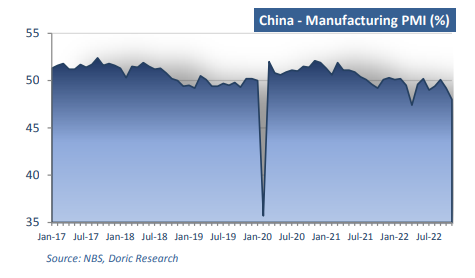

November was a rather uninspiring month for the world's second largest economy, with all main macro data indicating a softer tone across the board. In particular, the purchasing managers' index (PMI) for China's manufacturing sector came in at 48 in November, down from 49.2 in October, according to data from the National Bureau of Statistics. With a reading below 50 indicating contraction, November figure was weighed on by sporadic and scattered Covid-19 resurgences and the complex international environment, the bureau's senior statistician Zhao Qinghe said. Production activities slowed down by the epidemic outbreaks, with the sub-index for production standing at 47.8 in November, considerably lower than the previous month. In sync, demand has also declined, with the respective sub-index for new orders dropping 1.7 percentage points from October to 46.4.

Against this backdrop, China’s imports and exports shrank at their steepest pace in at least two and a half years in November, with weakening global demand and strict anti-virus controls in major Chinese cities having a clear negative bearing on the reported trading volumes. In fact, exports took a 9-percent year-on-year dive to $296.1 billion, worsening from October’s marginal decline. The downturn was even more severe than markets had forecast, with economists predicting a further period of declining export ts. On the same wavelength, imports fell sharply by 10.9 percent to $226.2 billion in November, down from the previous month’s 0.7-percent retreat. Amidst a monetary tightening in the US and the European continent, shipments to the US plummeted by 25.43 percent in November compared to the same period last year, while exports to the European Union fell by 10.62 percent year-on-year. Conversely, imports from Russia, mostly energy-related, rose 28 percent from a year earlier to $10.5 billion at the same time as exports to Russia were increasing by 18.5 percent to $7.7 billion.

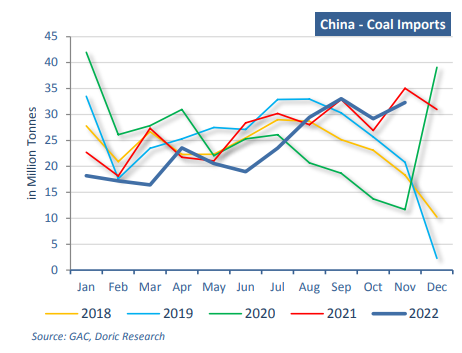

In the dry bulk spectrum, a rather mixed picture has become apparent. On the one hand, on a monthly basis, iron ore and coal imports reported strong gains. On the other hand, they are still remaining considerably lower year-on-year. Particularly, Chinese customs cleared 98.85 million tonnes of iron ore last month, up from an October reading of 94.98 million. However, November arrivals were 7.8 percent lower than the same month in 2021 and year-todate imports were 2.1 percent down. Symmetrically, coal imports also looked strong in November, rising to 32.3 million tonnes from October's 29.18 million. However, total imports for the first 11 months of the year dropped 10.1 percent compared to the same period last year. Soybean November imports fell 14 percent on the year to 7.35 million tonnes. After slower loading of shipments and longer customs clearance time, the softer number followed October's plunge in arrivals to just 4.1 million tonnes – the lowest level since 2014. For the first 11 months of the year, imports of the protein-rich beans were down 8.1 percent at 80.53 million tonnes, the data from the General Administration of Customs showed.

With the economic outlook coloured by various shades of grey and in the amidst of mass protests, China signalled a shift in its draconian Covid stance as it moves to ease some restrictions despite high daily case numbers. Yuan reached a three-month high early on Friday and Chinese stock markets rose as investors looked beyond poor data to growth prospects. There are early signs as well that steel mills are restocking iron ore ahead of an expected lift in demand in the new year. However, many analysts and business leaders expressed concerns, expecting Chinese economy to rebound only later next year as the path ahead might be rocky. In a similar vein, Dry Bulk Indices kept trading in a narrow range, bracing themselves for what the ill-famed first quarter will bring.

Data source: Doric