By Daniel Hynes

A lower-than-expected inflation print saw a risk-on tone across markets push commodity markets higher. This was supported by signs of improving demand for some commodities.

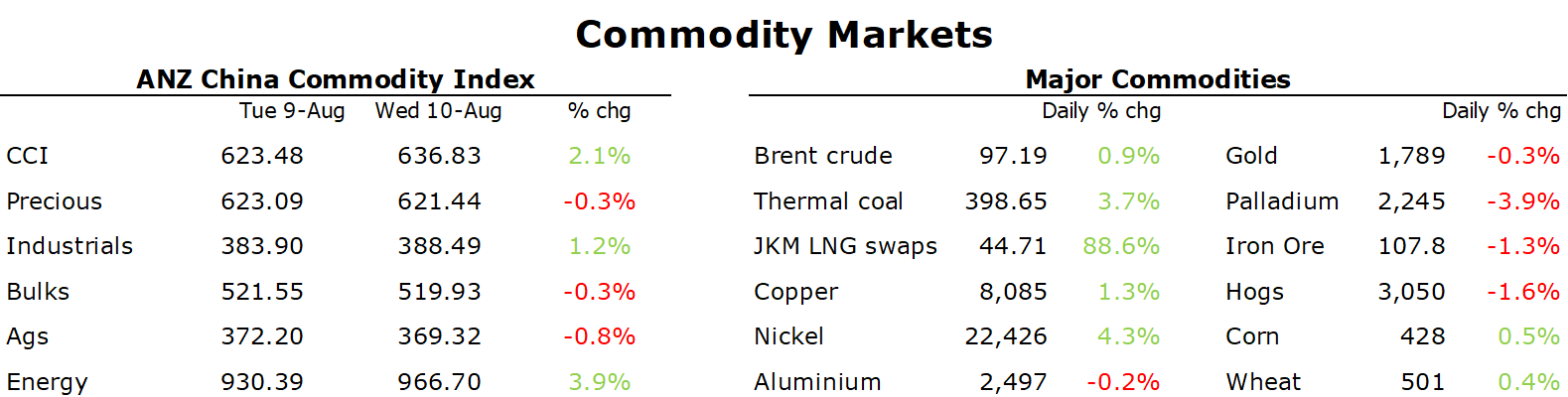

Crude oil gained amidst a risk-on tone across markets as signs of cooling inflation and a weaker USD boosted sentiment. The slower-than-expected pace of inflation cooled investor expectations of future rate hikes and eased concerns of weaker economic growth. This was supported by signs of better demand. Energy Information Administration data showed that US gasoline demand improved after inventories sank. US gasoline inventories fell 4,978kbbl last week, which helped push gasoline supplied (a proxy for demand) up 582kb/d to 9.12mb/d. This was slightly tempered by a strong gain in US crude oil inventories, which rose 5,457kbbl last week. Much of that gain was driven by a rise in domestic output, which hit a near two-year high of 12/2mb/d. Global supply concerns also eased, with Russia’s pipeline operator Transneft resuming flows on the Druzhba pipeline toward Ukraine.

European natural gas rallied as falling water levels on the key Rhine River threatens to disrupt energy shipments. Dutch front month futures rose 6.9% to EUR 205.47/MWh as a drought amid extreme temperatures has left the river almost impassable. It’s forecast to drop below the critical depth of 40cm on 12 August. At that level, barges hauling everything from diesel to coal are unable to transit the river. Europe has been grappling with the threat of energy crises this winter, as Russia gas flows are curtailed. It’s expected to rely heavily on coal in particular to mitigate the expected fall in gas. The grim outlook saw coal futures surge, with the European benchmark up 11.7% to USD335/t. This lifted other coal benchmarks, including Asia coal. Amid these concerns about energy supply disruptions, the build-up in European gas inventories is running about nine weeks ahead of last year. This is helping check the price increases.

North Asian LNG followed European gas markets higher, although the gains were much more limited following strong gains in recent weeks. Nevertheless, interest in spot LNG remains high. Thailand entered the market amid low supplies and a pipeline connected to a Myanmar gas field was shut due to a leak. It’s also expecting to keep buying as easing COVID-19 restrictions boost demand. Workers on Shell’s Prelude floating LNG terminal extended industrial action by a week, adding to tightness in the Asian market. This follows from data last week showing exports from Australia’s east coast LNG projects were down 7% y/y in July to 1.64mt.

Gold initially climbed after the US CPI came in lower than expected. The subsequent weaker USD and lower yields on Treasuries helped push gold to its highest level in a month. However, the precious metal gave up much of these gains after Fed governors warned that it doesn’t change the US central bank’s path toward higher rates this year and next.

Sentiment was more buoyant in the base metals sector, with copper extending a rally since mid-July as expectations of stronger demand rose following the inflation data. The rest of the sector was dragged higher, aided by concerns of supply disruption emanating from Europe’s energy crisis. Rising energy costs are threatening to curtail even more output in Europe as electricity prices surge higher.

Data source: Commodities Wrap