This time last year, the dry bulk market was grappling with pronounced weakness and a lack of conviction across nearly all segments. The Handysize sector, often considered the market’s defensive cornerstone, stood out merely by losing less than the rest. Even so, rates were sliding sharply, while Panamax, Supramax, and particularly Capesize earnings were under acute pressure. Freight sentiment at the time was dominated by oversupply, hesitant commodity demand, and a visible erosion of confidence, pushing the BDI into levels not seen since early 2023. Fast forward twelve months, and the contrast could hardly be more striking. The opening quarter of the year has unfolded with unexpected vigor, delivering one of the strongest starts of the recent past. Rather than grappling with double-digit weekly declines, the market has displayed broadbased resilience and consistent upward momentum. Notably, it is the gearless segments that have taken the lead. Capesize earnings advanced sharply over the week, recording gains of 16 percent and settling at $23,431 per day. Panamax rates followed closely, climbing 10.5 percent week-on-week to reach $14,504 per day. The Supramax segment also participated in the upswing, with average earnings closing just shy of the $13,000 per day mark, while Handysize rates strengthened further to finish the week at $10,793 per day. Although all indices remain below the elevated levels observed during the recent peak, they are decisively higher than the corresponding levels recorded a year ago, underlining the scale of the turnaround.

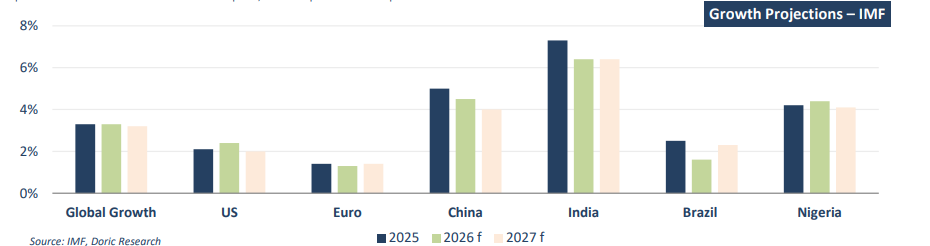

This improvement in freight markets is unfolding against a macroeconomic backdrop that, while far from exuberant, has proven more supportive than many had anticipated. According to the IMF, global economic growth in the 3 rd quarter of 2025 moderated to 2.4 percent on an annualized basis. While this figure reflects a gradual deceleration, it still exceeded earlier expectations. Looking ahead, growth is projected to stabilize rather than deteriorate, with ongoing momentum in high-technology and investment-driven sectors continuing to partially counterbalance weakness in more traditional industries. Trade policy uncertainty and tariffs remain a structural drag on global activity, but their impact on growth is expected to diminish as economies adjust. IMF projections place global growth at 3.3 percent in 2026, easing slightly to 3.2 percent in 2027. Notably, the 2026 forecast has been revised upward by 0.2 percentage point compared with the previous outlook, suggesting a more constructive near-term trajectory, even as medium-term risks persist.

Within advanced economies, growth is expected to remain rather stable. The U.S. is projected to expand by 2.4 percent in 2026, supported by fiscal stimulus and a lower policy rate environment, with the dampening effects of higher trade barriers gradually fading. Growth is forecast to remain close to 2.0 percent in 2027, aided by targeted tax incentives designed to stimulate corporate investment. In the euro area, growth is expected to hold at modest levels, averaging around 1.3 to 1.4 percent through 2026 and 2027. Increased public spending, particularly in Germany, alongside robust performances in Ireland and Spain, is expected to provide incremental support. Japan’s growth profile remains more constrained, with expansion projected to slow from 1.1 percent in 2025 to below 1.0 percent over the following two years. Even so, recent fiscal measures announced by the government have prompted an upward revision to earlier forecasts.

Emerging market and developing economies continue to provide the main engine of global growth, with aggregate expansion expected to remain just above 4.0 percent through 2026 and 2027. China’s outlook has improved modestly following additional stimulus measures and increased policy bank lending. Growth for 2025 has been revised upward to 5.0 percent, while the 2026 forecast has also been raised to 4.5 percent, reflecting lower effective US tariff rates and a multi-year policy support assumption. Beyond that, growth is expected to slow toward 4.0 percent in 2027. Among emerging markets, India continues to stand out as the new locomotive of global growth. IMF estimates place India’s growth at 7.3 percent in 2025, a sharp upward revision reflecting stronger-than-expected momentum. Growth is projected to moderate to around 6.4 percent in 2026 and 2027 as cyclical tailwinds fade, but this pace remains well above the global average and structurally supportive for seaborne trade. As India gradually assumes a more central role in global commodity trade flows, its influence on dry bulk demand dynamics is becoming increasingly structural rather than cyclical.

Global headline inflation is projected to decline further to 3.8 percent in 2026 and 3.4 percent in 2027, supported by softer demand conditions and lower energy prices. While inflation persistence remains more pronounced in the U.S. and select commodity exporters, most major economies are expected to converge toward central bank targets. This environment should allow for a gradual easing of financial conditions, reducing pressure on trade finance and capital-intensive sectors. From a trade perspective, merchandise volumes are expected to grow at a slower pace following the frontloaded expansion seen in 2025. World trade growth is projected to moderate from 4.1 percent in 2025 to 2.6 percent in 2026, before rebounding to 3.1 percent in 2027. These shifts reflect ongoing adjustments to new trade policies, inventory normalization, and evolving supply chains, rather than a collapse in underlying demand.

Compared with the stress conditions observed a year ago, today’s dry bulk market is operating from a markedly stronger footing. Early-year momentum, improving sentiment, and a more supportive macro backdrop have collectively lifted earnings across all major segments. However, with global trade growth expected to slow and policyrelated uncertainties still unresolved, the current upswing should be viewed through a cyclical lens rather than as the start of a linear recovery. The outlook remains constructive, particularly as emerging markets continue to absorb increasing volumes of seaborne commodities, but the sustainability of current rate levels will ultimately depend on how effectively demand growth keeps pace with fleet availability as the year progresses.

Data source: Doric