By Ulf Bergman

The war in Ukraine is less than a week old. The humanitarian costs are rapidly escalating, as casualties are mounting and many residents are forced to flee their homes for safety elsewhere. Beyond the immediate effects on the ground in the country, the ramifications are rapidly spreading across the globe as more and more economic sanctions are imposed on commercial entities and the flow of goods and commodities originating in Russia. In addition to formal sanctions, companies face increasing political and popular pressure to sever their ties with Russia.

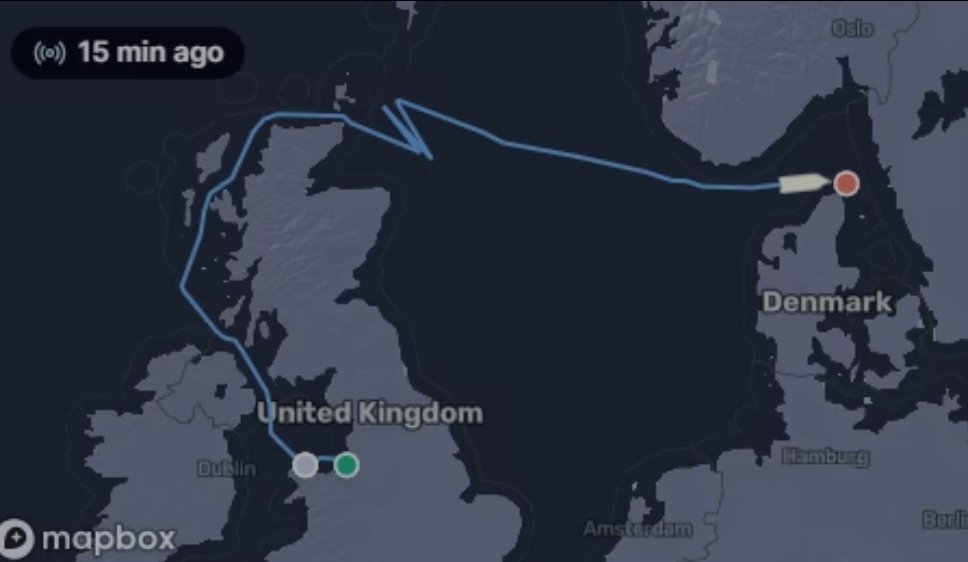

As a result of the far-reaching economic sanctions, the shipping and commodity market face disruptions in many different ways. Apart from the apparent impact on many Russian exports, the sanctions also target vessels owned or controlled by many Russian companies. There are increasing reports of such vessels being either refused to enter ports or facing detention. Over the weekend, French authorities apprehended a Russian RoRo vessel linked to a sanctioned entity in the English Channel. It remains moored in the northern French port of Boulogne-sur-Mer. In another highly publicised development, authorities on UK’s Orkney Islands have sought to block the docking of Liberia flagged crude oil tanker owned by Sovcomflot amid local protests. The 110,000 DWT vessel has since cancelled the port call and set course for Denmark and Skagen after sailing in a holding pattern off the islands.

However, it is unlikely that it is the ultimate destination and only serves as a staging post. The Danish port is primarily a fishing port without the facilities to serve crude tankers, and the Russian waters in the Baltic Sea should be a more attractive option for the owner. Following the incident, the British Transport Secretary recommends that UK ports refuse entry to all Russian vessels, and the European Union is rumoured to prepare similar measures.

NS Champion - Past Track and Predicted Course

Source: Shipfix

The ongoing war and the resulting sanctions have seen the commodity markets moving higher, amid fears over supply disruptions. In addition, the, at times, contradictory news flow has contributed to increasing levels of volatility across the global markets. Energy commodities and wheat have registered particularly large gains in the last week, with European gas prices leading the way with over eighty per cent. While Russian energy sources are not targeted directly by the new sanctions, with some Russian banks having been allowed to remain in the SWIFT network to facilitate payments, there are fears that exports could be disrupted or weaponised as a countermeasure to the sanctions. The exodus of Western energy companies from Russia and increasing difficulties to raise trade finance for Russian commodity exports, with many Singaporean and Chinese banks joining their Western peers, are adding to the perceived headwinds for the crude oil supply.

In the face of the threat of declining flows of natural gas from Russia, European governments are increasingly turning to an old friend. Even before the conflict began in earnest, unreliable supplies from Russia, in combination with low gas inventories and cold weather, the continent’s thermal coal imports have been on the rise after years of decline.

However, in light of the Russian leader’s increasingly aggressive rhetoric towards Europe, the most polluting among fossil fuels is having a revival. News that Germany will create a reserve of coal for its power plants and that Italy could reopen some of its shuttered coal plants have contributed to coal gaining more than a quarter during the last week and reaching a new all-time high of 301 USD per tonne.

When the Russian military forces rolled into their neighbouring country, around fifteen per cent of the global wheat production became affected by the war. In the short term, both Russian and Ukrainian supplies are likely to remain unavailable for the international markets. Even if hostilities were to cease relatively soon, Russian wheat exports are likely to continue to face sanctions. If there is a Ukrainian wheat harvest later this year, it can be expected to be decimated by the war.

Hence, there is no suggestion of wheat prices giving up any of the recent gains. One of the more prominent importers of seaborne wheat, Egypt, has also signalled it is looking beyond its traditional sources, Russia and Ukraine, for its supplies this year. The move will increase the tonne-mile demand, as the buyers will need to find alternative sources at more distant shores.

The war in Ukraine will see increasing competition for shrinking supplies of many commodities, with prices likely to continue to gain. Emergency measures, such as the release of strategic reserves, can potentially alleviate some of the pain. However, the effects of such initiatives are likely to be transient, and only demand destruction is likely to slow or reverse many rising commodity prices. A loss of Russian oil supplies could be offset by Saudi Arabia increasing its output and sanctions on Iranian oil being lifted. Still, at this stage, there are no signs of either happening.

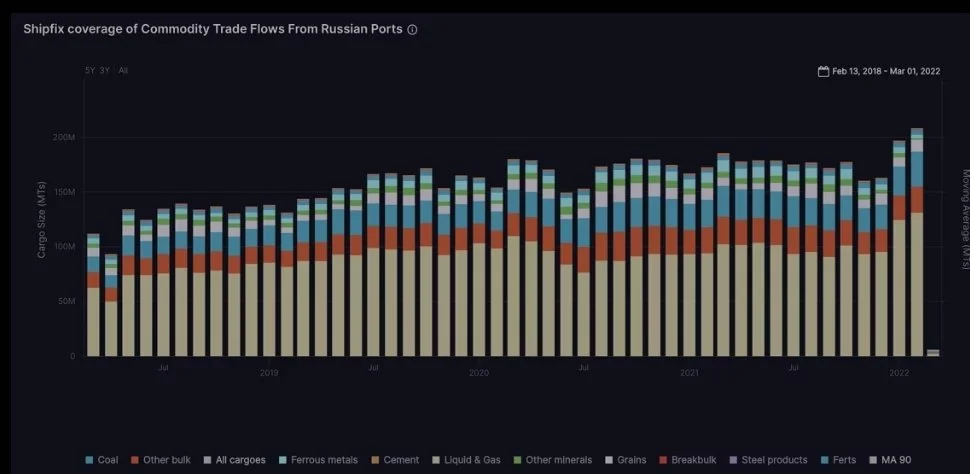

With the latest round of new sanctions on the Russian economy being only a few days old, the effects on global trade flows are yet to emerge. If anything, shipments from Russian ports have been robust during February, according to Shipfix’s trade flow data. Both dry and wet cargoes saw increasing volumes during last month, suggesting many exporters expected sanctions to be imposed. The fact that the new sanctions more or less coincided with the month-end also means that any meaningful month-on-month or year-on-year comparisons will have to wait until the latter parts of the current month.

Source: Shipfix

Somewhat lost in the recent news flow, the Chinese National Bureau of Statistics’ Manufacturing PMI was marginally stronger than expected. At 50.2, it was higher than the 49.9 consensus expectation and above the reading of 50.1 in January. The latest figure marked a fourth straight month of growth in factory activity, despite the seasonality impact of the Chinese New Year holidays and a slowdown in production during the Winter Olympics.

Hence, there are some signs that the Chinese economy is recovering following the soft patch in the second half of last year. The surge in commodity prices and the risk that the war in Ukraine derails global economic growth and demand for Chinese goods could nevertheless ruin the continued recovery.

Data Source: Shipfix