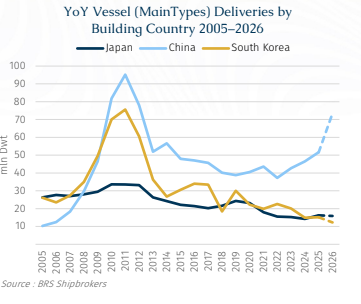

Japan’s shipbuilding capacity for bulkers, tankers, and container ships has undergone significant change over the past two decades. In 2005, total deliveries stood at approximately 26 mln Dwt—comprising 17 mln in bulkers, 1 mln in tankers, and 8 mln in container ships—representing around 25% of global shipbuilding activity at the time. By 2010, deliveries had surged to nearly 34 mln Dwt (22 mln bulkers, 2 mln tankers, and 10 mln containers), driven by booming demand during the 2005–2008 commodity supercycle. China’s iron ore imports had nearly doubled, while global oil demand rose by 20%, fuelling a sharp increase in bulker and tanker orders. Despite the Great Recession of 2008, causing a 50% collapse in new orders, deliveries remained strong in 2010, supported by pre-crisis contracts and export credit assistance.

The lagged effects of the global financial crisis began to take hold by 2015, with Japan’s vessel deliveries falling to around 22 mln Dwt (20 mln bulkers, 1 mln tankers, and 1 mln container ships), amid global oversupply and China’s market share reaching 40%. This period also marked a phase of structural contraction in Japan’s shipbuilding sector. Sumitomo Heavy Industries exited shipbuilding in 2022, closing its Yokosuka yard due to rising costs and foreign competition. Mitsui E&S shut its Chiba yard in 2021, relocating operations to China, while Sasebo Heavy Industries suspended newbuilding in 2022. These developments reflect broader industry consolidation and Japan’s diminishing global shipbuilding presence. The decline continued, with production dipping to approximately 23 mln Dwt in 2020 (18 mln bulkers, 1 mln tankers, 4 mln containers), reflecting weakened newbuilding orders post-COVID-19. Although Japanese shipyards do not routinely disclose orderbook for all vessel type data—implying that forward-looking estimates may understate actual volumes in 2025–26 deliveries are projected to stabilise around 16 mln Dwt, with forecasts indicating 16.2 mln Dwt in 2025 and 15.8 mln Dwt in 2026.

Japan’s modest recovery is underpinned by its 2020 zero-emissions strategy and the IMO’s decarbonisation targets, which have stimulated demand for high-specification, dual-fuel ships. Although overall bulker output has fallen, Japan remains a leader in this segment thanks to its quality-driven legacy. Recent orders—such as Pacific Basin’s dual-fuel vessels from Nihon and Imabari, and Tsuneishi’s pledge to produce only dual-fuel ships by 2035—highlight the country’s strategic pivot toward high-value, low-emission tonnage.

Looking towards 2040, Japan aims to lead in autonomous shipping and zero-emission technologies, with the Nippon Foundation backing efforts to make 50% of the domestic fleet autonomous. These ambitions reinforce Japan’s role as a maritime tech leader. However, bulk carrier orders may stay muted amid China’s dominance and a projected post-2025 decline in coal trade, according to the IEA.

China’s Bulker Supremacy

Japan’s Niche Strategy: Japan is projected to deliver 16.2 million dwt of new tonnage across all vessel types in 2025, surpassing South Korea but still trailing far behind China, which is expected to produce more than twice as much. Despite cost pressures, Japanese shipyards excel in high-value niches like methanol-ready bulkers and vehicle carriers. Their strength lies in domestic demand, driven by technological specialization in energy-efficient, eco-friendly vessels, aligning with local shipowners’ sustainability goals. This focus sustains shipyard activity and supports stable coal imports for steel and power needs. Japan’s future hinges on domestic charterer demand and green innovation leadership, as Chinese builders like CSSC and Yangzijian Shipbuilding advance lower-cost, low-emission alternatives.

Chinese Dominance: Chinese shipbuilding output across all vessel types peaked at 95.2 million Dwt in 2011, fell to 47.9 million by 2015, but has since rebounded strongly. With 73.5 mln Dwt expected in 2025, China remains the largest shipbuilding nation by volume. This resurgence has been supported by robust state backing, attractive export credit terms, and cost competitiveness across vessel types. While South Korea continues to lead in high-specification tankers and LNG carriers, China has secured global leadership in building conventionally fuelled bulkers and container ships. In 2024, Chinese shipyards delivered over 60% of global merchant vessel output, consolidating their dominance in volume-based segments and steadily expanding into dual-fuel and methanol-ready bulker designs.

Not the Biggest — Just the Best

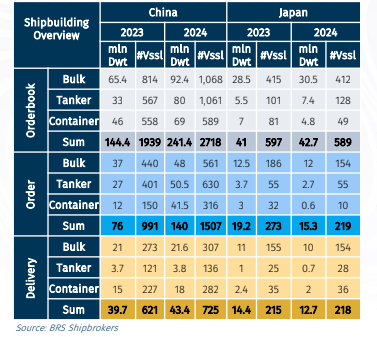

In 2023 and 2024, the bulk carrier orderbook breakdown highlighted China's dominance and Japan's continued resilience, driven by distinct factors. China's bulk carrier orderbook grew to 92.4 mln Dwt in 2024, up from 65.4 mln Dwt in 2023, reflecting a sharp rise in new orders from 37 mln Dwt to 48 mln Dwt, driven by Southeast Asian infrastructure demand for raw materials like iron ore. Japan's orderbook, in contrast, expanded more modestly, increasing from 28.5 mln Dwt in 2023 to 30.5 mln Dwt in 2024. Japan’s orders fell slightly to 12 mln Dwt in 2024 from 12.5 mln Dwt, driven by demand for fuel-efficient vessels amidst stringent IMO environmental regulations.

However, new global bulk carrier orders are expected to drop 26% in 2025 due to factors including high prices, fuel uncertainty, and concerns over oversupply, with approximately 600 newbuilding's expected. Deliveries are also shifting, with China’s deliveries increasing slightly to 21.6 mln Dwt from 21 mln Dwt, while Japan’s fall to 10.7 mln Dwt from 11 mln Dwt, focusing on green ship builds. Geopolitical factors, such as the US - China trade disputes, continue to influence freight rates and market sentiment, while US - Japan collaboration seeks to challenge China’s 55.7% global market share.

In Japan’s 2023-2024 maritime sector, Handysize vessels led demand, with orders jumping from 52 to 91 and deliveries from 52 to 70, serving regional trade routes in Asia (Southeast Asia, China, South Korea) for dry bulk commodities like steel, cement, grains, and fertilizers, fuelled by a 26% rise in meat exports and robust logistics. Panamax vessels showed stable demand, with orders slightly up from 19 to 21 and deliveries steady at 21, supporting balanced trade in grains and coal across Indo-Pacific routes. Capesize/Neo vessels, however, saw growing demand with orders rising from 18 to 25, but deliveries fell from 18 to 14, reflecting Japan’s need for large bulk carriers to import coal and iron ore, though supply constraints hinder fulfilment.

US - China Trade Tensions

The US has introduced escalating fees on Chinese-owned ($50/NT) and Chinese-built ($18/NT) vessels, aiming to reduce reliance on China's shipyards, which currently control over 67% of the global orderbook. These measures could prompt shipowners—particularly those involved in US trade—to reassess their procurement strategies and potentially shift towards Japanese shipyards, which specialize in bulkers due to their higher delivery volumes. However, such a shift presents challenges. Japan's shipyards may face capacity constraints, and decisions will likely depend on each owner's risk tolerance, cost analysis, and broader fleet strategy. Nevertheless, the added risks and rising costs could gradually diminish China's recent dominance in the shipbuilding sector, potentially creating space for Japan to focus more on bulker construction.

Policy and Structural Challenges

Japan champions fair competition at the IMO, challenging China’s estimated $15 billion in subsidies. Its own $ 1.29 billion (JPY 200 billion) Green Innovation Fund and Maritime Cluster Policy support eco-ship development and R&D but are modest compared to China’s annual support under the 14th Five-Year Plan and South Korea’s $5 billion modernisation and labour schemes, which include hiring Southeast Asian workers. Japan’s expansion is also constrained by structural factors: an ageing workforce—with around 40% over the age of 55—and limited coastal land for new shipyards. While vocational training $64.52 million (JPY 10 billion in 2024), immigration reforms, and public-private partnerships aim to address labour and capacity issues, progress remains slow. These structural challenges continue to limit Japan’s ability to scale production.

Scaling the Future

Japan’s shipbuilding sector, though highly advanced, faces structural hurdles—aging labour, limited land, and slow policy reform—that restrict rapid expansion. Operating near full capacity with orderbooks into 2028, Japanese yards lack the scale to compete with China’s volume-driven growth. However, Japan is leaning into high-specification niches, particularly green bulkers. Recent dual-fuel orders from Pacific Basin and Tsuneishi’s 2035 green-only pledge reflect this shift. Rather than matching China’s output, Japan’s strategy prioritizes quality, environmental compliance, and close domestic ties—offering long-term resilience in a tightening regulatory environment.