Effects on Dry Bulk Shipping and Agriculture

Executive Overview

Following our previous weekly analysis focused on the oil segment, this report examines the potential implications of current Middle East disruptions for the agriculture sector and the dry bulk shipping market.

Initial market attention centred on the potential interruption of oil and LNG flows through the Strait of Hormuz, one of the world’s most critical maritime chokepoints. However, the crucial importance of this corridor extends beyond energy markets and into the global fertiliser supply chain.

The Persian Gulf region has developed into a major fertiliser production hub due to the availability of competitively priced natural gas and long-standing investment in large ammonia and urea production facilities in countries including Qatar, Saudi Arabia, and the United Arab Emirates. Disruptions to maritime traffic through the Strait of Hormuz would therefore affect not only hydrocarbon exports but also the movement of nitrogen fertilisers and their feedstocks, linking energy market volatility directly with agricultural supply chains.

Countries with significant fertiliser import dependence, particularly in Asia and Latin America, may face rising procurement costs and supply uncertainty if logistical disruptions persist. Recent vessel-tracking observations indicate reduced bulk carrier activity linked to fertiliser and agricultural cargoes. At the same time, rising bunkering prices, higher war-risk insurance premiums, and widened energy market volatility are contributing to persistent uncertainty for the shipping industry.

Middle East Tensions and Dry Bulk Commodity Exposure

The geopolitical situation is influencing expectations across several dry bulk commodity markets as energy disruptions, maritime risk, and rising freight costs affect trade flows.

Coal shipments moving directly through the Strait of Hormuz represent a relatively small portion of global coal trade, estimated at roughly five million tonnes annually. However, the sector may experience indirect effects as energy markets adjust to LNG supply uncertainty. LNG benchmark prices have risen in recent weeks amid concerns about potential disruptions to Gulf export infrastructure and shipping routes. If LNG availability tightens or prices remain elevated, some energy importers may increase reliance on alternative fuels, including coal.

In the iron ore market, the overall global trade structure remains largely unchanged. However, Iranian exports have declined during the first quarter of 2026 amid rising logistical constraints, insurance costs, and freight risk premiums. While Iran represents a relatively small share of global iron ore supply compared with major exporters such as Australia and Brazil, continued disruptions could further reduce its export volumes.

Agricultural bulk commodities are more directly exposed to shipping disruptions in the region. Heightened tensions around the Strait of Hormuz increase risks for established grain and agricultural commodity routes serving Middle Eastern markets. Major suppliers to the region, including Brazil and Russia, may face higher freight costs or logistical adjustments should maritime traffic remain constrained.

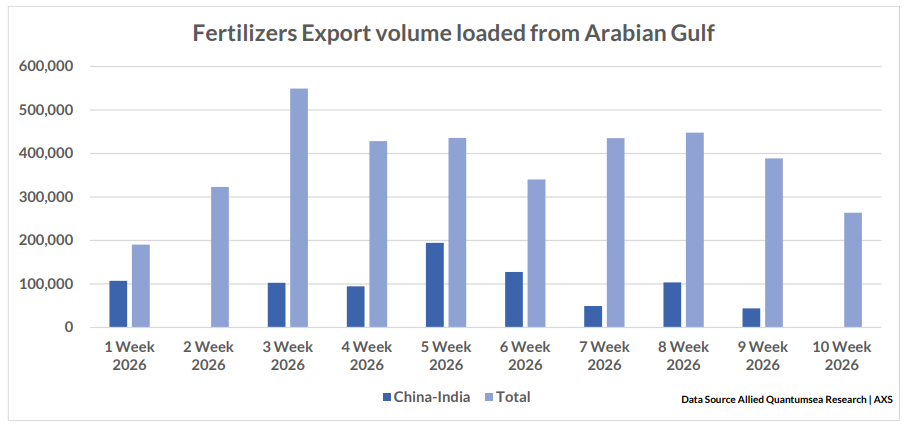

Brazil’s exposure extends beyond fertiliser imports to its large export volumes of corn and soybeans, while Russia’s exposure is primarily associated with wheat exports to the region. Other minor bulk commodities may also experience disruption. The Middle East is an important destination for construction materials, steel products, and other building inputs, and sustained shipping disruption could affect supply chains for major importing economies such as India. However, among dry bulk commodities, fertilisers remain the most structurally exposed. Industry estimates indicate that approximately 16% of global seaborne fertiliser trade originates from the Arabian Gulf, including sulphur, urea, and phosphate products

Fertiliser Supply Vulnerability

A significant share of global urea trade passes through the Strait of Hormuz. The region’s prominence in nitrogen fertiliser exports reflects access to low-cost natural gas and decades of investment in large-scale export-oriented fertiliser complexes. Sulphur supply is also connected to energy markets. Because sulphur is largely produced as a by-product of oil and gas refining, reduced hydrocarbon processing or export activity could tighten sulphur availability and influence fertiliser production elsewhere.

Unlike energy markets, where strategic reserves may partially mitigate supply shocks, fertiliser production capacity cannot be expanded quickly. Building new ammonia or urea plants requires significant capital investment and multi-year construction timelines, which means sustained supply disruptions could affect pricing and trade flows over an extended period.

Fertiliser Prices and the Role of Asian Importers

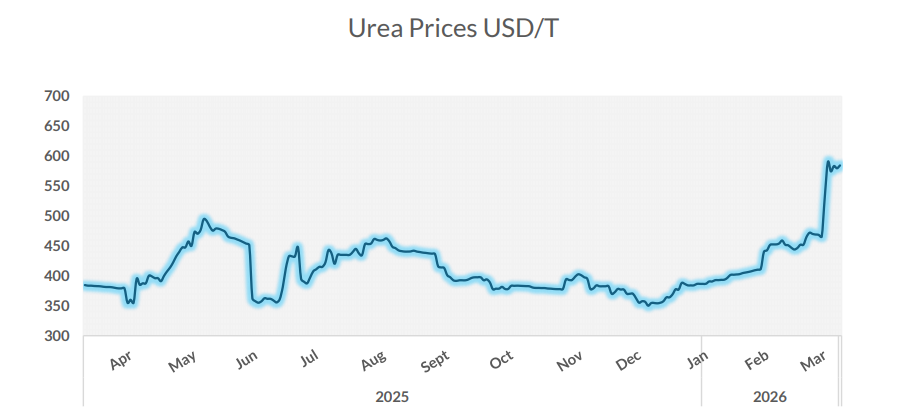

Market participants have already observed upward pressure in fertiliser markets as traders incorporate potential logistical risks, higher freight costs, and rising insurance premiums. Asian markets represent one of the largest demand centres for imported fertilisers. Countries including India, Pakistan, Bangladesh, and several Southeast Asian economies rely heavily on imported urea to support agricultural production.

India supplements domestic fertiliser production with imports while also relying on natural gas imports for part of its domestic manufacturing base. Disruptions affecting Gulf supply routes could therefore increase competition for alternative cargoes from other producing regions, contributing to upward pressure on global fertiliser prices. Government procurement programmes and fertiliser subsidy systems across Asia may also influence market dynamics if authorities move to secure additional supply ahead of key planting seasons.

implications for Brazil and Global Agriculture

For Brazil, one of the world’s largest exporters of soybeans and a major maize producer, fertiliser availability is a critical determinant of agricultural productivity. Brazil imports a substantial share of its fertiliser requirements, including nitrogen, phosphate, and potash products. If fertiliser prices rise or logistics become constrained, Brazilian farmers may face higher input costs that could affect planting decisions, crop margins, and export competitiveness in global agricultural markets. Because fertiliser availability influences agricultural production with a time lag, the full impact of supply disruptions may only become visible during future planting and harvest cycles.

Alternatives to Agricultural Urea | Short-term substitutes for urea remain limited.

Farmers can partially shift toward other nitrogen fertilisers such as ammonium nitrate, ammonium sulphate or urea ammonium nitrate (UAN) solutions. However, these products rely on similar upstream inputs, particularly ammonia and natural gas, meaning supply constraints may affect the broader nitrogen fertiliser complex.

Organic fertilisers and manure-based nutrients can supplement soil fertility, but cannot replace the scale of nitrogen required for modern commercial agriculture. As a result, global crop production remains strongly dependent on industrial fertiliser supply chains.

Dry Bulk Shipping Activity and Fleet Distribution in the Gulf

Vessel-tracking data indicate a significant slowdown in dry bulk movements through the Strait of Hormuz during the recent escalation in regional tensions.

Reporting by Lloyd’s List, citing Lloyd’s List Intelligence vessel-tracking data, indicates that only a limited number of dry bulk vessels have attempted to transit the strait in recent days. Among the bulk carriers reported to have crossed were the Supramax vessels KSL Hengyang (IMO 9333931) and Sino Ocean (IMO 9222338), both approximately 53,000 deadweight tonnes, which transited the Strait of Hormuz over the weekend.

According to the same reporting, several vessels that continued to transit the corridor were linked to Chinese ownership or operations and transmitted AIS messages identifying their national affiliation during passage. The Liberia-flagged bulker Sino Ocean broadcast the AIS message “CHINA OWNER_ALL CREW” while crossing the strait.

The limited number of crossings reflects the broader slowdown in maritime traffic through the chokepoint as shipping companies reassess war-risk exposure, insurance availability, and operational safety. Iranian authorities have warned that vessels linked to the United States, Israel, or their allies could face attack or be prevented from transiting the Strait of Hormuz. Vessel-tracking analysis by Lloyd’s List Intelligence shows that a small number of ships, including several linked to Chinese ownership or operations, have attempted to transit the corridor, with some vessels broadcasting national affiliation via AIS during passage.

During the recent disruption, several vessels attempting to transit the strait have transmitted AIS messages highlighting national ownership or crew composition. Ships associated with Chinese ownership or operations have been among those continuing to transit the corridor. If tensions persist, vessels owned, chartered, or operated by Chinese maritime companies or other non-Western operators may account for a larger share of transits as shipowners adjust routing and operational strategies to manage geopolitical risk exposure.

Fleet monitoring indicates that a large number of dry cargo vessels remain inside the Persian (Arabian) Gulf while operators assess security conditions. According to AIS-derived fleet intelligence compiled by AXSMarine, more than 350 dry cargo vessels are currently positioned within the Gulf, including:

• 236 bulk carriers

• 117 multipurpose vessels associated with dry bulk trades

A majority of vessels currently within the region are laden, indicating significant cargo volumes awaiting potential transit.

The fleet breakdown includes:

• 144 laden bulk carriers

• 92 bulk carriers in ballast

• 71 laden multipurpose vessels / 46 multipurpose vessels in ballast

Among bulk carriers currently located in the Gulf, the largest share consists of:

• Panamax vessels between 68,000 and 85,000 dwt

• Supramax vessels between 50,000 and 60,000 dwt

• Handysize vessels between 25,000 and 40,000 dwt

Only four Capesize bulk carriers, each between 170,000 and 180,000 dwt, are currently reported in the region.

Takeaways

The Strait of Hormuz remains a critical junction not only for global energy supply but also for fertiliser and dry bulk commodity trade. A meaningful share of global urea and sulphur exports originates from producers in the Arabian Gulf, making the region strategically important for agricultural supply chains. Fertiliser prices have shown signs of upward pressure as markets assess logistical risks. Asian importers represent a key demand centre, while Brazil’s agricultural sector may face higher input costs due to its reliance on imported fertilisers. Shipping data indicates limited recent bulk carrier activity linked to agricultural cargoes, reflecting heightened operational caution among vessel operators. If disruptions persist, the implications may extend beyond energy markets to influence fertiliser pricing, agricultural production costs, and dry bulk shipping demand worldwide.

Data Source: Allied