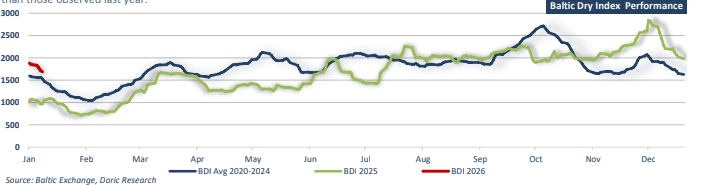

As the dry bulk sector progresses into the first weeks of 2026, the market is entering what is traditionally the softest period of the year, with seasonal patterns exerting their usual downward pressure on freight rates across all segments. Yet unlike previous cycles, Q1 has begun from a noticeably firmer base, reflecting the structural tightness carried over from 2025 and the continued firmness in major commodity flows. The usual early-year slowdown is therefore unfolding within a more balanced framework, with the market demonstrating resilience even as seasonal demand ebbs. Last year’s Q1 decline was more pronounced, shaped by soft Chinese demand, patchy weather in Brazil, and increased uncertainty. In contrast, 2026 has opened with steadier fundamentals and a clearer macro backdrop, reinforcing the industry’s expectation of “higher lows” and laying the groundwork for a smoother seasonal progression into Q2.

Iron ore remains the cornerstone of the dry bulk complex, and the comparison between 2025 and early 2026 illustrates both continuity and change. China ended 2025 with record imports surpassing 1.24 billion tonnes, driven by stockpiling behaviour, favourable pricing, and intermittent stimulus measures aimed at stabilising construction and manufacturing activity. Entering 2026, portside inventories have risen for a seventh consecutive week, reaching 162.7 million tonnes – just shy of the all-time high. This accumulation reflects both steady seaborne arrivals and more measured steel output, producing a market that feels heavy but still fundamentally supported. Capesize sentiment naturally softens in Q1. However, 2026 is opening from a stronger foundation than last year: despite recent corrections, the C5 and C3 spot routes continue to trade above their early-2025 troughs. Vessel supply in both basins is more evenly distributed compared with the dislocations of 2025, reducing volatility but also signalling that any early-Q2 pickup in Brazil may generate a more orderly tightening. Overall, the Capesize market is mirroring seasonal softness, yet retains a firmer undertone.

The Panamax segment is moving through its customary seasonal soft patch, yet it continues to perform from a noticeably firmer base than in early 2025. Coal demand across India and Southeast Asia has softened in line with seasonal norms, but procurement patterns remain more orderly than last year, when high inventories and inconsistent industrial consumption pushed the market into deeper early-year troughs. In grains, the pre-harvest lull is evident, but sentiment has improved thanks to a resurgence of interest in Nopac and Indo stems, which are offering welcome support in the Pacific. These early fixtures – though not yet large in volume – have helped stabilise regional lists and provide a sense that demand is more resilient than the calendar would suggest. Meanwhile, flows out of ECSA remain steady but limited, reflecting the natural pause before Brazil’s soybean export season accelerates, yet even these modest volumes are contributing to a more balanced Atlantic market compared with the disruptions seen in early 2025. With vessel positioning more evenly spread, the Panamax market is softer on a weekly basis but structurally stronger, reinforcing the broader expectation that this year’s seasonal lows will settle at higher levels than those observed last year.

Ultramax dynamics entering 2026 highlight a sector that continues to display underlying resilience. Throughout 2025, the segment benefitted from persistent imbalances in the Indian Ocean, strong coal movements into South Asia, and dense minor grain traffic across SEAsia and the Pacific. As the new year begins, the familiar seasonal pullback is unfolding, with softer tonnage demand ahead of the main harvest cycle and with regional coal flows pausing before they typically rebound toward the end of the Q1. Even so, the market stands on a firmer foundation than it did at the same point in 2025. Indian coal demand, though seasonally lower, remains supported by the country’s expanding power generation needs and a steady rise in industrial activity. Additionally, Ultramax remained buoyant on the back of improved demand from Indo and Nopac, while Australia continues to lag. The Atlantic is also enjoying a more constructive tone, with ECSA offering a steadier stream of cargoes than seen in previous Januarys, contributing to more balanced vessel positioning on both sides of the basin. As a result, although weekly fluctuations remain part of the seasonal pattern, the Ultramax market enters its annual trough in a noticeably firmer posture, with a clearer and more credible path toward a stronger rebound as agricultural flows gain momentum heading into the second quarter.

The Handysize market continues to reflect both seasonal behaviour and evolving macroeconomic conditions. Q1 typically brings subdued activity in the minor bulks and this pattern is visible again in 2026. European industrial activity remains soft, weighing on steel-related and project cargo demand, and dampening the momentum that supported Handysize vessels during parts of 2025. However, Asian coastal activity remains solid, with aggregates, bauxite, fertilizers, and short-haul grains providing stable employment. Latin America is also showing early signs of improved cargo flow as agricultural preparations begin, albeit still weeks away from meaningful export volumes. While Handysize earnings are seasonally muted, the base from which they are correcting remains higher, maintaining the theme that this year’s market is avoiding the deeper troughs of last year and is positioned for a more controlled seasonal recovery.

Taken together, the dry bulk market’s early-2026 performance illustrates a familiar seasonal dip layered onto a structurally stronger foundation. Iron ore remains the anchor, and while inventories are heavy, import momentum remains relatively steady. Coal and grain flows continue to support Panamax and Ultramax employment, even as seasonal softness temporarily suppresses earnings. Minor bulks are moving through their typical Q1 contraction, yet underlying trade lanes remain stable and vessel lists balanced. Looking ahead, the key variables shaping the next phase of the market include China’s policy stance following its January economic signals, the strength and timing of Brazil’s grain exports, India’s energy and industrial demand, and the broader impact of easing global financial conditions. Overall, the market appears better positioned than a year ago. As seasonal volumes build into Q2, the prospect of a more constructive year – anchored by higher lows and firmer structural support – remains credible.

Data source: Doric