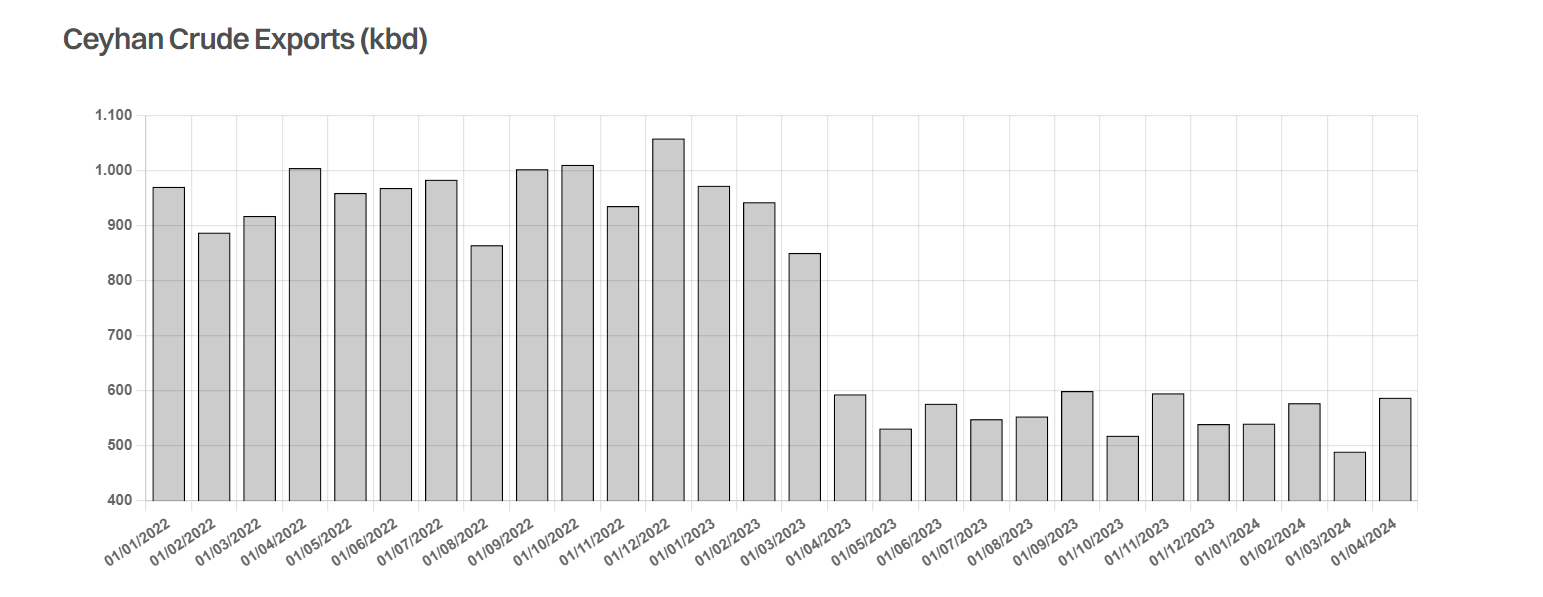

After just over a year of being offline, discussions about restarting the 450 kbd KRG pipeline remains at an impasse. Despite months of negotiations since March 2023, insufficient progress has been made to restart flows from Northern Iraq to the Turkish port of Ceyhan. Political tension between the Federal Iraqi Government, the autonomous Kurdistan Regional Government (KRG) and Turkey have blocked previous attempts at finding a resolution. For the tanker market, particularly the Aframax sector, this resulted in the loss of approximately 400 kbd of exports out of Ceyhan, reducing the supply of crude cargoes in the Mediterranean, forcing owners to look for other opportunities.

Therefore, the news this week that the Iraqi government will go ahead with repairing and reopening the separate 350 kbd Kirkuk-Ceyhan pipeline comes as welcome news. The 960km pipeline had been out of action since 2014 after repeated attacks by ISIS. Nevertheless, government officials are indicating the pipeline will probably be ready to restart operations by the end of April, once work on the storage and pumping facilities are completed. However, this start date is quite ambitious and likely to be pushed back later into Q2.

In terms of what this means for restarting the KRG pipeline, this development is likely to add further difficulty to the current dispute. The KRG will not be satisfied with Iraq being able to export its crude into the Mediterranean while cutting the KRG off from the revenue this generates to finance its various commitments. This is likely to stall reopening the KRG pipeline beyond this year and entrench existing positions unless one side makes concessions which again appears unlikely at present.

For the Mediterranean refining sector, fresh light and medium sour Iraqi grades are likely to be well received given both the ongoing absence of Urals and eliminating the need to go via the Cape of Good Hope to avoid the Red Sea. This should provide some support to the Mediterranean middle distillates complex.

It is also worth noting that given current OPEC product quotas, if Iraq is to start exporting via its North bound pipelines into the Mediterranean, they may have to reduce exports from its Southern ports. In such scenario, this would be bearish for the AG tanker market, especially in the Suezmax sector.

Although, the resumption of Northern exports should be good news for the Mediterranean Aframax sector, the gains could be capped. While in in theory this should support cross-Mediterranean rates. The biggest unknown is likely to come from Aframaxes engaged in Russian trade. Urals continue to trade above the $60 G7 price cap and increasing sanctions enforcement is forcing some players to exit this trade and seek other opportunities. An additional, 350 kbd of non-sanctioned Iraqi crude is unlikely to be sufficient to offset rising vessel availability in the region if enough tonnage leaves the Russian market.

Data source: Gibson Shipbrokers