The past week saw the Baltic Dry Index rise by eleven per cent, with much of the upward momentum provided by the panamaxes and capesizes. Among the commodities, iron ore and base metals belonged to the winners. On the other hand, crude oil, grains, and soybeans were among those facing headwinds.

By Ulf Bergman

Macro/Geopolitics

Over the past week, robust US economic data and hawkish statements from some Federal Reserve officials effectively ended any hopes of an imminent monetary easing. As a result, market expectations have shifted, and the first interest rate cut is now widely expected in September. Against this background, the US dollar index ended the week near the highest level since early November last year. With US interest rates expected to be higher for longer, a stronger US dollar will likely add some headwinds for the commodities markets.

The week ahead will provide some further indications of the state of the US economy. Data for durable goods orders will be released on Wednesday, followed by growth during the first quarter on Thursday. Additionally, consumer spending and price data will be available on Friday.

Commodity Markets

Crude oil was in the red for much of the past week. However, daily price movements were generally modest, with a substantial decline on Wednesday responsible for most of the past week’s performance. The June Brent futures recorded a weekly decrease of 3.5 per cent, ending Friday’s session at 87.29 dollars per barrel, as tensions in the Middle East eased somewhat. The contracts have continued to retreat in today’s trading amid losses of around one per cent.

The European natural gas futures market experienced a week of volatility as supply disruptions and easing geopolitical tensions competed for traders’ attention. The front-month TTF futures ended the week at 30.76 euros per MWh, marginally higher than the previous week’s close. The new week has seen further losses for the contracts, which are trading more than three per cent below Friday’s settlement.

The benchmark futures for the Asian and European coal markets experienced diverging fortunes throughout the past week. Lower European natural gas prices contributed to the futures for delivery in Rotterdam next month shedding 2.3 per over the course of the week, ending Friday’s session at 116.55 dollars per tonne. On the other hand, robust demand in Asia saw the Newcastle futures record a weekly gain of 6.0 per cent as they settled at 141.75 dollars per tonne on Friday.

Iron ore delivered a second consecutive week of solid gains as Chinese demand remained robust. Amid three sessions in the black, the May futures listed on the SGX recorded a weekly gain of 4.9 per cent, ending the week at 116.45 dollars per tonne. However, the new week has begun in the red amid limited losses of around a third of a per cent.

An improving demand outlook and concerns over global supplies contributed to rising base metal prices last week. The three-month nickel and aluminium futures listed on the LME led the way higher with weekly gains of 8.6 and 7.0 per cent, respectively. The copper contracts advanced by 4.4 per cent over the past five trading sessions, while zinc edged up by 0.8 per cent over the period.

Despite gains on Friday, the grain and oilseed futures listed on the CBOT declined last week as abundant supplies and some concerns over demand weighed on prices. The May soybean futures recorded a weekly loss of 2.0 per cent, while the wheat and corn contracts shed 1.0 and 0.5 per cent, respectively.

Freight and Bunker Markets

The Baltic Exchange’s dry bulk indices had a second straight week of gains, with all segments recording gains. As a result, the headline Baltic Dry Index rose by 11.0 per cent over the past week.

Despite some marginal weakness on Friday, the sub-index for the capesizes recorded a weekly gain of 11.2 per cent, with weaker tonnage supply in the Atlantic and Pacific basins contributing to the bullish sentiments. Still, the gauge for the panamaxes delivered the past week’s most robust performance with a gain of 11.9 per cent. The segment benefitted from relatively strong cargo order volumes in the Atlantic and the Pacific. The indicator for the supramaxes advanced by 9.6 per cent over the past week as demand remained stable amid lower vessel availability. The handysizes were the past week’s laggards, with their sub-index recording a modest weekly gain of 2.6 per cent.

The Baltic Exchange’s wet freight gauges endured more mixed conditions and volatility during the past week. The dirty tanker index declined throughout the past week, adding up to a 7.3 per cent weekly loss. On the other hand, the indicator for the clean tankers rose by 16.3 per cent amid robust demand during the first half of the week. The gauges for the LPG and LNG carriers ended the week in the black, albeit to very different extents. The freight gauge for the LNG tankers recorded a weekly gain of 4.0 per cent, while the LPG index jumped by 41.1 per cent amid a surge on Friday.

Falling crude oil prices contributed to losses for the trading in marine fuels last week. While the VLSFO recorded only a marginal retreat in Singapore, the past week saw the fuel decline by around three per cent in Houston and Rotterdam. For the MGO, the past week’s losses were more substantial. Rotterdam led the way lower with a weekly loss of 7.6 per cent, while Singapore and Houston saw the fuel decline by 6.2 and 5.0 per cent, respectively.

The View from the Shipfix Desk

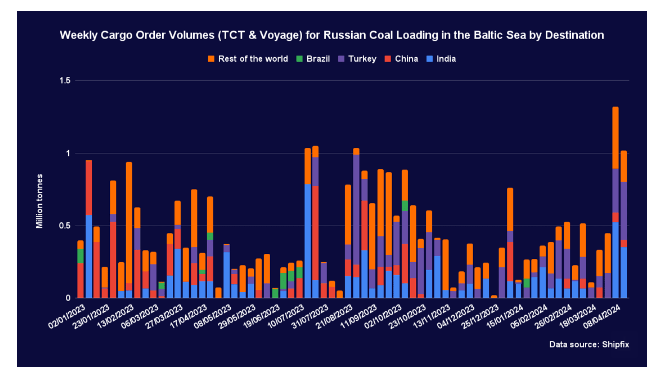

Russian coal exports from its terminals in the Baltic Sea have experienced both headwinds and volatility since sanctions put an end to access to European Markets. As highlighted in Friday’s edition of The Fix, a likely increase in Indian demand could see a rise in volumes shipped from the ports in the Baltic Sea.

The past two weeks have seen a significant increase in cargo ordering activities for Russian coal loading in the Baltic Sea region. While, as previously mentioned, part of the surge has been for shipments to India, there has also been an increase in demand for cargoes bound for Türkiye. After a weekly average during the first three months of the year of around 360,000 tonnes, the past two weeks have seen the total topping one million tonnes.

The recent surge in weekly cargo has chiefly benefitted the panamaxes, with the demand situation in the other segments broadly unchanged. Given the often lengthy voyages in the coal trade from the Baltic Sea, the recent developments have added to the tonne-mile demand in the panamax segment.

Data Source: Shipfix