India’s salt sector is a global heavyweight, ranking among the top three producers worldwide with output averaging 30 mln mt annually. Moreover, India became the world’s largest salt exporter in 2024, shipping 17.3 mln mt on bulkers, propelled by an extraordinary surge in Chinese demand. Exports to China alone topped 10 mln mt, doubling y-o-y and underscoring the structural reliance of its chlor-alkali and soda ash sectors on low-cost Indian solar salt.

World’s Largest Salt Exporter (2024)

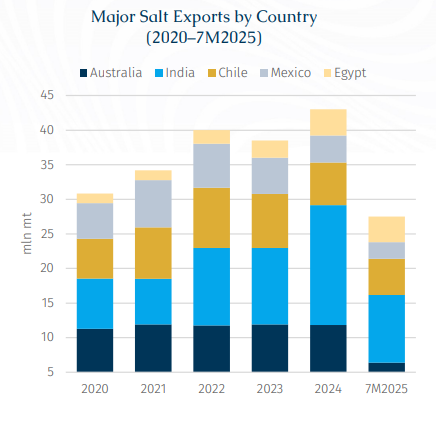

India accounted for nearly 29% of world salt trade in 2024, ahead of Australia (~19%) and Chile (~15%). In the first seven months of 2025, exports rose 11.7% y-o-y, keeping India firmly on course to retain its top position. Gujarat contributes close to three-quarters of national output, with significant shipments also coming from Tamil Nadu’s coastal pans at Thoothukudi. Reliance on solar evaporation keeps costs among the world’s lowest, underscoring Indian exporters’ competitive edge.

In the first seven months of 2025, India exported 9.8 mln mt, of which 8.2 mln mt were to the Far East. In comparison Australia shipped 6.3 mln mt most of which went to Asia. While both countries primarily utilise Supramaxes and Handymaxes, their market orientation differs. India focusses on China, to where it shipped 5.5 mln mt (compared with Australia’s 1.3 mln mt). Meanwhile, Australia focusses on Japan where it exported 1.7 mln mt (compared with India’s 0.6 mln mt). This means the two compete directly in China and Southeast Asia using the same vessel segments, but Australia’s position in Japan is more entrenched. Meanwhile, Chile remained Atlantic-oriented, sending 3.5 mln mt to the US East Coast and 1.0 mln mt to East Coast South America, and Egypt split its volumes between the US East Coast (1.5 mln mt) and the Eastern Mediterranean (0.9 mln mt). Mexico contributed 1.5 mln mt to the Far East (much of it heading into Japan) and smaller parcels to the North Pacific and US East Coast.

Production Prospects - Upside and Ceiling

India’s domestic salt output rose about 10.1% y-o-y in 2024 to a 33.7 mln mt, underpinned by favourable dry conditions and the country’s low-cost solar evaporation model. Industrial demand remains a key anchor, with more than 60% of national salt consumption driven by chlor-alkali, soda ash, and allied sectors, thus ensuring steady offtake. Infrastructure improvements under the Sagarmala programme, a government initiative focused on port modernisation, coastal connectivity, and lowering logistics costs, further reinforced production momentum. Based on these fundamentals, output may reach about 35.8 mln mt in 2025. However, this outlook is tempered by risks from lease renewal delays in Gujarat’s salt pans, tightening environmental scrutiny, and climate volatility.

North Asia’s Demand Pull

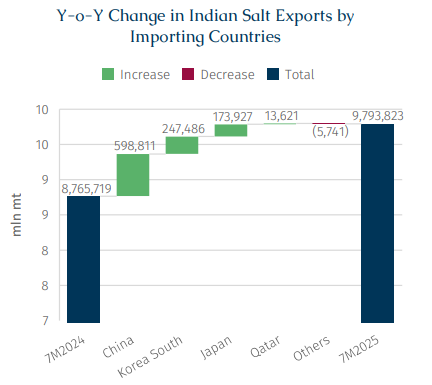

Unlike sugar, where India both imports and exports depending on domestic balances (see Page 7 for further details), salt is primarily exported. Cargoes in 7M2025 were lifted mainly from west coast ports, led by Kandla (7.6 mln mt), Mundra (1.1 mln mt), and Jakhau (1 mln mt), largely on Supramaxes. Trade flows remain heavily concentrated, with China, South Korea and Japan as the main buyers driven by industrial demand.

China accounted for more than half of India’s salt exports in Jan–Jul 2025, with 5.55 mln mt (+12.1% y-o-y), underlining the demand from its vast chlor-alkali and soda ash sectors. According to Argus, alumina refining alone accounts for 32% of caustic soda demand, highlighting the depth of industrial pull. Policy is not aimed at cutting imports but at tightening sustainability: the MIIT’s “14th Five-Year Plan for Petrochemicals” requires new chlor-alkali projects to adopt membrane electrolysis technology and demonstrate waste-recycling capabilities before approval.

South Korea lifted 1.72 mln mt in Jan–Jul 2025 (+16.8% y-o-y), reflecting demand for chlor-alkali for PVC, synthetic fibres, and semiconductors. Meanwhile, demand for food processing is smaller. Government policy focuses on supply diversification and traceability. Notably, following a series of scandals in 2023, the Ministry of Oceans and Fisheries introduced new monitoring rules requiring all imports to meet safety and origin-labelling standards. Furthermore, in April 2025, US Customs banned imports from Taepyung Salt Farm over forced labour allegations, pushing Seoul to reinforce oversight and modernisation.

Japan lifted 0.6 mln mt in Jan–Jul 2025 (+37.9% y-o-y), the fastest growth among the three buyers but still modest in absolute terms. Domestic production remains structurally constrained, and Japan sources most of its industrial salt from Australia, with India serving as a smaller complementary supplier. However, the purity of Indian solar salt supports a niche role in Japan’s supply mix, particularly for the chlor-alkali and food-processing industries.

Supramax Backbone, Panamax Support

In 7M2025, India’s salt exports were overwhelmingly carried by Supramaxes and Panamaxes, which together accounted for more than 90% of liftings. Supramaxes hauled 7.35 mln mt (75.1% of total trade), reflecting their suitability for the typical 50–60,000 Dwt parcel sizes lifted out of Kandla, Mundra, and Jakhau. These vessels align closely with the requirements of major North Asian buyers, making them the backbone of India’s salt export logistics.

Panamaxes lifted 1.48 mln mt (15.2%), to China, South Korea, and Taiwan. Their deployment reflects the economies of scale sought by large industrial buyers shipping bigger parcels on longer-haul routes. Though less frequent than Supramaxes, Panamax employment highlights the growing concentration of demand among a handful of key industrial consumers.

The prominence of Supramaxes and Panamaxes in India’s salt exports is reinforced by their heavy inbound flows at Mundra and Kandla. These ports handle a wide mix of bulk commodities yet are also India’s principal salt loading hubs. In 7M2025, Supramaxes discharged about 6 mln mt of coal, petcoke, fertilisers, and gypsum, while Panamaxes brought in around 5 mln mt of coal. This inbound activity ensures that vessels arriving laden with industrial cargoes can reload salt on the outbound leg to China, Japan, and Southeast Asia, thereby reducing ballast requirements.

India’s salt industry is set to deliver another record year in 2025, with output projected near 35.8 mln mt, supported by Gujarat’s favourable dry conditions and the country’s entrenched low-cost advantage. Exports are forecast to reach 18.4 mln mt in 2025, a 6% increase over last year’s record.

If this year’s exports do surpass last year's volume (17.3 mln mt), Panamax deployment could rise further in 2026 as Chinese buyers consolidate shipments.