The Week

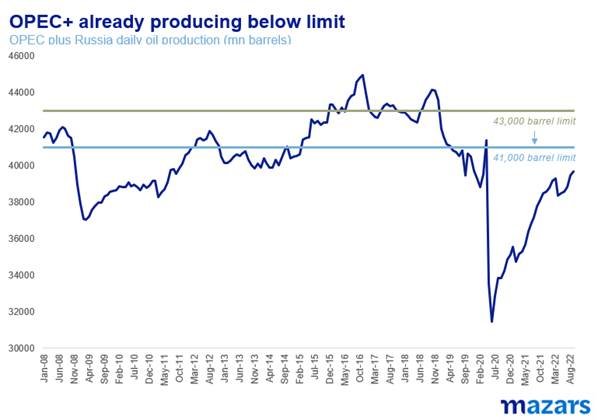

The global financial system is trying to cope with a series of exogenous shocks increasing in magnitude using internal tools. So far this has not been working. The shocks keep coming in and markets remain very volatile. Last week, OPEC+ announced a surprise decision to reduce oil production by 2m barrels per day.

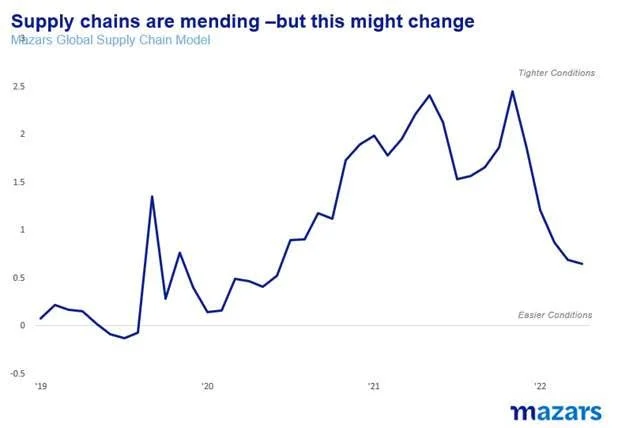

Just as global supply chains were mending, a surprise policy decision threatens yet higher transportation costs and could push the return to lower inflation levels further out.

The move itself is largely symbolic. OPEC+ was producing roughly 2m barrels under the quota anyway. Nevertheless, oil prices rose more than $12-$13 last week. What is more interesting is that Saudi Arabia, a staunch US ally, especially after 9/11, is now breaking with the White House administration, hiking prices at the pump, just a few days before the US Mid-Term election. This was a direct response to US plans to use the Dollar to curb the purchase price for Russian oil for any country or company that is connected with American businesses. Which is, mostly, everyone. Saudi Arabia is uncomfortable with the development of such tools, as, in the future, they could also be subject to such a policy.

This is just another example of a world that is completely unbalanced and in no way resembles the pre-pandemic norm. Policy makers respond to events and pressures in a piecemeal and often decentralised way. In essence, global policymaking has become something like out of Dostoevsky’s The Gambler (1866). Every response to every event causes global markets and economies to become further unbalanced, requiring even bolder action, causing even sharper events.

Recently this was evident in UK policymaking as well. The Conservative party had abandoned its tax-friendly principles in an attempt to balance the budget post-pandemic. This caused a voter backlash and a change in leadership. The new government performed a sharp U-turn, slashing taxes and attempting to rekindle growth with debt. The backlash came from markets this time and was probably more extreme than any new PM ever experienced.

And round it goes. Every decision, whichever way, causes further instability. Lack of decision may prolong governments, but it defeats the point of government itself.

Through the noise and the constant surprise, which now happen on a weekly basis, we can see the shifting background.

The United States, the global economic and financial leader, pursuing more nationalistic policies after a decade of retreating from its role as the ‘global police force’. As a result, global autocracy has been on the rise. America’s decision to weaponize the Dollar and the financial system against Russia is causing further instability amongst its allies.

China attempting to prevent businesses from taking hold of its larger economic agenda and, at the same time, retreating from its own role as the ‘global manufacturer’. As a result, global supply chains remain unbalanced and inflation persists.

European growth suffering from a monetary union that has been left politically and regulatorily unfinished.

And in the very background of it all, the reverberations from the 2008 Global Financial Crisis are still with us. They are causing consumers to be conservative and at the same time raging against a system that spent years funnelling trillions into financial markets, but keeping headline growth at sub-par levels, for fear of high inflation that came anyway.

Economic decisions, like the US trying to isolate Russia economically, have, in history caused much bigger trouble. Responding to an American embargo in oil, Japan in 1941 simply destroyed a large part of the American fleet in Pearl Harbor. In fact, war was usually humanity’s preferred way of solving things for aeons.

The world is increasingly unbalanced. It has been so since the Global Financial Crisis in 2008, and it was only accommodative policy making and debt that have helped growth, especially in developed nations.

We don’t see any immediate resolution to this. It is a time that history would have naturally wrought wars. Were it not for the nuclear deterrent, countries would have probably already vented their frustration in wider military conflicts. Devastation would be followed by reboot, a complete change in leaderships, debt erasure and a newfound appreciation for life, until the next war that is.

The destructive power of modern weapons simply prevents cycle from being played out, protracting instability and requiring solutions more erudite than simple domination. This is a new challenge for humanity. It is compelled to ignore its centuries-long instincts and think its way through problems rather than just bash enemies with a cudgel.

What it all means for investors

But how does this all affect investment portfolios? What can fund managers and private investors do to protect their wealth amidst instability we have not seen in generations? Other than being patient, there are a few simple rules which may help.

One: Focus on strategy. Acknowledge that tactical investing might yield less than in the past, as visibility is so low. Other than some quick trading ideas, tactical bets on portfolios will tend to have more random outcomes. It is the quality of the Strategic Asset Allocation and wider balance of assets that will guide returns for long-term portfolios. Moving closer to the benchmark does not mean lack of skill. Quite the opposite, it is a sanguine acknowledgment that the exact outcome of present events is unpredictable.

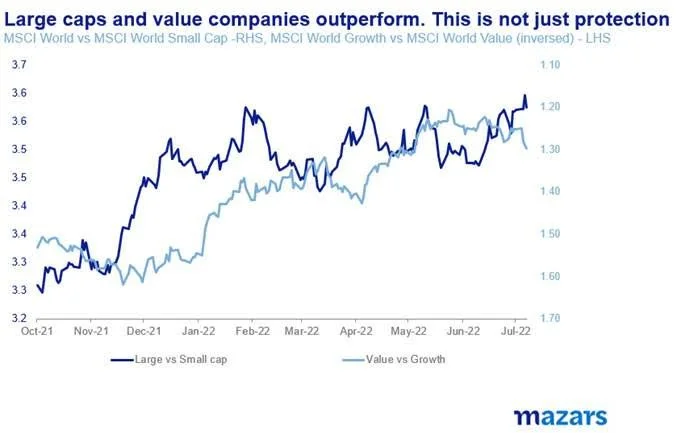

Two: Focus on fundamentals. This world will not feature a Yalta Conference or a Bretton-Woods, for the fate of nations and economic systems to be decided. These were post-war events, featuring the clear victors. Change, instead, will come from the bottom up. From companies compelled to find solutions for their shareholders. Investors need to identify those organisations better placed to solve supply chain problems, those that can cope with debt and those with the clout to adjust to the shifting sands will emerge as the possible winners. The rebound in Value and outperformance in large caps over the past few years are no accident.

Three: Ignore the noise. Despite it all, people prefer to live and thrive than destroy themselves. This is the time for clients to maintain close communications with their trusted advisers. The objective is to focus not on what might happen in the world, but what strategies are being deployed to protect individual wealth.