By Ulf Bergman

Macro/Geopolitics

Last week saw the European Central Bank following the US Federal Reserve’s example with a sizeable interest rate hike to combat the continent’s rising prices. Some of the bank’s policymakers also suggested that similar increases could follow in the coming months. The growing prospect of more large-scale interest hikes around the world has continued to weigh on investors’ expectations for global economic growth last week, with commodity prices suffering as a result. A recession is looking increasingly likely, especially as significant demand destruction is widely seen as one of the few cures for the current high inflation rates.

In contrast, Chinese inflation data released on Friday provided a glimmer of hope. Both consumer and producer prices rose by less than expected in August, which will provide the country’s central bank with more room for manoeuvre as it looks to support the economy’s flagging growth rates. There have already been calls for additional monetary easing, which, if implemented, could provide some support for the Chinese demand for commodities.

Commodity Markets

Crude oil prices lived through yet another volatile week, with the opposing effects of a weaker demand outlook and continued tight global supplies taking turns to dominate sentiments. Brent crude oil futures had fallen as low as 88 dollars per barrel by mid-week as increasing Covid-restrictions in China weighed on the projections for global demand. However, reduced expectations of a deal over the Iranian nuclear programme and efforts to impose a price cap on Russian oil exports saw prices recovering most of the losses as supply concerns moved back to the top of the agenda. The Brent contracts ended the week at 92.84 dollars per barrel, only marginally below the previous week.

Following a sharp increase last Monday, European natural gas prices trended lower during the rest of the week. Despite continued disruptions to the continent’s supplies through the pipelines from the east, the front-month contracts registered a 3.5 per cent decline for the week. Concerns over the demand outlook amid the risk of a recession and efforts by the European Union to insulate the continent from the worst effects of the rising gas prices contributed to the decline. The contracts for delivery next month settled at 207 euros per megawatt-hour on Friday.

The mounting concerns for the European growth rates amid rising interest rates, combined with falling natural gas prices, saw European thermal coal prices ending last week at the lowest levels since early August. The contracts for delivery next month in North-West Europe registered a weekly loss of more than thirteen per cent, despite robust gains at the beginning of the week, and ended the week at 320 dollars per tonne. In contrast, the benchmark futures for the Asian coal trade fared somewhat better, with the Newcastle contracts for delivery in October ending the week at 431 dollars per tonne following a 2.3 per cent decline.

The prospect of an accelerated rollout of the Chinese economic stimulus programmes amid weakening economic growth rates supported iron ore prices last week. As a result, the October contracts trading at the Singapore Exchange reversed recent losses. The futures gained nine per cent last week, despite daily losses during the middle of the week, and settled just shy of 103 dollars per tonne on Friday.

Most base metals advanced last week as rising energy prices have put pressure on global supplies. Copper futures trading at the London Metal Exchange increased by 2.9 per cent, while zinc edged up by one per cent. Nickel proved to be last week’s star performer, with the contracts soaring by twelve per cent amid falling supplies. The aluminium contracts went against the flow with a weekly decline of 0.4 per cent.

The agricultural commodities faced a mixed and volatile week. Following criticism of the current deal that has allowed Ukraine to resume its seaborne grains exports by the Russian leader, the wheat futures trading in Chicago gained 7.6 per cent last week. The comments, later echoed by the Turkish president, have raised concerns of disruptions to the flow of wheat from the Ukrainian ports. The corn contracts advanced by more than three per cent last week amid continued concerns over global supplies. In contrast, the darkening outlook for the global economy weighed on soybean prices, with the contracts declining by 1.4 per cent during last week.

Freight Markets

Most of last week’s drama in the markets for seaborne freight was provided by the Panamaxes in the dry bulk space. The Baltic’s sub-index for the tonnage segment gained nearly 47 per cent during last week as order volumes rebounded, especially for seaborne coal. In contrast, the recovery for the Capesizes lost steam and the indicator for the freight rates for the largest vessels retreated by 8.3 per cent. The smaller vessel segments provided more modest weekly performances, with the gauge for Supramaxes shedding 2.6 per cent and the Handysizes edging up by half a per cent. The robust performance for the Panaqmaxes contributed to the headline Baltic Dry Index advancing by 11.7 per cent.

Among the Baltic tanker indices, the indicators for the gas carriers provided last week’s stand-out performances. The gauge for the LNG tankers advanced by 13.1 per cent, while the index for the LPG carriers gained 9.2 per cent. The darkening outlook for the Chinese oil demand following the increase in Covid-restrictions, combined with falling prospects of a resumption of Iranian crude oil exports, weighed on the Baltic’s dirty tanker index last week, with the indicator retreating by 3.8 per cent. In contrast, the gauge for the clean tankers advanced by 3.4 per cent following recent weakness.

The View from the Shipfix Desk

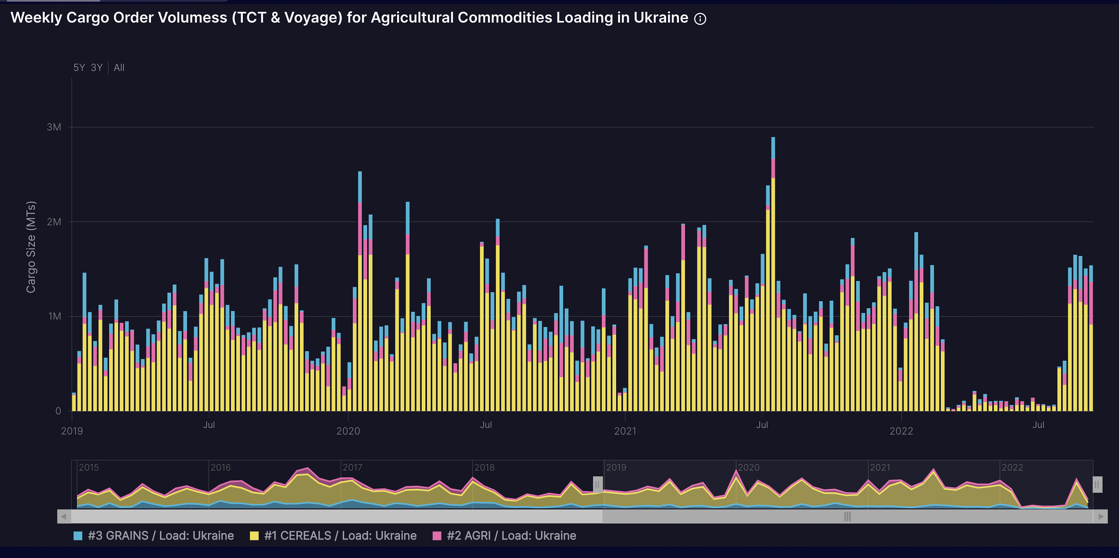

Wheat prices rose to the highest levels since early July last week following the Russian President’s criticism of the deal that has allowed Ukraine to recommence its seaborne exports of agricultural commodities. The prospect of a renegotiation of the agreement or renewed disruptions to the flow of grains through the corridor in the Black Sea sent wheat futures trading in Chicago nearly eight per cent higher last week. The sharp rise for the futures contracts highlights the tightness of the global supply situation, suggesting that any future disruptions could push prices sharply higher.

Despite the rising risk of disruptions, the cargo order volumes for agricultural commodities loading in Ukrainian ports have remained stable in recent weeks, following the rebound that began in late July. However, the average cargo size remains low, suggesting that it will take considerable time to shift Ukraine’s substantial inventories, potentially putting the flow at risk from future disruptions.