The past week witnessed extensive volatility across the global commodities markets as traders digested contradicting signals. Weaker-than-expected Chinese data and lower demand in the Northern Hemisphere contributed to falling energy prices. At the same time, metals and agricultural commodities generally gained some ground over the course of the week. Dry bulk freight rates remained on their recent downward trajectory, with the Capesizes especially severely hit.

By Ulf Bergman

Macro/Geopolitics

Last week saw the release of several contradictory signals for the health of the global economy. Two sets of Chinese manufacturing PMI data pointed in opposite directions. The weaker-than-expected reading for the official gauge of the sentiments in the industrial sector suggested that a contraction is underway, while the alternative Caixin indicator was stronger-than-expected and indicated that manufacturing is still expanding modestly.

On the other side of the Pacific, the US labour market signalled continued resilience, with payroll data for May showing that an unexpectedly high number of jobs were created during the past month. In contrast, the ISM PMI gauge for the US manufacturing sector was marginally lower than consensus and continued to suggest that industrial production in the world’s largest economy has peaked and is declining.

The week ahead will see the release of Chinese trade and inflation data. A weak reading for the latter will provide the Chinese leadership with more room for manoeuvre to stimulate the world’s second-largest economy amid an increasingly patchy recovery.

Commodity Markets

Despite solid gains on Friday, crude oil declined over the course of the past five trading sessions amid volatile conditions. After gaining 2.5 per cent during the week’s last day, the August Brent futures settled at 76.13 dollars per barrel, 1.1 per cent below the previous week’s close. Friday’s positive momentum has carried into the new week, with the contracts advancing by around two per cent during today’s early trading following news that Saudi Arabia is unilaterally reducing its oil output by one million barrels.

European natural gas futures also had a volatile week, with reports of an unscheduled outage for a Norwegian gas field briefly contributing to prices recovering some recent losses. However, the front-month futures ended the week at 23.69 euros per MWh, 5.4 per cent below the previous week’s closing price. The contracts have maintained Friday’s bullish sentiments in today’s session amid gains of more than ten per cent.

While Friday’s trading saw a reversal of fortunes, with gains for Asian and European coal futures, the dirtiest of fossil fuels nevertheless recorded a week of losses. Demand remained soft following the end of the heating season and lower natural gas prices. The Newcastle futures for delivery in July declined by 2.2 per cent over the past week and settled at 134.15 dollars per tonne on Friday. The front-month contracts for delivery in Rotterdam recorded a weekly decline of 0.8 per cent, as a 2.5 gain on Friday offset most of the earlier losses. The futures ended Friday’s trading at 93.70 dollars per tonne.

Despite the weaker-than expected official PMI data in China, the iron ore futures listed on the Singapore Exchange advanced over the past week. The front-month contracts recorded a weekly gain of 6.1 per cent and ended the week at 103.90 dollars per tonne. The contracts have begun the new week on a positive note, reaching a six-week high on Monday amid rumours of more support measures for the Chinese property sector in the near term.

A weaker dollar and tentative optimism over Chinese demand saw most of the base metals recording minor gains last week. The three-month copper and aluminium futures advanced by more than one per cent during the previous week, while the nickel contracts edged up by 0.2 per cent. In contrast, the zinc futures declined by 1.6 per cent during the period.

The grains and oilseed futures listed on the Chicago Board of Trade recorded limited gains during the past week, with concerns over the flow of agricultural commodities from Ukrainian ports contributing to higher prices. The July wheat and corn futures advanced by 0.5 and 0.8 per cent, respectively, while the soybean contracts gained 1,1 per cent.

Freight and Bunker Markets

While the past week was shorter than usual because of a public holiday in the UK, there was no shortage of drama during the remaining four days. The headline Baltic dry Index declined by 21.6 per cent over the past four sessions, with the Capesizes providing much of the headwinds.

The sub-index for the largest vessels slumped by 33.7 per cent as cargo ordering activities in the segment remained subdued. While the mid and small-sized vessels faced less pressure, they all recorded weekly declines. The Panamaxes saw their freight rate indicator declining by 8.0 per cent last week after remaining unchanged on Friday, the first non-negative session in more than three weeks. The gauge for the Supramaxes dropped by 13.4 per cent during the week amid weak demand, while the Handysizes shed 7.3 per cent.

Among the Baltic wet freight indicators, only the one for the dirty tankers ended the past week in the red. Continued concerns over demand for seaborne transportation of crude oil saw the gauge declining by 7.6 per cent. In contrast, the freight index for the clean tankers advanced by 0.9 per cent. The indicators for the gas carriers had the week’s strongest performances, with the LNG freight rates increasing by 20.9 per cent and the gauge for LPG carriers gaining 2.9 per cent.

Headwinds in the crude oil markets contributed to bunker fuel prices retreating over the past week in Singapore and Houston. However, after five volatile sessions, they ended the week broadly unchanged in Rotterdam. VLSFO prices declined by 3.1 per cent in Singapore and 2.2 per cent in Houston, while the trading in MGO recorded a weekly loss of 2.1 per cent in both maritime hubs.

The View from the Shipfix Desk

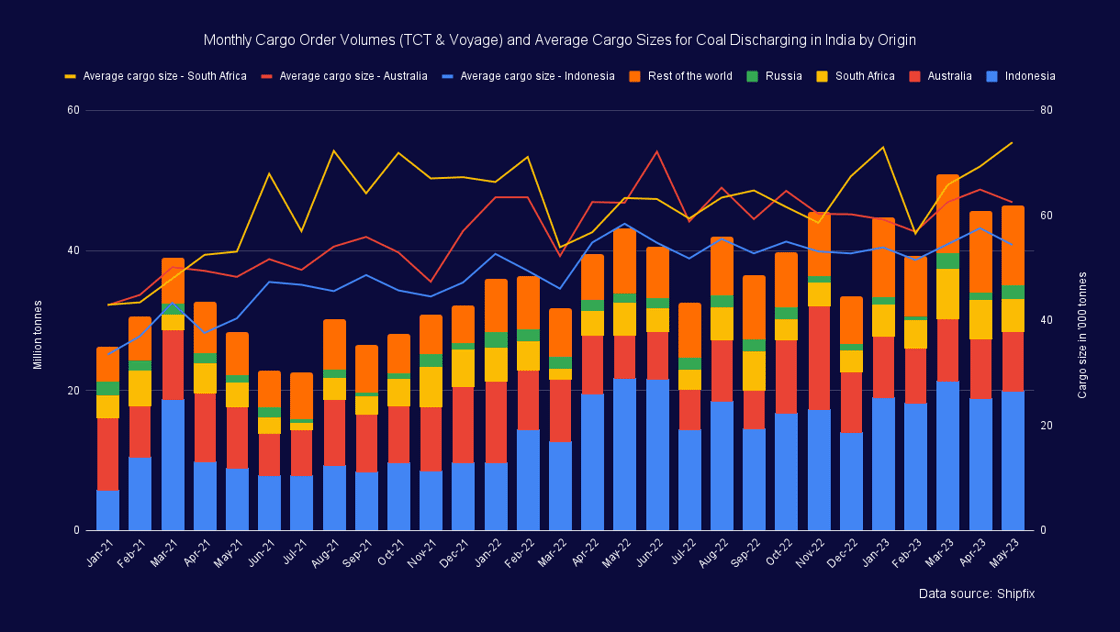

While European coal imports remain on a downward trend, Indian imports of the commodity have been buoyant. A spike in cargo order volumes for coal discharging in India during March has translated into very substantial import volumes during the past month. However, it looks unlikely that the high import volumes will be sustained in the coming months. After peaking at the end of the first quarter, demand for seaborne transportation of the fossil fuel to the South Asian country has softened. The forward-looking nature of Shipfix’s cargo order data set suggests that actual monthly imports could decline by around ten per cent in the coming months.

Average cargo sizes for shipments from Australia and Indonesia to India have seen a mean reversion during the past month amid marginal declines. In contrast, the average for imports from South Africa has remained on the upward trajectory that began during the early parts of the year.