In early 2026, China’s official customs data points to a sequential slowdown in steel exports, with cumulative shipments across January and February totalling 15.59mln mt, down 8.1% y-o-y. However, shipping data from AXSMarine presents a somewhat more nuanced picture. While reported export volumes have declined, shipments via dry bulk vessels have increased over the same period, rising by 12.3% y-o-y to 13.8mln mt. While part of the discrepancy may reflect differences in shipment timing, the increase in dry bulk volumes nonetheless points to a degree of resilience in seaborne activity, suggesting that underlying export flows may be holding up better than implied by customs data.

This divergence indicates that the recent weakness in export data may not fully reflect actual demand conditions. In particular, it raises the possibility that earlier concerns over a sharp contraction in steel-related shipping demand may have been overstated.

A closer look at the January–February custom data reinforces this view. Export volumes stood at 7.75mln mt in January (-11.37% y-o-y) and 7.84mln mt in February (-2.47% y-o-y), pointing to a gradual adjustment rather than a sharp contraction. This suggests that market participants have largely adapted to the new regulatory framework. While smaller traders continue to face higher compliance costs, larger mills, supported by more established compliance systems, have been able to maintain relatively stable export flows, and may have even captured market share from smaller players given their relative cost advantage.

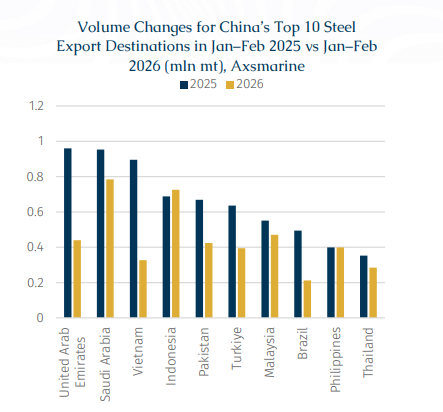

Shipping wise, the steel export segment within the dry bulk market reveals a notable trend: China’s steel export destinations have become increasingly diversified. According to data from AXSMarine, although China’s seaborne steel exports in the first two months of this year posted an annual increase, shipments to only two countries among the top ten export destinations from the same period last year rose..

While the combined import volume of these top ten destinations declined by 32.4% y-o-y in January–February 2025, this was offset by increased shipments to a broader range of smaller markets. As a result, the overall export performance remained relatively resilient, highlighting a shift toward a more diversified export structure amid the previously mentioned trade frictions. Despite weakening demand from traditional buyers, China has successfully identified new markets to absorb incremental export volumes. Among the key sources of growth, India stands out, with imports increasing by 228.8% y-o-y to 0.52mln mt, compared to just 0.16mln mt in the same period last year, when it ranked only 25th among China’s steel export destinations.

Nevertheless, China’s steel exports are unlikely to enjoy a smooth path going forward. More importantly, the Middle East conflict has disrupted shipping through the Strait of Hormuz, prompting some Chinese steel exporters to halt new offers to the region. Rising freight rates, vessel shortages, and insurance inflations have limited the availability of cargoes to Gulf countries, China’s second-largest steel market. Such constantly evolving policy and macro developments are also raising the bar for seaborne trade: shipowners and charterers must continuously adapt to shifting market conditions and actively explore viable trade routes.

While seaborne steel exports have shown some positive signs in the first two months of this year, it is important not to overlook the fact that, from a fundamental perspective, steel exports are still likely to remain under pressure. Whether current seaborne steel volumes can sustain their growth trajectory will remain a key point to monitor over the longer term.

From a policy perspective, the decline in exports is not unexpected. Export controls introduced in late 2025 triggered a wave of front-loading, with December exports rising by 16.2% y-o-y to 11.30 mln mt. Against this backdrop, the subsequent pullback in early 2026 reflects a normalisation following the pre-policy surge. That said, in magnitude, the decline has remained relatively moderate, suggesting that the actual impact of the new regulations has been less pronounced than initially expected.

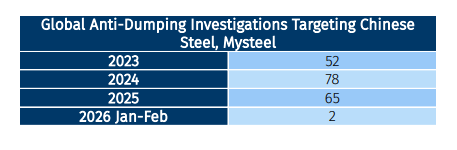

Beyond policy, other factors have also played a role. RMB appreciation has weighed on export competitiveness, while ongoing trade frictions, including anti-dumping measures from countries such as Mexico, Brazil, and Pakistan, have added pressure on shipments. Taken together, these dynamics suggest that the recent decline in exports reflects a combination of factors, rather than being solely driven by regulatory changes. Escalating US tariffs have also increased export uncertainty. Although some duties were struck down in February 2026, core tariffs under Sections 232 and 301 remain, and frequent policy shifts, blocked transshipment routes, and broader coverage on downstream products make cost calculation difficult for exporters, adding indirect pressure on Chinese steel shipments.

That being said, this seaborne export resilience should be interpreted with some caution. Structural headwinds remain in place, including policy-driven export constraints and broader industry restructuring. From a medium- to long-term perspective, a reduction in steel exports is likely to remain the prevailing trend, in line with policy objectives outlined during the recent “Two Sessions” meeting which emphasised capacity reduction, industrial upgrading, and a transition towards higher-value production.

In summary, while China’s steel exports have declined in early 2026, the impact on shipping demand appears more muted than initially feared. The recent strength in dry bulk shipments highlights a degree of resilience in seaborne demand, suggesting that earlier market expectations may have been overly pessimistic. Nevertheless, with export volumes still likely to trend lower over time, any near-term strength in shipping demand may prove temporary and worth continuing monitoring.