Our House View: Oil prices are rising at the quickest pace since the 1980s. Still, we see the Iran War as a major disruption, but well in line with our 3D themes (Debt, Disruption, Deregulation), and a world that is experiencing significant geopolitical and geoeconomic reorientation.

Inflation from oil itself may not necessarily be a long-term problem if the present sharp disturbance (closed Straits of Hormuz, attacks on refineries in the wider area) doesn’t last for very long. It will likely affect prices at the pump and some products, but it could very well be a short-lived affair. The equity market correction is, up to this point, within norms and there’s little reason, at this point in time, why medium-term impact should be significant.

But we do see this episode, as well as emerging issues from the private credit market, as adding to the general risks, which are underpinned by very large debt and exacerbated by worsening trade uncertainties.

----------------------

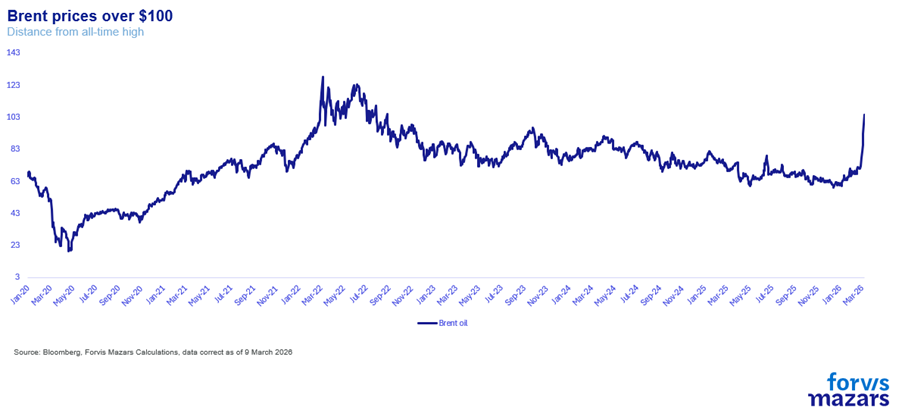

This morning Brent crude peaked at highs of $117, with intense volatility—almost double (+98%) its levels at the December lows, before retracing just north of $100. It is the steepest rise in oil prices in modern history since 1985. The move comes after the election of a new Supreme Leader in Iran and a wider spillover of the conflict, with Iranian strikes against targets including Bahrain, Quartar, Saudi Arabia, and Iraq, as well as the targeting of Iranian refineries by western forces.

Is this a crisis?

Not yet.

The sharp increase in oil prices is, to some extent, expected as long as the Strait of Hormuz remains closed and Iran, as well as the U.S. and Israel, intensify their attacks and the war spilling over to other countries.

The key issue remains not “how much” oil rises, but “for how long.” Markets still look towards the cost of money as a key driver of asset prices. Central banks can set the tone for equities and bonds, they can provide comfort (“the Fed Put”, via lower interest rates or market operations) when prices oscillate too much, or they can cause worries if they hike to fast, or even stay silent during a crisis. The sharper and more prolonged the increase, the more likely it is to fuel inflation and the harder it becomes for central banks to intervene in a reassuring way.

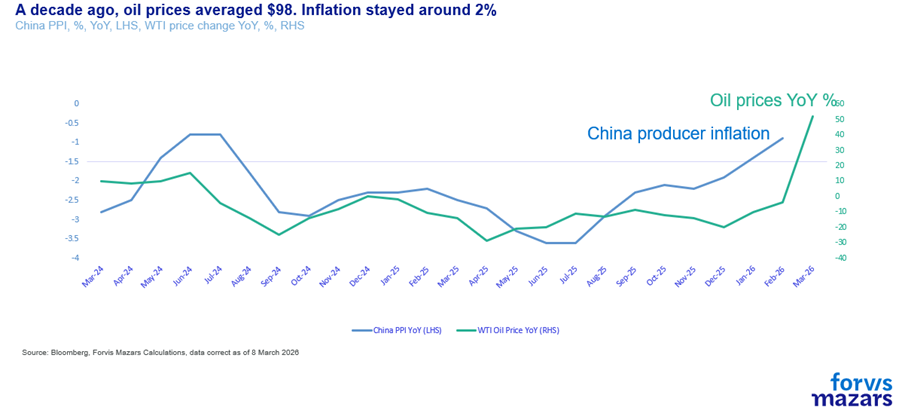

At the moment, the U.S. Federal Reserve finds itself in a difficult position. Friday’s weak payroll numbers (minus 92,000, the second-worst reading since the pandemic) would normally have triggered expectations of rate cuts. However, fears that a prolonged war could push energy prices even higher and complicate the central bank’s traditional reassuring intervention, whether in practice or in rhetoric, creating concern in financial markets. Additionally, and while largely unnoticed, Chinese producer prices are coming out of disinflation territory, adding to inflationary pressures.

Nevertheless, we don’t see evidence of a wider crisis.

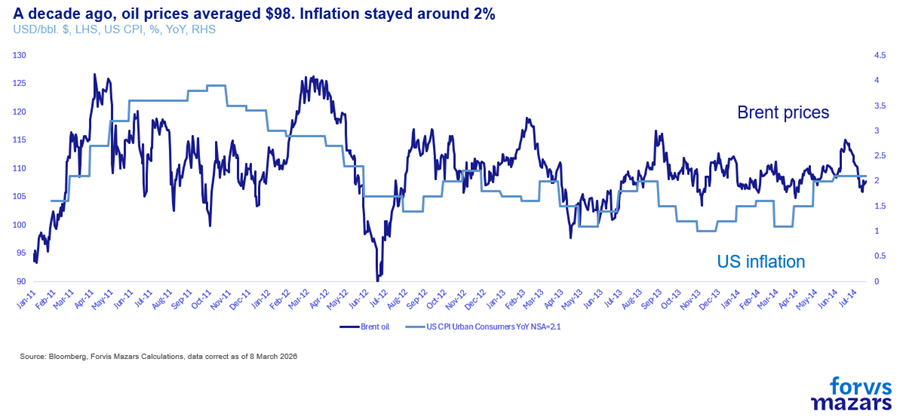

Oil alone does not necessarily create inflation

Between 2011 and mid-2014, Brent prices averaged around $98 per barrel. During that period, average U.S. inflation was 2.1%, while European inflation averaged 1.9%.

With the labour market weakening, artificial intelligence creating structural changes in the economy, and the United States reducing its demand from the rest of the world, strong disinflationary pressures remain in place.

Of course, a new inflationary wave, particularly in the United States, cannot be ruled out, with energy acting as a catalyst, though not the sole underlying cause. The real issue has been, and remains, the U.S. trade war. Lower energy prices had played a major role in limiting the impact of tariffs. An oil shock could therefore act as the trigger for the inflation bump that markets and economists had long anticipated.

In Europe, however, and the UK, weaker demand continues to generate even stronger disinflationary pressures, so the probability of a sustained inflation wave is smaller.

The equity market correction was long overdue

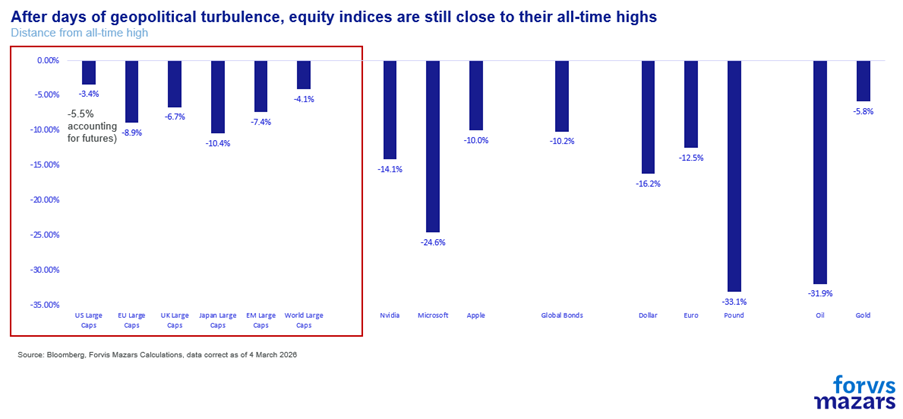

Equity markets had become relatively expensive and were searching for a catalyst for a correction. That catalyst has now arrived in the form of war—and so far the correction remains fairly mild.

U.S. equities were about 6% below their highs on Monday morning, while European and Japanese markets have entered "official correction" territory, slightly above 10%.

All of this remains within the range of normal market volatility. It is also worth remembering that European and Asian equities had rallied significantly since the beginning of the year, largely due to U.S. dollar weakness. Now that this trade has reversed amid the crisis, these markets are correcting more sharply.

There is significant “noise” in energy prices, and markets in general

The sudden move in oil prices is certainly concerning. However, we should not forget that markets today are dominated by fast trading. The recent meteoric rise and subsequent decline in the price of gold, a supposedly safe and stable asset, should remind us that volatility is here to stay.

The Strait is unlikely to remain closed for very long

The main issue lies in the Strait of Hormuz and Iran’s attacks on its neighbours. Threats from the Revolutionary Guards to target passing vessels have created a bottleneck in the global energy supply.

However, “incentives drive behaviour”, our CIO Ben Seager Scott would say. We need to remember that the importance of the Strait is arguably big enough to prompt all actors in the Gulf and those involved in the war to take action and protect it, sooner rather than later.

Meanwhile, some shipping companies—Prokopiou’s group, for example—are already willing to take the risk and transit the passage. Others may follow. Shipping is a highly dynamic industry that has learned to significantly increase profitability during such periods.

Insurance companies are returning to the market with higher premiums (1% to 5% of the vessel’s total value) but with at least some level of protection for shipowners.

Still, there is no room for complacency.

Iran alone may probably not trigger an economic or financial crisis, but it can amplify problems that already exist.

Tariff uncertainty, for example, which would have likely been a bigger headline were it not for Iran, is now threatening to weaken the developed and global economy further. The trade war has made inflation more unpredictable and dangerous, and the conflict with Iran is complicating matters further. At the same time, White House attacks on the Federal Reserve are at the very least threatening to weaken the most important of the institutions that may provide defence against market and economic crises.

Alongside the Iran situation, another potential problem is unfolding in the U.S. private credit market, which could have broader consequences. Starting with the collapse of Market Financial Solutions, redemption restrictions were imposed on major private credit funds managed by Blackstone and BlackRock—an indication of a classic liquidity crisis in an illiquid market that had expanded its reach to retail (and many institutional) investors.

It is important not to become too consumed with the geopolitical crisis and to pay close attention to pre-existing structural problems that we already know about—problems that oil above $100 may bring to the surface more quickly.

What Businesses should remember.

Businesses should continue to build resilience. We have spent the last two years repeating that “Resilience” is the key to a disrupted world. We have further expanded the idea into our 3D themes (Debt, Disruption, Deregulation), to explain why and how the world is likely to remain disrupted for the foreseeable future. The Iran War is but another branch in the global geopolitical and geoeconomic rebalancing, with, possibly more disruption to follow.

What Investors should take away?

Equity markets were long overdue for a correction, and the war provided a catalyst. But it would be a terrible oversimplification to suggest that mean reversion and fresh highs are the only way forward. Volatility is set to continue. This creates angst, but also opportunities for capable active managers and asset allocators. As far as we can see, the market continues to function well. As long as the event is not systemic, or does not trigger other systemic events, then the long-term benefits of portfolio management are still very much working in favour of those who remain invested.