By Ulf Bergman

The number of destinations available for Russian exports is rapidly being decimated. An increasing number of formal economic sanctions combined with more informal corporate decisions to cease trading with Russia has made any trade with the country perhaps not impossible but increasingly challenging.

The sale of Russian energy commodities to Western countries has become progressively more contentious, despite being excluded from the initial batch of sanctions targeting the Russian economy. The decision to allow some Russian banks to remain in the SWIFT network reflected how vital the supplies of energy commodities from Russia are for many countries, most notably Germany. However, the German government decided against allowing the completed Nord Stream 2 pipeline to become operational. In retaliation for this move and other sanctions, the Russian deputy prime minister has suggested that the fully operational Nord Stream 1 could become the target of an export ban from the Russian side. In addition, the Russian leader instructed the government on Tuesday to compile a list of commodities and countries that will be banned for exports.

While European natural gas prices have been showing some of the most spectacular price gains, at around 200 per cent in the last month, in the wake of the Russian invasion of Ukraine, the energy source is far from the only one to be trading significantly higher than a few weeks ago. The risk of disruptions to Russian gas supplies and an even tighter global supply situation has resulted in many utilities looking to substitute natural gas with thermal coal, something that has driven prices sharply higher in recent days. Futures for thermal coal from the Australian port of Newcastle has reached new all-time high several days in a row following weekly gains of around 35 per cent. The dirtiest of fossil fuels is currently trading around 400 dollars per tonne, after spending most of the last six months in the 150 to 250 dollar range.

Likewise, crude oil has been gaining around 35 per cent since the beginning of the war on concerns that Russian supplies will become inaccessible. The news of a move by the US administration to ban imports of all Russian oil sent Brent back above 130 dollars per barrel and near the all-time high of 139 dollars recorded in 2008. The American import embargo is designed to include natural gas and coal, but that is more of a political statement as such shipments have been very rare in the past.

The race to replace Russian oil, gas and coal have raised the question of where alternative supplies can be sourced. Even before the conflict, the global energy markets were already struggling with tight supplies, and the removal of a major supplier of such commodities will amplify an already complicated situation. While the European Commission has stated that Europe has enough gas supplies to make it through the remainder of the winter, it tells the bloc’s member states to replenish inventories ahead of next winter. Hence, European buyers are likely to remain active globally to secure supplies, with seaborne imports remaining robust into the warmer parts of the year. For crude oil, the political pressure on OPEC major players to increase production is likely to be immense, especially from Washington. The efforts to ease sanctions on Iranian and Venezuelan supplies are unlikely to generate an immediate flow of additional supplies, even if negotiation reach a successful conclusion.

In the last few years, thermal coal has widely been seen as an energy source in terminal decline. However, it remains an essential ingredient in the energy mix for many countries, especially in Asia, and the energy crunch that began during the second half of last year saw it regaining some of its importance in Europe. Shipfix trade flow data show that imports of seaborne coal in Europe reached the highest levels since 2018 at the end of last year, as Russian gas deliveries disappointed and the winter arrived earlier than usual. However, as many banks and investors have withdrawn from coal, there has been limited new mining capacity coming online in recent years and the supply situation looks set to worsen as many buyers scramble to replace energy imports from Russia.

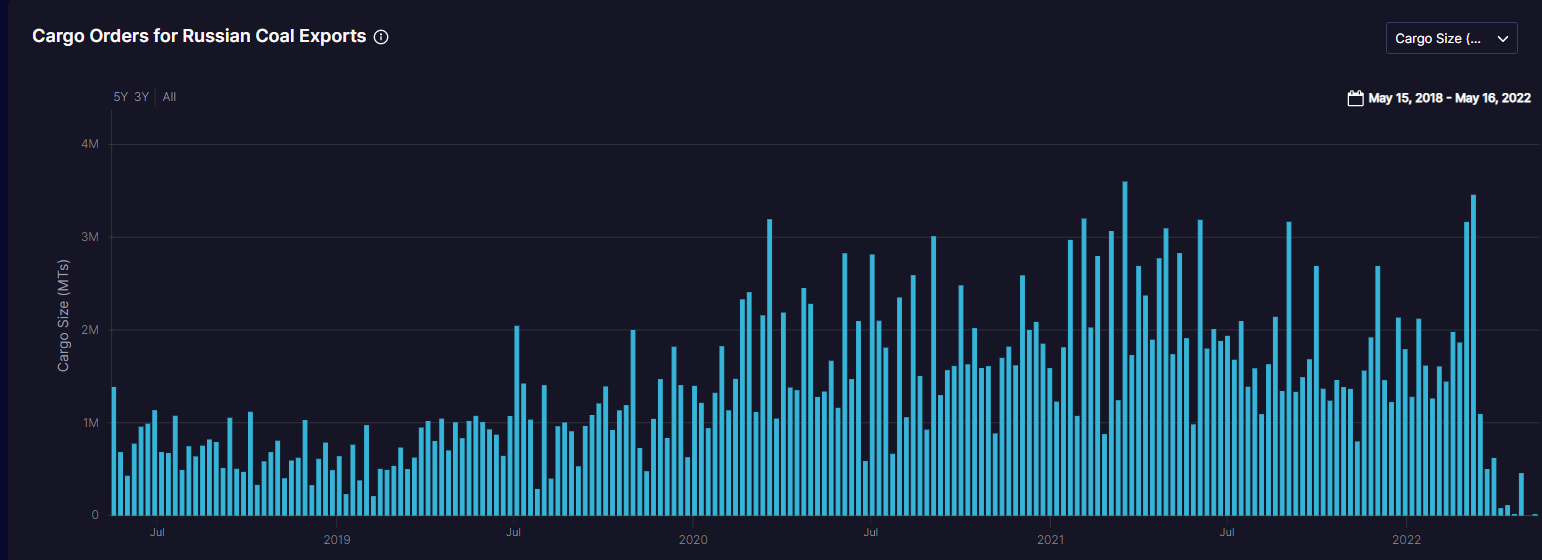

As tensions escalated in the run-up to the outbreak of the war, cargo orders for exports of Russian coal soared as sanctions became a realistic threat, and traders scrambled to ship their cargoes before it became impossible. The strength of the cargo orders has been maintained as the war has escalated, according to Shipfix data. However, as sanctions and political pressures are starting to bite, the data suggest that recent highs may not be repeated in the coming weeks.

Source: Shipfix

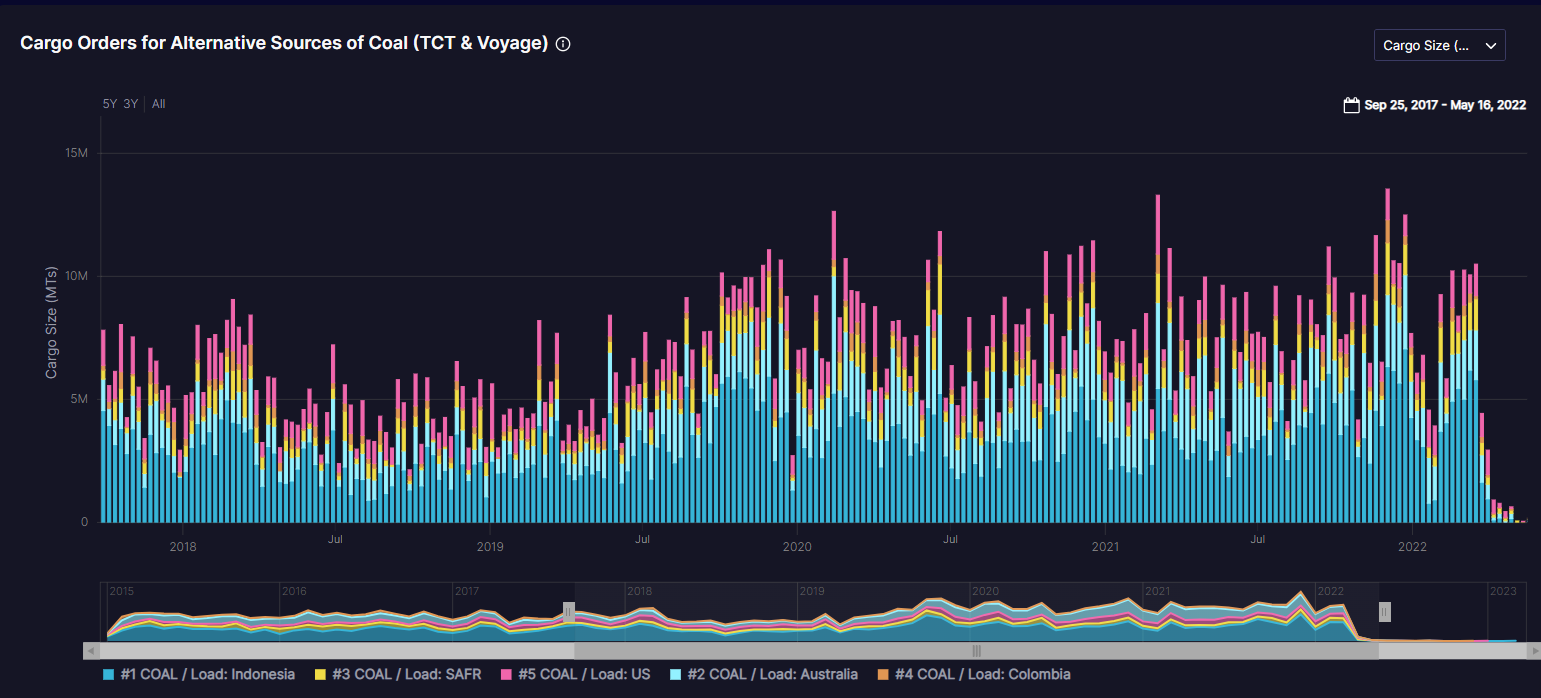

Recently, headlines have been covering coal cargoes heading to Europe from distant shores, such as Indonesia and South Africa. Cargo order data from Shipfix also confirm a recovery in volumes being shipped from these countries in recent weeks. Indonesian export volumes of coal collapsed during the first month of the year, as the government imposed an export ban to safeguard supplies for the domestic power generation. However, most of the restrictions were lifted at the beginning of February, and export orders have been on an upwards trend ever since. Ironically, the successful recovery of Indonesian export volumes could result in yet another export ban. Indonesian authorities have signalled that domestic inventory levels are not sufficient and that they are considering yet more restrictions in April or August when mining output is at its lowest.

South African coal exports have recovered after a long period of disruptions in the wake of the pandemic and social unrest. The improving volumes suggest that Europe may be able to source some of its coal from there. In addition, the Chinese ban on imports of Australian coal may provide the world with some spare export capacity.

Source: Shipfix

With the war in Ukraine less than two weeks old, it is still too early to make any firm conclusions on what new trade flows will look like in the future. However, with sanctions and countermeasures, in the form of export bans, looking increasingly likely to be in place for the foreseeable future, coal buyers are facing a more competitive world. For Europe, with supplies from its nearest provider out of bounds, the newfound appetite for thermal coal will contribute to increasing tonne-mile demand and support dry bulk freight rates.

Data Source: Shipfix