The Baltic Dry Index retreated into the red on Tuesday amid headwinds for the capesizes. Among the commodities, base metals and iron ore were among the day’s winners, while energy prices generally recorded modest moves.

By Ulf Bergman

Macro/Geopolitics

Amid the continued challenges for the Chinese economy and an ongoing rout for the country’s equity market, the People’s Bank of China announced that it is lowering the required reserve ratio for the country’s banks with effect from early February. The move aims to inject more money into the banking system to support lending and economic growth, as foreign investors are taking an increasingly dim view of the outlook for the world’s second-largest economy. Still, the initiative is unlikely to be sufficient to restore faith in the Chinese economy, and more support measures can be expected to materialise in the coming weeks.

Commodity Markets

Crude oil prices had a relatively quiet session on Tuesday as expectations of lower demand balanced fears over supply disruptions. The March Brent futures declined by 0.6 per cent, ending the day at 79.55 dollars per barrel. Little has changed during today’s session, with the contracts trading approximately half a per cent above yesterday’s close.

After substantial losses on Monday, European natural gas markets had an uneventful session yesterday. Limited changes in demand saw the front-month TTF futures closing broadly unchanged for the day at 27.23 euros per MWh. However, after initial losses, the contracts have recovered in today’s session and are trading around two per cent above Tuesday’s settlement.

As markets assessed the supply and demand situation, coal prices also had a session of limited price moves . The February futures for delivery in the port of Newcastle shed 0.6 per cent, ending the day at 123.25 dollars per tonne, while the Rotterdam contracts edged up marginally to 92.50 dollars per tonne.

Expectations of further support for the Chinese economy supported iron prices on Tuesday. After beginning the week with limited losses, the front-month contracts listed on the SGX rose by 2.4 per cent, settling just shy of 132 dollars per tonne. Yesterday’s narrative has carried into today’s session, with gains of more than two per cent.

The base metals ended Tuesday ’s session in the black as traders grew increasingly concerned over the global supply situation. The three-month aluminium futures listed on the LME led the way higher with a daily gain of 3.2 per cent, while the zinc and nickel contracts advanced by 2.6 and 1.9 per cent, respectively. Copper was the session’s laggard, with a modest 0.7 per cent rise.

Tuesday’s session was also uneventful for the grain futures trading on the CBOT. The March wheat futures closed unchanged for the day, while the corn contracts edged up by 0.2 per cent. On the other hand, the soybean futures for delivery in March gained 1.2 per cent amid some concerns that the Brazilian harvest may fall short of expectations.

Freight and Bunker Markets

After three consecutive sessions of gains, the Baltic Dry Index retreated into the red yesterday. The headline indicator declined by 3.0 per cent on the back of weakness for the capesizes. The sub-index for the largest vessels declined by 7.6 per cent amid soft demand in the Pacific and Indian Oceans and rising tonnage supply in the Atlantic. In contrast, the freight rate gauge for the panamaxes rose for a seventh consecutive session as order volumes remained robust. For the smaller segments, gains were more limited. The index for the supramaxes rose by 0.6 per cent, supported by demand, while the gauge for the handysizes increased by 0.3 per cent amid pressure on tonnage supply.

On Tuesday, the Baltic Exchange’s wet freight gauges had a day of primarily adverse developments. The dirty tanker indicator declined by 3.6 per cent, while the LNG and LPG indices shed 8.2 and 0.5 per cent, respectively. In contrast, the gauge for the clean tankers surged by 16.1 per cent as tonne-mile demand was seen rising in the wake of developments in the Red Sea.

After a relatively quiet start to the week, the trading in bunker fuel had a mixed session on Tuesday. In Singapore, the VLSFO declined by 0.4 per cent while gaining 1.8 per cent in Houston and 1.0 per cent in Rotterdam. The MGO recorded gains of around one per cent in Singapore and Rotterdam while declining by 2.0 per cent in Houston.

The View from the Shipfix Desk

The announcement that China’s central bank is lowering the required reserve ratio for the country’s commercial banks from next month highlights that Beijing remains concerned over sluggish growth rates. Also, the manner in which it was presented, i.e. with extensive advance warning, suggests that the Chinese leadership is growing increasingly worried over developments. While last year’s economic growth was broadly in line with the official target of somewhat more than five per cent, the level was nevertheless conservative by Chinese standards.

According to data released last week, China’s industrial production expanded by 6.8 per cent in December compared to a year earlier, somewhat more than expected. Last month’s reading followed a stronger-than-expected output in November as well. However, base effects played a role as China’s extensive anti-COVID measures were being dismantled during the final months of 2022. As the Chinese New Year approaches, markets will, in line with tradition, have to wait for the joint reading for January and February, which is due for release towards the end of March. Hence, in the meantime, alternative indicators for the state of the Chinese economy will have to be employed.

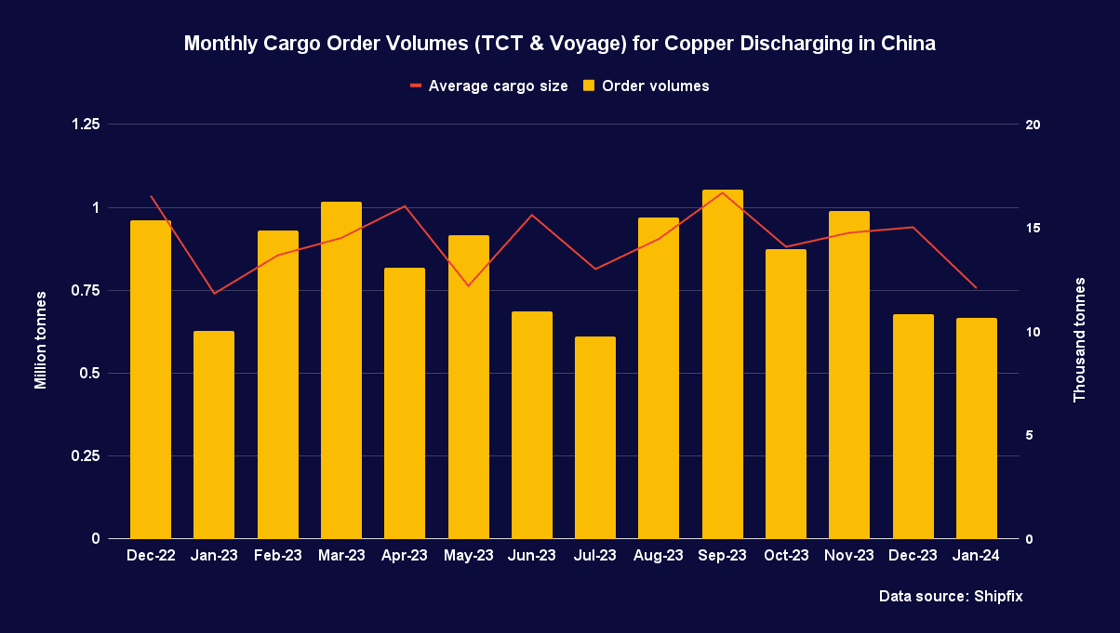

Copper is often seen as a bellwether for economic and industrial activities, given its central role in modern manufacturing. While copper prices have been moving higher over the past week, they remain around two per cent below the levels recorded at the end of last year. A stronger dollar has contributed to the decline, but uncertainty over Chinese demand has also been a factor.

Cargo order volumes for copper discharging in Chinese ports are on course for a month-on-month increase, with the aggregate for the month so far at par with the reading for the whole of December. Also, assuming a high degree of linearity for the remainder of the month, cargo order volumes would top the volumes recorded in January last year by around 40 per cent. However, bearing in mind that the situation is nearly the reverse of the previous month, the linear projection for the month looks less impressive. The aggregate for the past two months could be on track to match what was recorded during the same period last year. Hence, the data for the red metal suggest that Chinese growth during the first months of the year will be subdued.

Data Source: Shipfix