The freight market keeps the downward correction of rates from the last week, whereas the growth of demand ton-days appears significantly high for the Panamax segment. We see a wave of uncertainty for demand in the iron ore market as the resurgence of COVID-19 cases in China has dampened the sentiment. Prices for iron ore cargoes with a 63.5% iron ore content for delivery into Tianjin have bottomed now around $145/t, and the seven-month high of $159/t hit earlier this month is far from the market.

In the coal segment, there is also a drop in prices stemming from an easing sentiment in Chinese demand. Newcastle coal futures have seen levels below $300/t, however, prices are still doubled since the beginning of 2022, fueled by energy supply constraints from the Russia-Ukraine conflicts, floods in Australia, and a partial ban of exports from Indonesia. Coal prices are expected to remain elevated for the rest of the financial year, as the global economy is experiencing severe supply disruptions following the conflict given that Russia is the key supplier of coal in the seaborne market.

In the grain market, the situation of exports is worsening day by day and Ukraine’s new agriculture minister confirmed that would only improve if the tensions with Russia end. The minister confirmed that Ukraine’s grain shipments have dropped from 4-5mil tons per month to a few hundred thousand. In the meantime, the U.N. warned that the significant reduction in Ukraine’s grain exports could increase international food and feed prices by 8% to 22% above the current levels, which were already elevated.

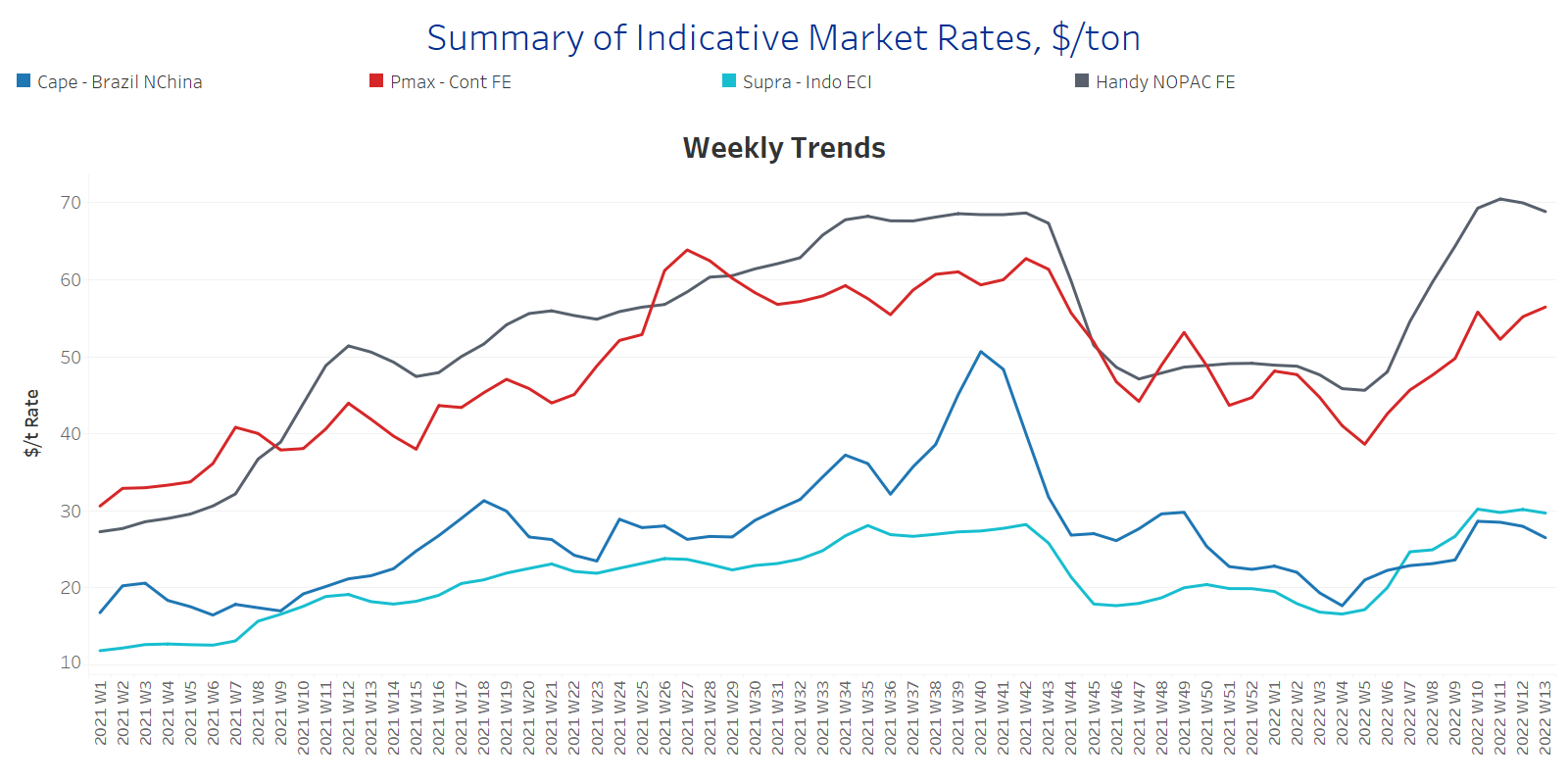

SECTION 1 - FREIGHT - Market Rates ($/t) - Weaker

‘The Big Picture’ - Capesize and Panamax Bulkers and Smaller Ship Sizes

A weaker sentiment of freight rates is mainly reflected in the Capesize and Handysize segment for this week, while freight rates still sustain a high level in the Supramax and Panamax segments.

Capesize Brazil-to-North China freight rates dropped to less than $27/t, down by almost $2/t from last week, while the last peak remains to be at Week 50, 2021 at levels of around $50/t.

Panamax Continent-to-Far East freight rates increased to $57/t, up by $5/t from the previous week, with the current trend indicating that freight rates could remain strong in the next few days.

Supramax Indo-to-ECI freight rates remain robust at $30/t and continue stronger than the level of freight rates in the Capesize segment.

Handysize NOPAC-to-Far East freight rates have shown an accelerated decline over the last three weeks and plateaued around $69/t. However, the NOPAC-to-Far East freight rates are still exceeding the Panamax Cont-to-Far East rates with a persistent surprising increase over the last nine weeks.

SECTION 2 - SUPPLY - Ballasters View

Number of Vessels - Decreasing

Supply Trend Lines for Key Load Areas

The overall trend of ballasters continues to decrease in the bigger vessel sizes, whereas it has not yet shown any indications of downward movement for the smaller Handysize ships.

Capesize SE Africa: The number of vessels sailing in ballast dropped slightly further this week and found a steady sentiment at around 69 vessels, which is almost 10 vessels less than the one-year average. It seems that the current levels have severely plateaued and there is a question of whether there will be a further downward correction in the upcoming days.

Panamax SE Africa: The number of vessels sailing in ballast remains at significantly lower levels over the last five weeks, while the decline for the last week is not sharp with levels around 70 vessels. The current figure is 30 vessels less than the one-year average; however, it seems that the acceleration of decline is almost over, for now, the same as in the Capesize segment.

Supramax SE Asia: The number of vessels sailing in ballast continues the downward trajectory of the last week, with a decrease to 74 vessels, when the last peak was during Week 10, 92 vessels.

Handysize NOPAC: The number of vessels sailing in ballast soared over the week and is now around 74 vessels, which is almost 10 vessels more than the one-year average and 16 vessels more than the levels of the previous week.

As long as vessel availability remains low in the Capesize and Panamax segment, we could still see robust freight rates in the next few days compared to the first weeks of the year. The challenge seems to be the evolution of ballasters in the Handysize segment and the future impact on freight rates along with the geopolitical tensions.

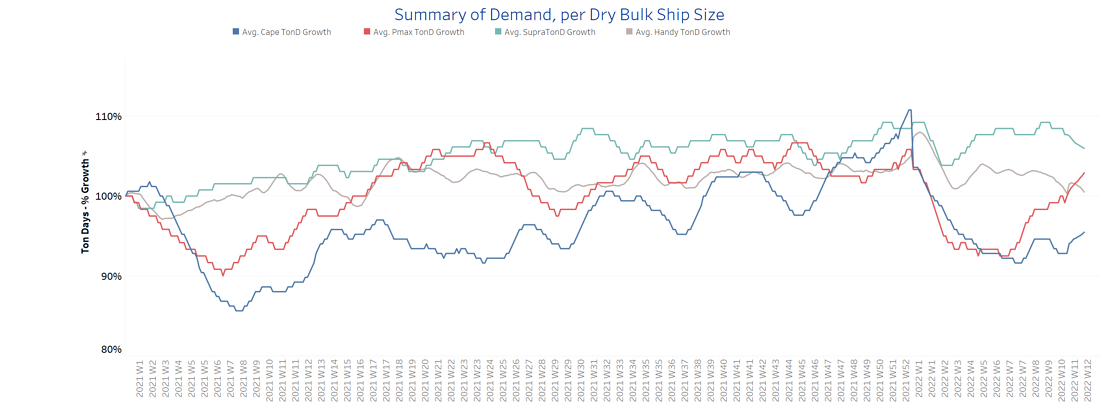

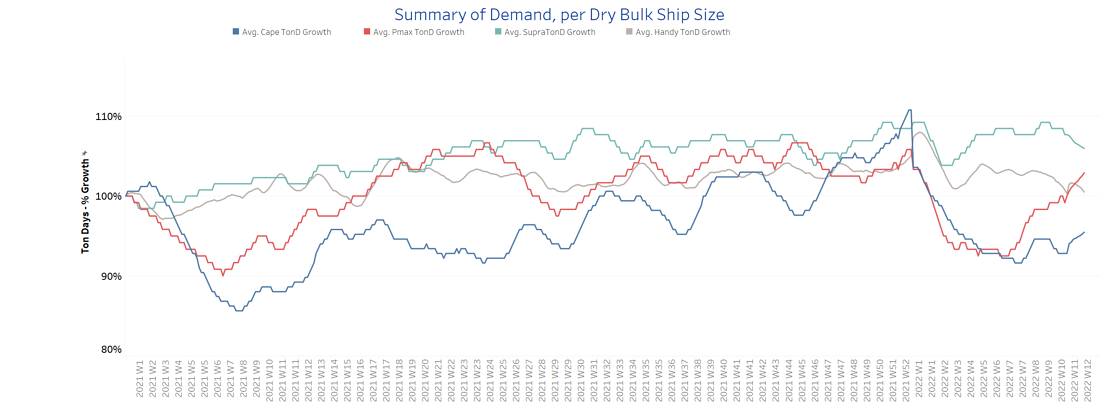

SECTION 3 - DEMAND - In Ton Days

Decreasing

The overall trend of demand ton-days is increasing for the Panamax segment, whereas it is softening for the smaller vessel sizes.

Capesize demand ton-days: The sentiment is softer compared to the demand evolution during Weeks 8 and 9. However, we could see signs of stronger growth in the next few days stemming also from Beijing's robust growth target to more stimulus measures ahead.

Panamax demand ton-days: Dramatic growth in Panamax tonne-mile demand has taken place over the last five weeks and the trend seems unstoppable as March is near ending. The Panamax demand ton-days have started to near the percentage level of increase of the Supramax.

Supramax demand ton-days: We see indications of slower growth; however, demand ton-days are still showing stronger growth compared to the other vessel sizes.

Handysize demand ton-days: The trend continues dropping and it has now started to indicate a slower magnitude of growth than the Panamax evolution.

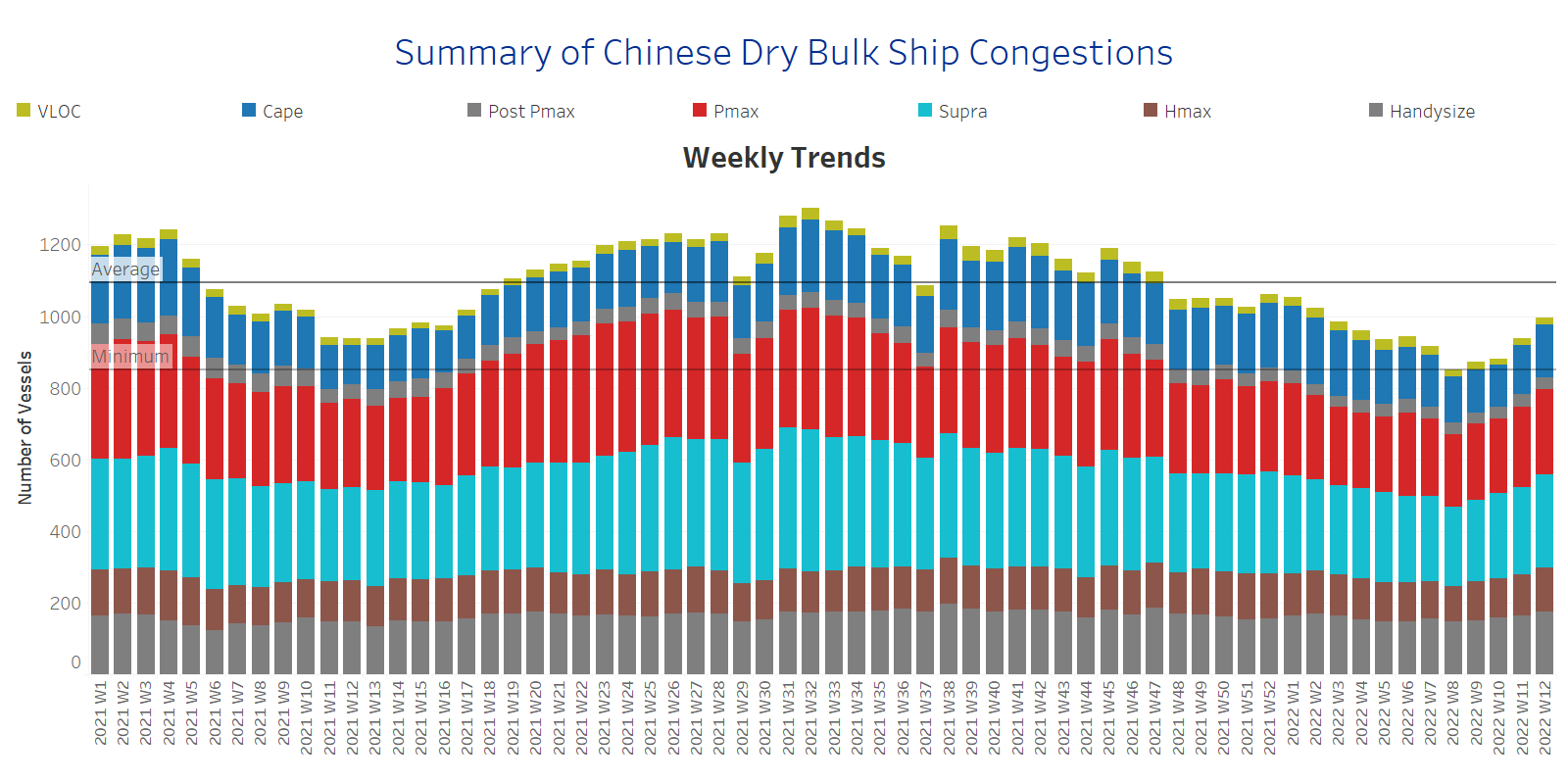

SECTION 4 - CHINESE PORT CONGESTIONS -

Number of Vessels - Increasing

Dry bulk ships congested around Chinese ports

Dry bulk ships in congestion have shown a sharp increase over the last two weeks and the number is nearing the one-year average of 1090 vessels.

Capesize: The number of ships in congestion has now surpassed 140 vessels, compared to the low of 119 in Week 10.

Panamax: There is a sharp increase to 275 ships in congestion, which is almost 35 vessels more than in the previous week.

Supramax: The upward trend has the same sharp increase as the Panamax. The number has now fetched 286, 30 vessels more than last week.

Handysize: The number of ships in congestion has kept the increased levels of the previous week and we see now 169 ships, which is a slight increase of 4 vessels from last week.