Fe. New high-grade sources, such as the Simandou project in Guinea, expected to produce ore around 65% Fe, underscore the global scarcity of premium-grade deposits and highlight why China continues to look abroad for high-quality supply.

China’s domestic ore, with its low iron content and high impurities, cannot meet the requirements of modern blast-furnace operations on its own. To achieve the necessary sinter-feed chemistry and maintain stable furnace performance, steelmakers use domestic material only after beneficiation and then blend it with higher-grade imported fines. This blending raises the effective grade, improves fuel efficiency, and supports consistent output. High-grade imports are therefore essential for keeping China’s steel production efficient, cost-effective, and technically reliable.

Impact on Seaborne Trade and Freight Market Evolution

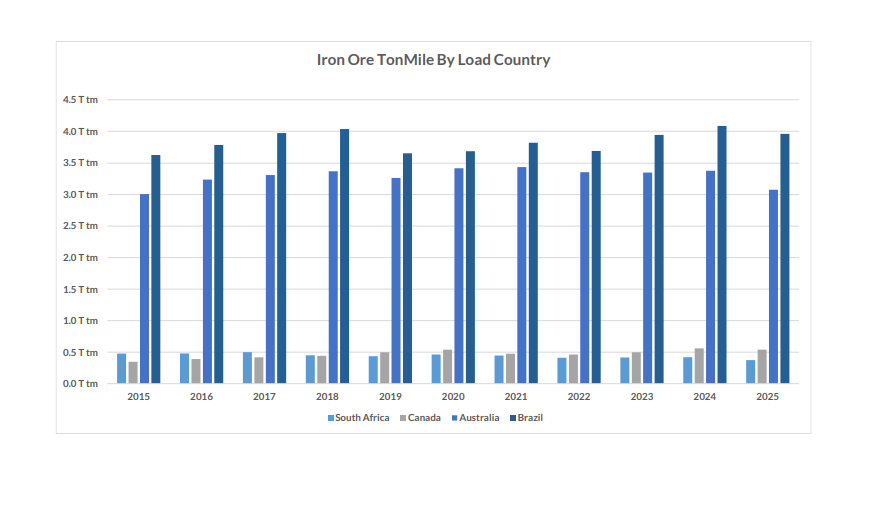

China’s sustained import levels continue to shape global iron-ore shipping flows. Australia and Brazil remain the dominant exporters, generating 29.5 trillion and 30.8 trillion tonne-miles respectively in 2025. Brazil’s contribution exceeds Australia’s despite fewer voyages, reflecting the longer haul distances involved. These patterns underline the continued significance of long-haul routes in Capesize employment.

Tonne-mile Composition: Bauxite Vs Iron Ore

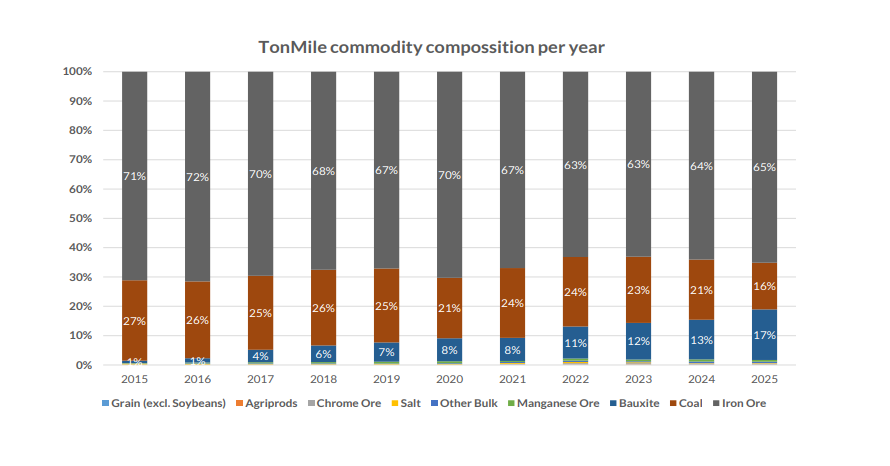

Before 2020, iron ore accounted for an average of approximately 70 percent of Capesize tonne-mile demand, reflecting the dominance of China’s steel expansion cycle and heavy sourcing from Brazil and Australia. Beginning in 2020, iron ore’s share has steadily declined, falling into the 63–65 percent range by 2023–2025. The primary driver of this shift has been the growth of bauxite shipments, particularly from Guinea, where large mining expansions and new export capacity have increased long-haul volumes.

By 2025, bauxite accounts for roughly 16 percent of Capesize tonne-mile demand, up from low single digits in 2015. This evolution has diversified Capesize employment, reducing concentration risk and increasing the influence of West African trade routes.

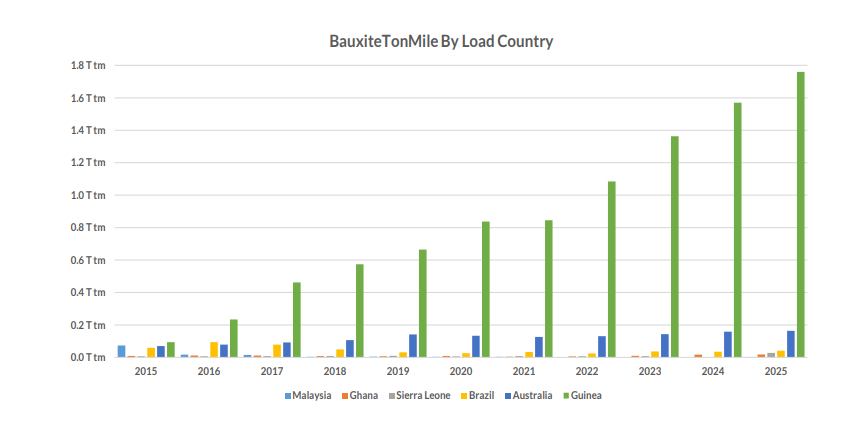

Guinea has established itself as a central player in global bauxite trade, producing over 8.4 trillion ton-miles in 2025, which is more than six times the ton-mile output of Australia, the second largest exporter. This development highlights both the significant growth in Guinea’s export capabilities and China’s increasing dependence on long-haul West African bauxite for its alumina and aluminum industries.

Key Development: First Iron-Ore Shipment from Simandou

A significant milestone was reached in December 2025 with the first commercial shipment from Guinea’s Simandou mine. On 2 December, the bulk carrier Winning Youth departed Morebaya Port carrying 200,000 tonnes of high-grade ore for China, marking the launch of Simandou’s integrated mine-rail-port-shipping system More than just a milestone, this shipment signals the start of deliveries from an enormous deposit estimated at over 4 billion tonnes of ore, boasting an average iron content above 65%.

Signals That Will Shape the Capesize Market Ahead

The Capesize freight market is expected to continue holding a firmness, supported by strong Chinese import demand and sustained reliance on high-grade overseas ore. Tracking monthly domestic production will be essential for assessing any shift in China’s import requirements, while import volumes and port inventories will continue to serve as immediate signals for chartering activity and vessel deployment. Strategic stockpiling adds irregularity to procurement cycles, amplifying freight volatility. Quality differentials will keep shaping trade routes, with Australia, Brazil, and eventually Guinea (Simandou) retaining competitive advantages and supporting long-haul Capesize demand.

Data Source: Allied