Summary

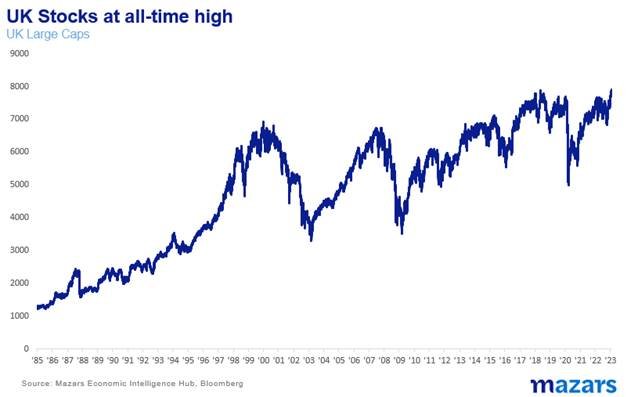

Equity and bond markets continue to rally, with the FTSE 100 hitting all-time highs last week.

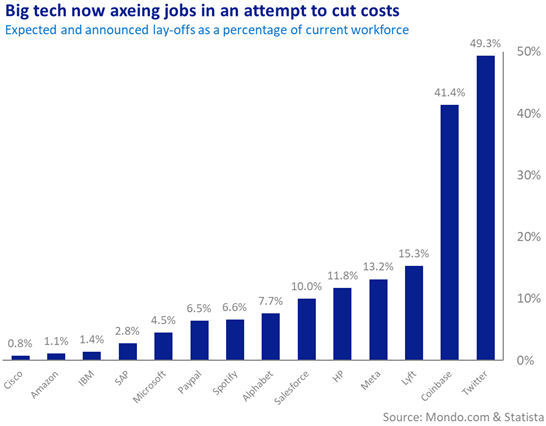

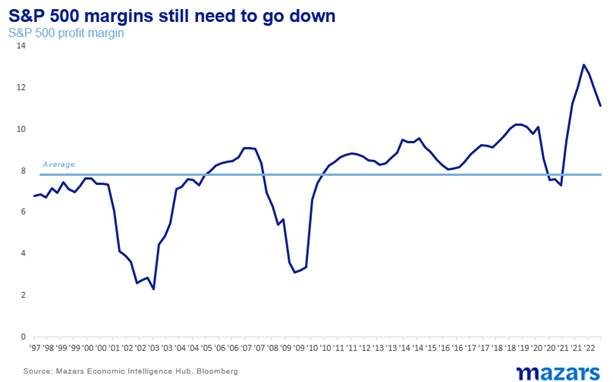

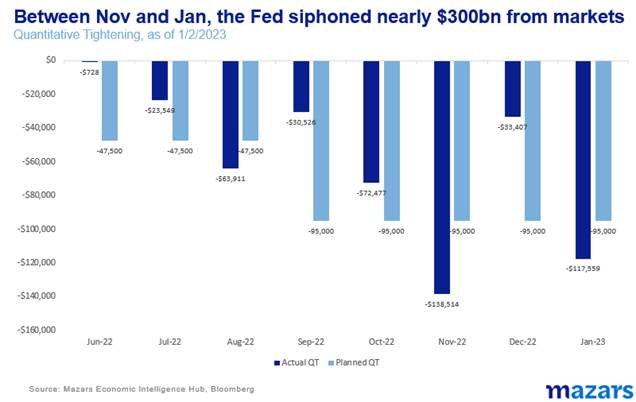

However, the economic realities of last week are in antithesis with this bull market. In the past fifteen days, the Fed raised rates into a cooling economy and warned markets that it will continue to do so in the coming months. Friday’s great US jobs data will only reinforce the central bank’s hawkishness. The Fed was followed by equally hawkish central banks in Europe and the UK. Meanwhile, US bank and Megatech earnings disappointed. Despite the IMF’s somewhat brighter outlook, top S&P 500 companies are firing workers, fearing an earnings recession. Earnings analysts warn that present valuations are low, and earnings could fall in the coming quarter as they don’t encompass the type of significant deterioration (10%-18%) we would see in a recession. At the same time, Asia is rocked by what could possibly prove to be one the biggest corporate scandals in history. And let us not forget that the Fed continues to siphon money from markets at an increased pace.

Why the dichotomy? One reason could be just plain old optimism, coupled with algorithmic trading.

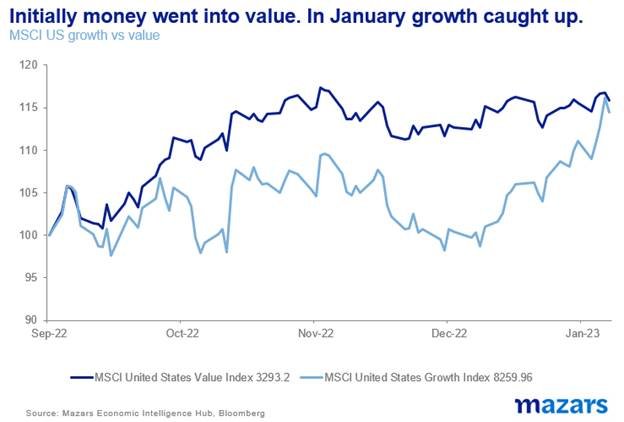

The other reason could be a little more surprising. Money managers are always telling investors to invest more when valuations are low. What if this is what is happening? After all, we are not seeing another tech-driven rally, but rather an overall buoyant market affecting value as well as growth.

We feel that the answer is probably a mix of those conditions. What’s more important is that in this market we expect bull-runs and pullbacks more often than in the past.

Barring a serious financial accident in the next twelve months, the single-course low-volatility market may be consigned to the past. We have moved from a uniform and unipolar market to a multipolar one and one thing is beginning to become clear: The future is not about beta (passive investing) anymore, but Alpha, finding the best managers and the best points of view in what is now a polyphonic market.

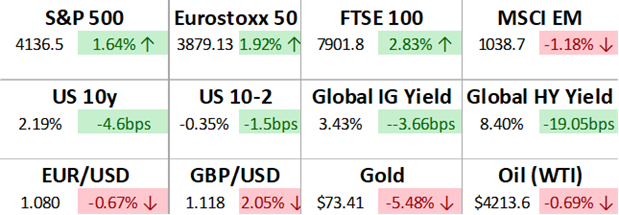

The S&P 500, the world’s leading equity indicator continued to rally, closing the week just 12% below its record levels levels, making up for more than half of the losses incurred last year. The US 10y yield, meanwhile, remains anchored around 3.5%, significantly below its cycle high of 4.2%. Corporate spreads are subsiding as investors are willing to take on more risk. Meanwhile, the FTSE 100 hit an all-time high last week.

The statement above is difficult to reconcile with the realities of the last two weeks. In the past fifteen days, the Fed raised rates into a cooling economy and warned markets that it will continue to do so in the coming months. Friday’s great US jobs data will only reinforce the central bank’s hawkishness. The Fed was followed by equally hawkish central banks in Europe and the UK. Meanwhile, US bank and Megatech earnings disappointed. Despite the IMF’s somewhat brighter outlook, top S&P 500 companies are firing workers, fearing an earnings recession.

Earnings analysts warn that present valuations are low, and earnings could fall in the coming quarter as they don’t encompass the type of significant deterioration (10%-18%) we would see in a recession.

At the same time, Asia is rocked by what could possibly prove to be one the biggest corporate scandals in history. Wall Street behemoths like Blackrock and Vanguard have exposure - a reminder that passive investing has risks. And let us not forget that the Fed continues to siphon money from markets at an increased pace.

Commentators and pundits are wondering why the bullishness. If anything, a bullish environment would enable the Fed to tighten further, or at the very least to increase the pace of quantitative tightening.

One reason could be just plain old optimism, coupled with algorithmic trading. Humans are simply betting that the Fed will stop hiking at some point this year. If inflation numbers are not too affected by China (and according to heavy machine manufacturer Caterpillar they might not) then waning demand could even cause deflation (incredible as it may sound) by the end of the year. Meanwhile, robotic trading amplifies moves upwards and downward and takes into account seasonality. Traditionally January is one of the best months for markets.

The other reason could be a little more surprising. Money managers are always telling investors to invest more when valuations are low. What if this is what is happening? After all, we are not seeing another tech-driven rally, but rather an overall buoyant market affecting value as well as growth.

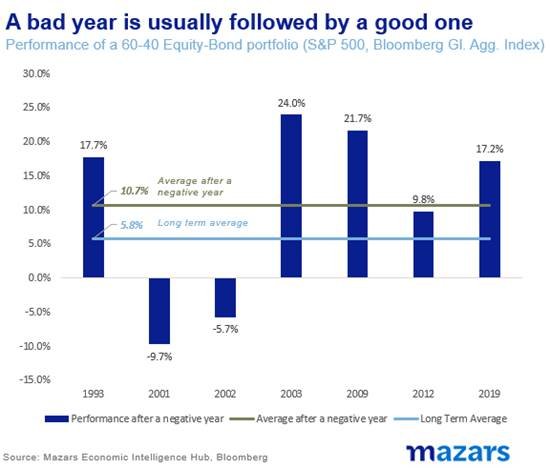

Is it that incomprehensible that Investors who have been yield-starved for years find 3% and 4% investment grade and sovereign valuations attractive? Or that, considering past returns, investors are coming back after a bad year?

We feel that the answer is probably a mix of those conditions. Some bullishness, some algos, some buying the valuation, the yield and the history, each of these trends reinforcing the other.

Of course, volatility and surprises are still with us. So investors should expect pullbacks. But this is a healthy market, going from gloom to boom and vice versa. What’s healthy about it? That optimism is not policy-dictated. Those who decide to invest today should know that this market will have a lot of debate and analysis and a lot of opposing views. They should still be ready for many more twists and turns than they were used to in the past few years. Today’s 4200 S&P 500 can quickly go down to 3500 and back up again.

Barring a serious financial accident in the next twelve months, the single-course low-volatility market may be consigned to the past. We have moved from a uniform and unipolar market to a multipolar one and one thing is beginning to become clear: The future is not about beta (passive investing) anymore, but Alpha, finding the best managers and the best points of view in what is now a polyphonic market.

What to look for this week:

European countries and UK industrial production December (throughout week)

Various Fed speakers (throughout week)

Earnings continue (throughout week)

UK Q4 GDP (10th Feb)

Chinese liquidity data and PPI (10th Feb)