Global industrial production increased by 1.6 percent year-on-year in the December quarter of 2023, as reported in the latest Resource and Energy Quarterly by the Australian Department of Industry, Science, and Resources. Positive annual growth reflects lower energy prices in many major economies, as well as rebounding industrial activity in China following a weaker 2022. Conversely, regarding international trade, merchandise volumes declined by 1.9 percent year-on-year in 2023. The WTO expects a recovery of trade volume to 3.2 percent in 2024; however, rising trade distortions and geopolitical fragmentation are expected to weigh on global trade going forward. The IMF noted 3,200 new trade restrictions imposed in 2022 and about 3,000 in 2023, up from about 1,100 in 2019.

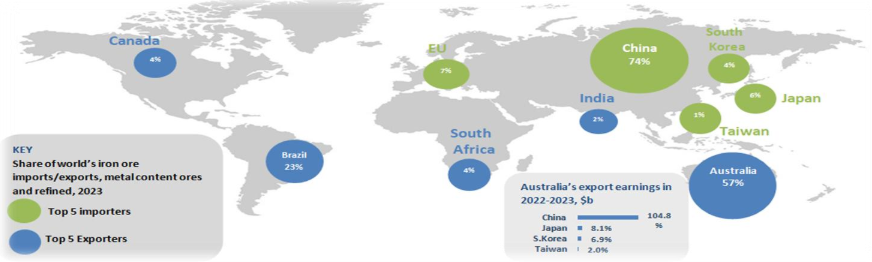

In the realm of iron ore trade, China's imports surged to record levels in 2023. Combined shipments from Australia, Brazil, South Africa, and Canada reached an estimated 1,370 Mt in 2023, marking a 2.6 percent increase from 2022. Notably, iron ore shipments from Brazil rose by 21 Mt in 2023. Vale, which dominates over 80 percent of Brazil’s iron ore production, anticipates producing 310-320 Mt in 2024, aligning with the 315 Mt produced the previous year. Australia exported 893 Mt of iron ore in 2023, up by 1.1 percent. Over a five-year outlook, Australia’s iron ore production is projected to increase by 1.9 percent a year, to reach 1,069 Mt by 2029. Beyond Australia and Brazil, exports are expected to receive a boost from additional supply originating from Canada and India, as well as from new projects in Africa. One such project is the Simandou mine in Guinea, projected to produce over 150 Mt per annum, targeting first production in 2025-26. Over the next five years, global trade in iron ore is forecasted to grow by 2.1 percent annually, according to the Australian department of industry, science and resources.

Seaborne thermal coal demand also experienced significant growth in 2023, reaching a peak of 7 percent. However, as this peak period passes, weak global demand is expected to lead to a decline in exports from 1,099 Mt in 2023 to 1,034 Mt in 2029. Indonesia maintained its position as the world’s top exporter of thermal coal in 2023, with exports totaling 521 Mt – up by 12 percent year-on-year. However, Indonesia’s exports are expected to undergo a slight decline over the next five years to 507 Mt by 2029. Following sanctions from the EU, China emerged as Russia’s largest export market for coal. In 2023, Russia exported 75 Mt of coal to China, a 60 percent increase year-on-year. However, this trend could be influenced by China’s decision to reinstate import tariffs on non-Free Trade Agreement countries. Seaborne thermal coal exports from the US are anticipated to decrease to 39 Mt by 2029. Exports surged by 23 percent in 2023 to a five-year high of 44 Mt. Likewise, seaborne thermal coal exports from Colombia are projected to decline, due to the country’s decarbonization goals and depleting reserves, from 56 Mt in 2023 to 39 Mt by 2029. In sync, South African exports are also expected to drop from 74 Mt in 2023 to 59 Mt in 2029. Australian thermal coal exports, on the other hand, finished 2023 on a strong note, with 18.9 Mt exported in December – the highest record since July 2021. Australian exports are expected to hold steady at 210 Mt in the next five years, with near-term outlook being favourable. Global seaborne imports of thermal coal are expected to fall at an average annual rate of 2.6 percent over the next period from 1,120 Mt in 2023 to 957 Mt by 2029.

Global demand for metallurgical coal soared to 317 Mt in 2023, marking an 8 percent increase from 2022, with India and China being the main drivers. In a significant development, India surpassed China to become the world’s leading importer of seaborne metallurgical coal. However, China still holds the top spot for overall (land and sea) imports. Demand from other markets remained relatively stable. US exports performed strongly in 2023, reaching 43 Mt. Seaborne exports from the US are projected to remain flat in the next years, with a slight decline to 42 Mt by 2029. Mongolia experienced a substantial increase in metallurgical coal exports in 2023, with volumes more than tripling from 14 Mt in 2022 to 48 Mt. However, exports are expected to decrease to 35 Mt by 2025 and remain around that level thereafter. On the other hand, exports of Canadian metallurgical coal are anticipated to decline from 29 Mt in 2023 to 26 Mt by 2029. Russia witnessed a robust growth in metallurgical coal exports in 2023, rising to 44 Mt compared to 37 Mt in 2022. Over the next period, Russian seaborne exports are forecasted to experience a slight decline to 42 Mt by 2029. Australia’s metallurgical coal production and exports have faced constraints in recent years due to adverse weather conditions and logistical challenges. However, higher production in NS Wales and Queensland is expected to boost exports from 156 Mt in 2022-23 to 175 Mt by 2029. Global trade in metallurgical coal surged to 349 Mt in 2023, representing an almost 12 percent increase from 2022. However, world exports are anticipated to decline to 333 Mt by 2029.

Looking ahead, Australia’s Department of Industry, Science, and Resources anticipates that Chinese demand will continue to exert a significant influence on commodity markets. However, the department also highlights India's robust economic growth. India's expanding manufacturing base and substantial infrastructure spending point toward an increase in per capita consumption of resource and energy commodities. Additionally, the ongoing global energy transition and efforts towards decarbonizing steel and aluminum production, along with supply chain transformations, are expected to impact growth and trade patterns in the coming years. Considering these overarching themes, recent trends in the S&P market suggest a positive mid-term outlook for the dry bulk sector.

Data source: Doric