By Ulf Bergman

The year has so far seen seasonality taking an extended leave of absence across many sectors. The massive fiscal stimulus measures put in place in many parts of the world, especially in China, have altered the trading patterns usually seen for many industrial commodities and dry bulk shipping. For seaborne volumes and freight rates, a year is typically characterized by a weak first quarter followed by a gentle recovery during the second quarter and a stronger second half of the year. However, in the wake of the pandemic, the current year has not followed the first half of that narrative. The strong Chinese recovery, which began over a year ago, has maintained much of its strength during the first six months of the year and continued to feed a strong demand for commodities. While there are increasing signs of the Chinese economic growth plateauing, the economy is still expected to expand by a healthy six to eight per cent this year and will continue to contribute to the global demand for commodities. The accelerating recovery in other parts of the world, most notably in the US, has also contributed to the first half of the year failing to show much of the customary seasonality.

What does the crystal ball have to say about the second half of the year? As outlined above, under normal circumstances the demand for seaborne transportation and many commodities would be expected to increase in the coming months. While seasonality may not have featured in the earlier parts of the year, there is little to suggest that global demand for commodities will decline any time soon as many parts of the world continue on their paths towards economic recovery. Hence, there is a good chance that the traditional acceleration during the second half of the year will yet again materialise and provide commodity markets and dry bulk shipping with more to celebrate. The continued spread of the more contagious variants of the coronavirus could potentially put a spanner in the works, but with the continued rollout of vaccines, the likelihood for additional fullscale lockdowns is decreasing.

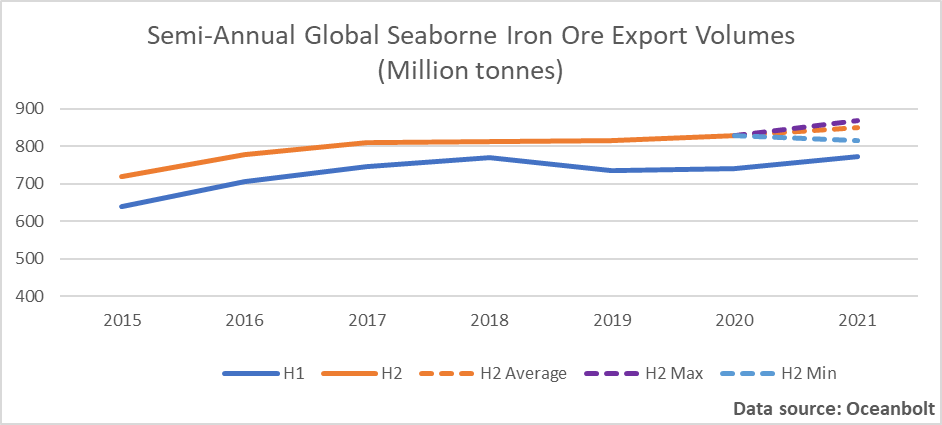

Iron ore has received much of the attention since China embarked on its post-COVID recovery, as the country’s seemingly insatiable appetite for the commodity pushed prices ever higher. Recent attempts by the Chinese authorities to control the soaring prices have to date only been modestly successful, with prices only marginally below the highs recorded in May. Rising global demand has offset much of the Chinese efforts and, according to some pundits, it is questionable if the price controls will have any long-term effect. According to data from Oceanbolt, the first six months of the year saw 772 million tonnes of iron ore shipped across the oceans, which is a record for the period. During the period 2015 to 2020 seaborne iron ore volumes were on average ten per cent higher during the second half of the year compared to the first half. Hence, it can be expected that the iron ore trade will continue to support the freight rates with increasing tonnage demand.

A simplistic approach to modelling the seaborne volumes for the coming six months, based on the seasonal effects during the previous years, suggests that between 815 and 869 million tonnes of iron ore will cross the oceans. While the volumes shipped during the first half were a new record, it is not guaranteed that the second half will follow suit. Needless to say, very little so far this year has been average and the seasonal effect for the coming six months may not fall in line with what has been observed previously. Assuming that the new coronavirus outbreaks can be controlled, the continued global economic recovery could see volumes surprising on the upside.

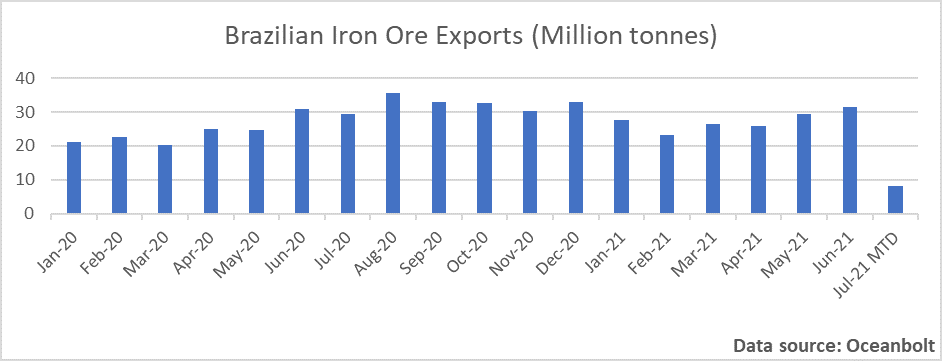

The increasing export volumes from Brazil in recent months suggest that the much-anticipated recovery for the country’s iron ore production is starting to gain some traction, after a long period of sub-par output levels. July has also started strongly, with around eight million tonnes exported during the first eight days and putting it on track of matching the previous months. The increasing Brazilian production is good news for the shipping sector, with China likely to buy most of it to reduce its reliance on Australian iron ore with increasing the tonne-mile demand as a result. At the same time as the Brazilian output has been on the increase, Australian export volumes declined in June compared to the same month a year ago suggesting that there is additional capacity available should global demand increase further.

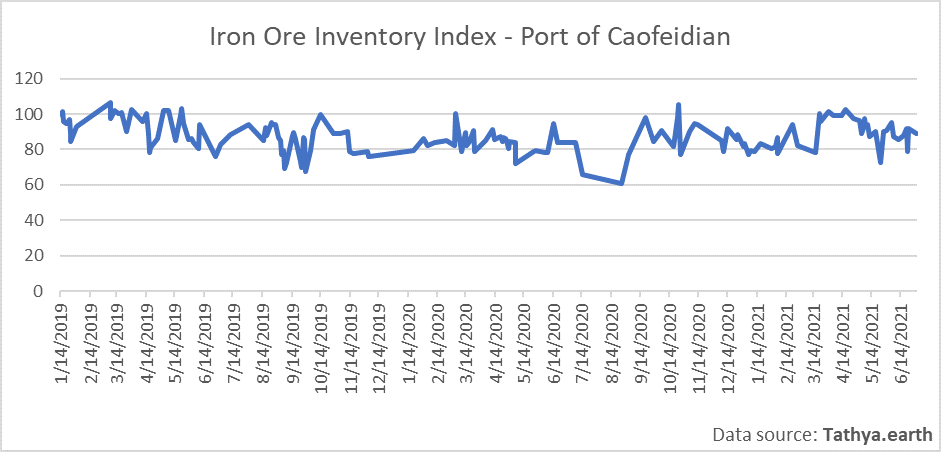

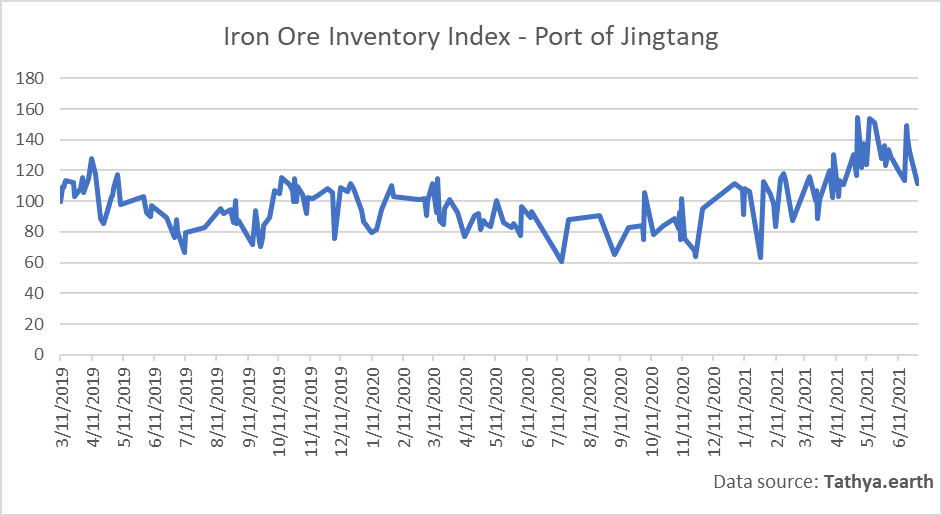

Adding to the bullish case for the second half of the year is the low inventory levels of iron ore in many Chinese ports. Data from Tathya.earth covering the two largest iron ore ports, Caofeidian and Jingtang, highlights the downward trajectory for the stockpiles. While the data is volatile by nature, the trend has been building since April/May for the two ports and could indicate that we will see increasing Chinese iron ore imports in the near future.