By Mark Nugent

The Big Picture: Global growth slowing

GDP revisions

As fresh economic data headlines continue to drag on sentiment for the global economy, we look at how this is likely to shape bulk commodity demand going forward.

Global economic growth concerns

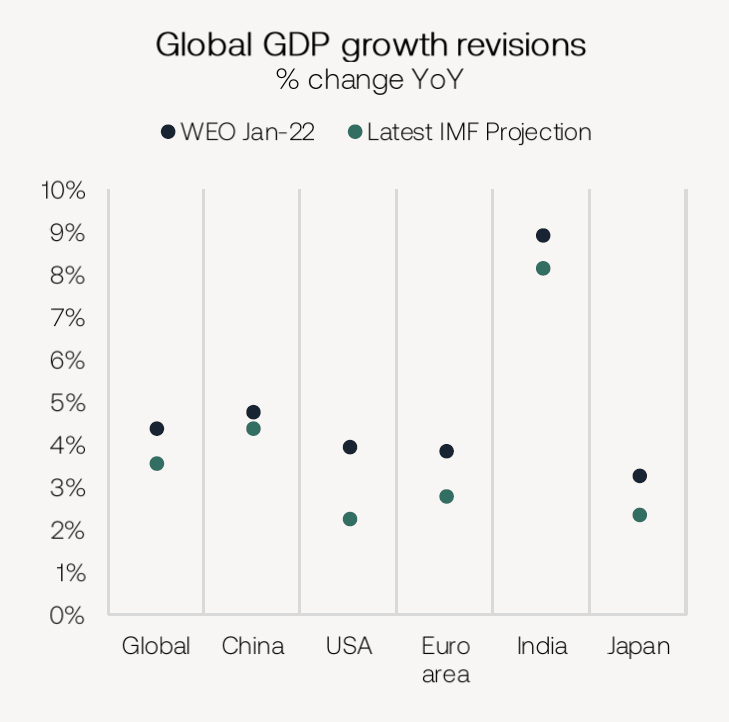

Economic sentiment in the past few months has started to trend downwards following the Russia-Ukraine war, with several concerning GDP readings for Q1 already released. The IMF currently forecasts global GDP to grow by 3.8% in 2022, revised down from 4.4% in January, according to its latest World Economic Outlook (WEO). As we know, global trade is stronger when economies are performing well, so naturally, a worsening economic outlook is worrying for bulk carrier demand. The IMF lowered its US GDP forecast for 2022 to 2.3% this week from 2.9% in late-June, which was already revised down from 3.7% marked in April’s WEO. A worsening US GDP growth outlook not only has negative implications for the US, but to any countries that are leveraged in US dollars.

We may already be in the midst of a global slowdown in trade with total dry bulk commodity imports in June declining by 7.4% YoY to 389m tonnes. The closure of Ukrainian ports, of course, has been a factor in this.

China: a tale of two halves?

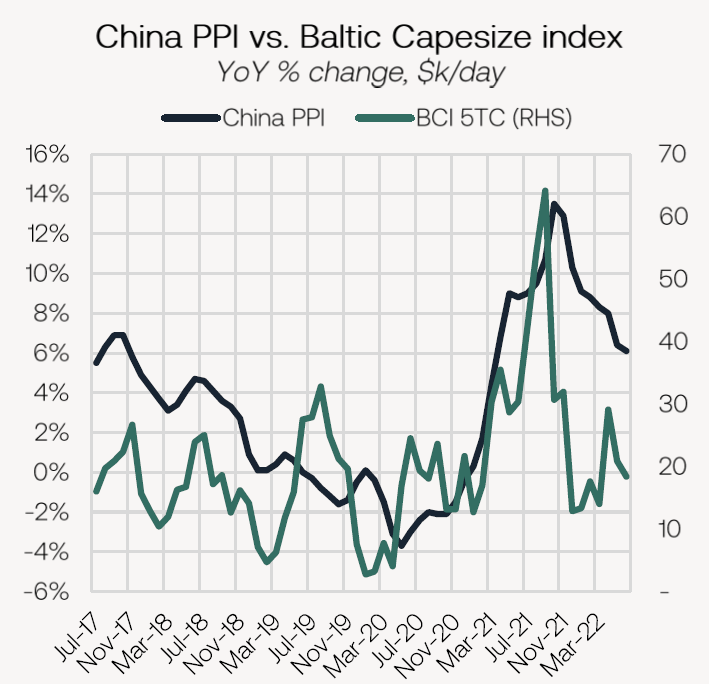

In the first half of the year, China’s seaborne bulk commodity imports declined by 8.3% YoY to 941.7m tonnes, with June amounting to just 146.4m tonnes, the lowest level since February 2020. Demand weakness across most facets of the Chinese economy has driven producer prices lower. These have consistently declined since reaching the metric’s highest level on record, in tandem with the BCI’s most recent high, in October 2021. Purchasing price indexes indicate the growth in ex-factory prices of industrial products, such as steel. Logically, when this metric declines, so does the incentive to boost output. With the weakness in the country’s property sector and stop-start economy, it is unsurprising that this is trending lower. For context, the last time this metric hit growth levels near these highs was August 2008, measuring 10.1%.

Contrary to countries in the West, Chinese CPI has been moderate, measuring at 2.5% YoY in June, compared to a 9.1% reading in the US released this week. The lower CPI reading can be accredited to weaker demand but also easing supply-side constraints, given domestic production across several commodities has increased. This is important when considering the Chinese government is aiming to stimulate the economy, with other economies forced to tighten to combat inflation.

To limit any further downside, the Chinese government has been actively taking steps to improve industrial activity. This has come in large bond issuances for infrastructure projects, which of course are highly bulk commodity-intensive. The People’s Bank of China (PBoC) also reduced the reserve requirements for major banks to encourage lending. This has seemingly started to emerge with 2.8 trillion yuan worth of loans extended in June. Tomorrow morning, China is set to release a range of economic data, none more important than Q2 GDP growth. While Q2 will largely reflect the impact of the lockdowns, we are still confident activity will improve in 2H 2022, replicated by a rise in the country’s dry bulk commodity demand.

Exchange rates

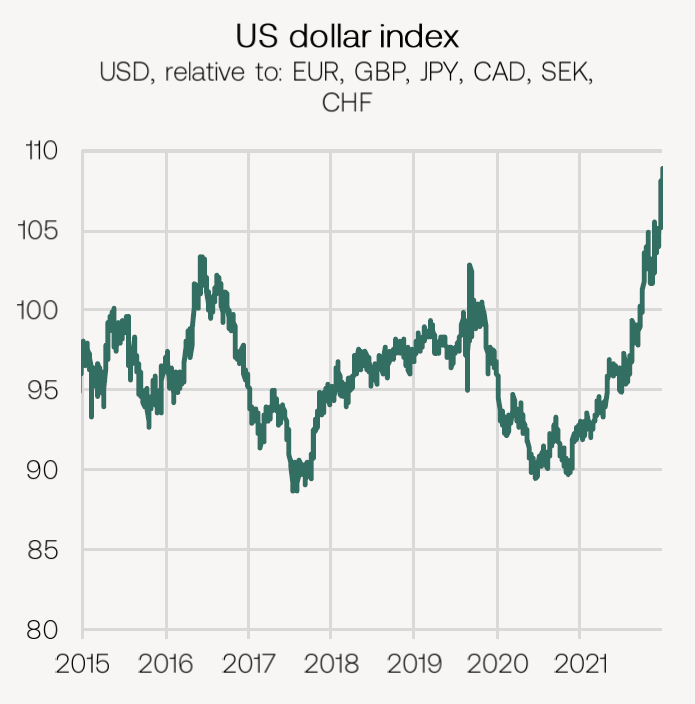

The US dollar index, weighted against six major foreign currencies, this week reached 20-year highs at $108.8. The strength in USD drove the Euro-Dollar to 1-for-1 parity, which could be important as the US and EU looks to strengthen trade relations amid the Russia-Ukraine war. Amongst the two regions, this makes European-produced products more attractive to US buyers and vice versa. With dry bulk commodity flows between the regions largely heading from the US to Europe, this is unfavourable for bulk carrier demand in this region. For instance, some steel products are said to be offered at similar levels domestically and abroad in Europe, but unloading and inland transport costs are making importing US products less desirable. Overall, while the bloc is a net-importer of dry bulk commodities, a weakening Euro makes the seaborne market less-attractive. For coal imports, we still see this trade increasing regardless, with the effect potentially making an impact on other trades such as steel, and grains.

Further, with the US dollar continuing to get stronger, countries may look to purchase commodities in other currencies as their purchasing power in USD has declined. Most recently, there have been reports of a yuan-based iron ore purchase out of Australia to China. If the US dollar continues to increase we will likely see this trend continuing.

Monetary tightening

In countries such as the US, Canada and South Korea, along with the EU, central banks are opting for substantial interest rate hikes in an attempt to control inflation. By doing this, the aim is to reduce demand by increasing the cost of borrowing thereby reducing the supply-demand gap. This is largely an issue in the West where interest rates had plunged towards 0%. By reducing economic activity, we could see this weaken dry bulk demand in these countries. On the other hand, in China, where the economy has struggled as of late, baseline interest rates lie at 2.9%. Based on this, the PBoC still has room to cut rates in an attempt to stimulate the economy, particularly as it is not constrained by high inflation. With dry bulk demand heavily weighted towards China, the fact the government still has tools to provide additional stimulus is encouraging if the economy continues on its current path of credit growth.