In 2010, the cotton market witnessed one of the most dramatic squeezes in recent memory. Torrential monsoon rains in Pakistan and severe weather in China devastated global harvests, while demand from Asian textile manufacturers surged. As inventories dwindled, India abruptly restricted exports to protect domestic supply, sending prices skyrocketing. Cotton futures surged past $2.00 per pound in early 2011 – levels not seen since the U.S. Civil War. The panic became visceral. Mills in Bangladesh and China were operating with just days of inventory. In the U.S., brands like Levi’s and Hanes publicly warned of pressure on margins. The frenzy reached such a pitch that one Turkish spinner reportedly chartered a private jet to fly in bales from Central Asia – an extraordinary response to an extraordinary squeeze.

While no such jet was dispatched from Santos this week, the urgency that gripped the Panamax market felt strikingly similar. After months of stagnation, the Panamax market burst into life this week, driven by a sudden and significant tightening of tonnage in the East Coast South America (ECSA) region. The Baltic P6 Index surged by 21.3 percent week-on-week, closing at $16,909 daily – marking one of the strongest weekly gains in recent years. To put this into perspective, over the last 385 trading weeks since 2018, only 14 have recorded a weekly increase of more than $3,000 on this index. The pace and timing of this rally caught many off guard, particularly as early July is typically a quiet period for ECSA grain activity, nestled between the end of the soybean season and the beginning of the corn export cycle. This unexpected surge in sentiment seems to stem from mounting evidence of a supply squeeze, with charterers scrambling for tonnage and owners holding firm on offers. In a matter of days, a market that had struggled to find a floor through much of the first half of the year was reignited.

The rally was particularly surprising given the time of year. July typically marks a quiet interlude for dry bulk activity in ECSA grain exports, as it falls between the end of the soybean season (March to June) and the start of the corn export window (late August through October). Cargo availability during this stretch is usually limited, with most inland soybeans already cleared from ports and safrinha corn still making its way toward terminals. This seasonal gap often leads to softer freight rates, as owners reposition vessels or accept lower returns to bridge idle time. July, in short, is rarely the setting for such a powerful market surge. Yet this year defies that script. As demand spiked and available tonnage tightened, charterers were caught short. Owners, buoyed by a sharp shift in sentiment, pushed offers higher, with bids scrambling to catch up. The result: a rally that pulled the entire Panamax market upward, fueled by the very fundamentals that had long been assumed dormant.

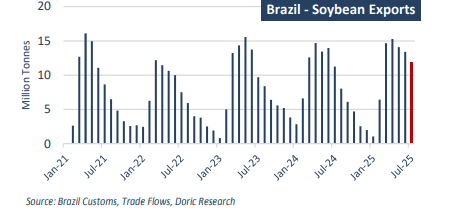

The roots of this Jolt are embedded in trade flow dynamics that have evolved throughout the year. The campaign began on shaky ground when, in January, China suspended several major Brazilian exporters following multiple detections of pesticide residue. These firms collectively accounted for nearly a third of Brazil’s soybean exports to China in 2024. Even with an impressive March rebound, total Q1 soybean exports were up by just 0.66 percent year-on-year. However, volumes gained momentum in the following months. By the end of May, Brazil had shipped 51.6 million tonnes of soybeans – a 2.88 percent increase over the same period in 2024.

In mid-May, China reinstated five of the previously suspended exporters, a move that rapidly reignited Brazilian flows to Asia. Since then, the pace has accelerated. As of July 7, LSEG data tracked 67.4 million tonnes of soybean exports from Brazil since February – 3 percent ahead of last year’s record-breaking run, with 47.6 million tonnes headed to China. The July line-up reinforces the bullish narrative: 10.4 million tonnes are scheduled to load, a 12 percent year-on-year increase. According to ANEC, Brazil’s July soybean exports are now expected to hit 11.93 million tonnes, up from 9.6 million tonnes in the same month last year. Driving this surge is Brazil’s massive 2025 harvest, which yielded 169.3 million tonnes of soybeans – 22 million more than in 2024. Exporters are pushing volumes aggressively, particularly as uncertainty grows around U.S. trade negotiations. Buyers are keen to secure Brazilian product before the U.S. harvest becomes available in September, anticipating potential geopolitical risks in the second half of the year. Meanwhile, corn looms on the horizon. Brazil’s corn output is expected to reach 128.3 million tonnes this season – an 11 percent year-on-year increase. StoneX projects corn exports at 42 million tonnes, up from 38.5 million in the previous cycle. But logistical friction may emerge as soybean and corn cargoes begin competing for terminal capacity. Should Chinese demand for soybeans remain firm, corn may face port congestion and scheduling conflicts.

For months, the Panamax segment was weighed down by oversupply and tepid demand. Then, almost overnight, a spark caught fire. Owners stopped chasing stems; charterers began chasing ships. The charts moved, the sentiment flipped, and the market roared back to life. As history often reminds us, turnarounds in commodity and shipping markets sometimes come not with a whisper, but with a bang.

Data source: Doric