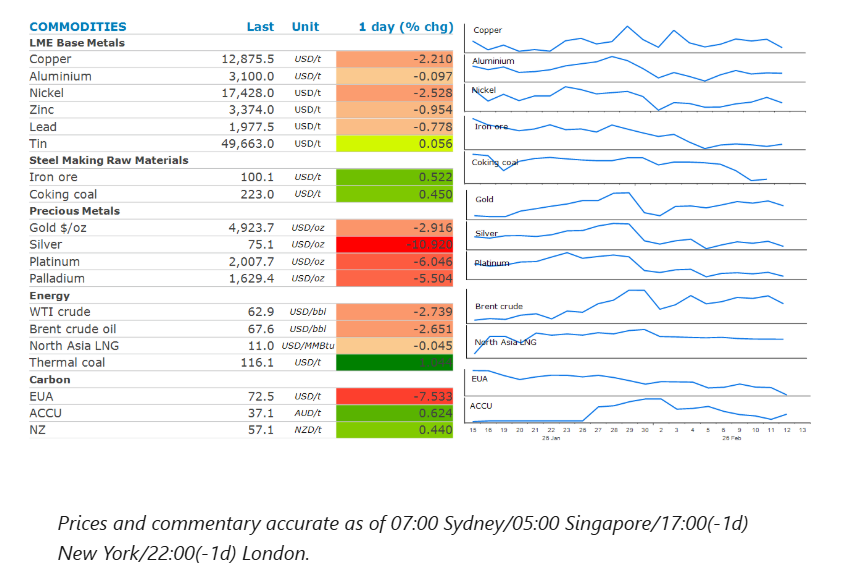

A risk-off tone across markets weighed on commodity markets. Precious and industrial metals led the sell-off. Oil was also lower on lower geopolitical tensions.

By Daniel Hynes

Market Commentary

Crude oil fell amid a risk off tone across markets. Easing geopolitical tensions also weighed on the market. US President Donald Trump said that his preference is to reach a nuclear deal with Iran. He told Israeli Prime Minister Benjamin Netanyahu that he intends to press ahead with talks, despite Israel’s preference for a broad curtailment of Iran’s military activities in the region. These eased concerns of US military intervention in the region, and any subsequent disruption to oil supplies. Sentiment wasn’t helped by a bearish outlook from the International Energy Agency. It trimmed its 2026 oil demand growth amid higher prices. Global oil consumption is now seen rising by 850kb/d this year, down from 930kb/d in its January report. It also noted that oil stockpiles have swelled the most since 2020. Inventories increased by an extraordinary 477mbbls in 2025, with stocks in OECD countries surpassing their five-year average for the first time in four years. Oil trading firms suggest the rising level of sanctioned oil stranded at sea is driving up oil prices. According to ship-tracking firm Vortexa, there is around 290mbbls of Russian and Iranian crude currently on the water. This is more than 50% higher than a year ago. A ramp up of sanctions has restricted flows from these nations over the past few months, forcing buyers such as India to seek alternatives.

European natural gas extended gains on rising energy security concerns. Traders attending an industry conference in Germany sounded the alarm over the continent’s depleted natural gas inventories. With six weeks to go until the end of the heating season, Europe’s storage tanks are set to emerge from this winter even more depleted than in 2025. To compound matters, there is little incentive for buyers to purchase fuel to inject into storage sites, with summer prices still slightly higher than those for next winter. There is a threat that some storage facilities shut due to challenging financial conditions if state support is not forthcoming. North Asia LNG prices edged higher as spot buying picked up. Buyers from Thailand and South Korea were particularly active. Still, warmer conditions forecast across China and Japan in coming weeks could cap spot prices as higher temperatures may reduce demand for the fuel.

Aluminium led the base metals higher early in the session as a looming smelter closure added to supply strains. South32 confirmed that it’s still planning to mothball its Mozal smelter in Mozambique, despite receiving some “inbound interest” in the asset. The smelter is a key supplier of aluminium into the European market. This comes as China’s industry nears its government-imposed cap on capacity, leaving buyers scrambling for alternative sources. Nickel struggled to hold onto yesterday’s gains after reports emerged that output must be slashed at the world’s largest nickel mine in Indonesia. Production at Weda Bay will be capped at 12mt of nickel ore, down from 42mt in 2025. However, concerns were eased with the market likely to remain in surplus despite the lower Indonesian output.

Gold ended the session lower following a sharp selloff across financial markets near the close. US technology stocks fell amid renewed concerns over whether massive investment in AI will materialise in a big way. The risk off tone also triggered some profit taking in the precious metal sector. The moves come ahead of key US economic data, which should shed some light on the Fed’s next move. An unexpected rise in inflation could reduce the Fed’s desire to cut interest rates further, making gold less attractive for investors.

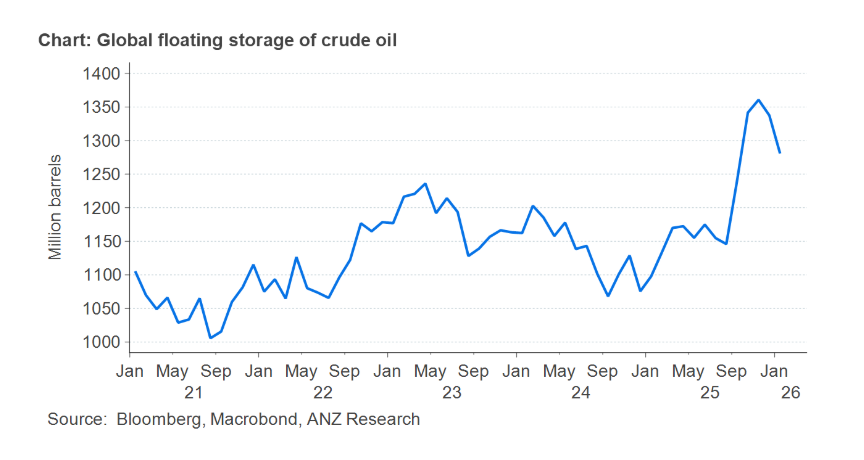

Chart of the Day

Global storage of crude oil on tankers at sea is sitting at record highs. However, the easing of some sanctions on Venezuela has seen this level drop in recent weeks.

Data source: Commodities Wrap