The summer of 2008 was a particularly odd period for shipping, let alone for the rest of the global economy. As the world was about to experience the first-ever Olympic Games in China and shipowners were gathering in Athens, Greece for the bi-annual Posidonia shipping conference, freight rates for both tankers and bulkers were hovering at stratospheric levels. Rumors about shipowners not even picking up their cell phones to talk to brokers about long term period deals that were “only” half the spot market, while freight futures were fluctuating by thousands of dollars every hour, provided a small testament to the impact that human sentiment can bring to financial markets and especially to the shipping market. Six months later, the shipping industry collapsed along the rest of the global economy, and numerous shipping related entities went under in a matter of weeks.

Then, China came to the rescue with a significant $600B+ infrastructure stimulus program that once again lifted dry bulk rates from rock bottom levels but by then it was too late. The shipping industry was already in a supply-driven recession that lasted most of the past decade and led to considerable struggles for most shipping firms around the globe.

Fast forward to today, and the summer of 2021 feels eerily similar to that of 2008. While stocks markets are reaching new highs daily, shipping is also back in the headlines, especially for containers where a monstrous supply squeeze has pushed freight costs to unimaginable for the industry levels. In commodity shipping, although rates are nowhere near the 2008 levels (tankers are actually in a mini depression by themselves with freight rates at or close to negative), for dry bulk, and especially for the sub-cape segments, conditions remain extremely favorable. Dry bulk rates hover at levels where cash flow generation is extremely high, returns on investment (even based on the highest asset prices of the past decade) are way above the cost of capital and sentiment is as positive as one can get.

The future is unknown and risks remain high, but forecasts are meant to provide more of a confidence judgement in future conditions based on known variables rather than a random prediction based on low probability unrelated outcomes.

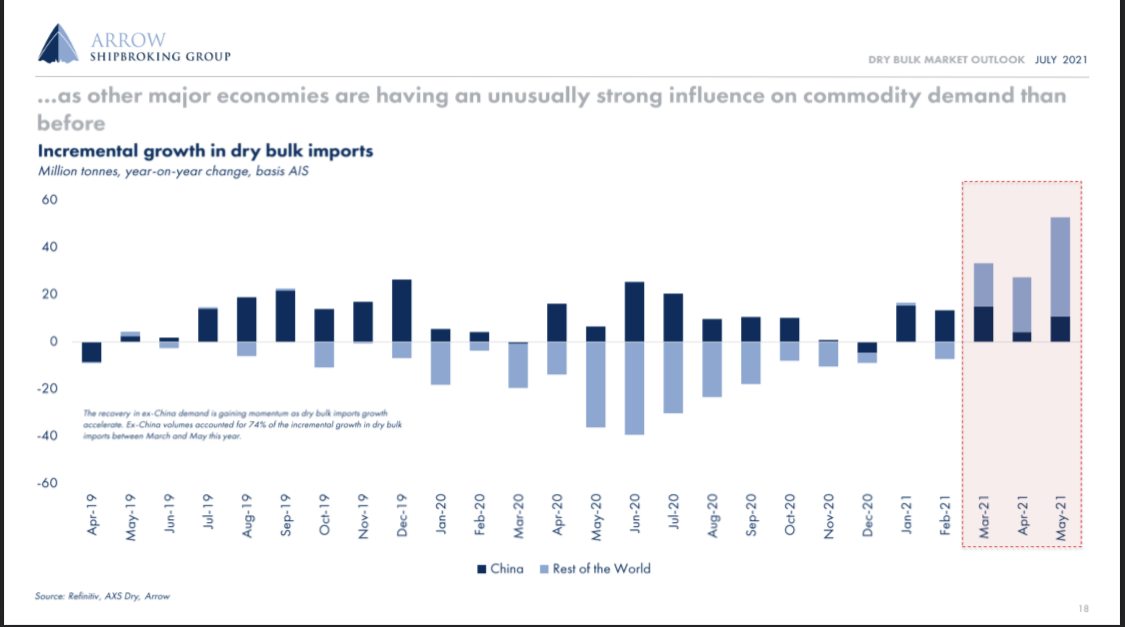

To that extent, it is easy to understand why dry bulk owners expect a bright future for the next 12-18 months. Seaborne trade has reached new record highs, surpassing even the 2019 previous peak. Although the rate of increase will naturally moderate from here as comparisons become less favorable (i.e. demand growth normalizes following the very weak levels of 2020), growth should remain stronger versus the pre-pandemic trend, aided mainly by minor bulks and coal. And this time around it is not only China. The rest of the world is thirsty for commodities and that is aiding shipping at its core. As the chart below shows, it is regions ex-China that is now the driving force behind commodity prices and shipping rates alike.

Source: Arrow Shipbrokering

How long will such strong demand growth lasts? Well, for one it is not difficult to argue about the cyclicality of commodities. As inventories rebuilt, demand will slowly ease, leading to a gradual turn of the cycle. Yet, the world is flooded with money, and government stimulus is still playing a major role in economic growth. Whether that trend has peaked or not is arguable, but as we stand today there are very few signs (ex-China at least, given that in China credit impulse is now pointing down, a bad omen for industrial activity) that such a trend is about to come to a halt. Thus, we expect for the next year demand to remain at above-trend levels, supporting commodity shipping.

Geopolitics has also been a major source of incremental tonne-mile demand and the Australia-China trade dispute has been front a center of such a trend. It is also the major force behind the very strong coal trading market this year, and as the chart below shows, trade routes are shifting to the benefit of dry bulk shipping.

Source: SSY

Then, there is the supply side. There, more secular fundamental trends are slowly shaping the industry and providing the base for a gradually tightening balance. 2022 will experience the slowest deliveries in many years, before a marginal increase in growth into 2023. Even with conservative assumptions about demolition despite scrap prices that are approaching record high levels of close to $600/ldt, fleet growth for the dry bulk fleet will drop below 2% next year (and likely be only just above 1%) a level that the industry has not seen in many decades.

It is easy to see why the industry is optimistic about the medium term. Assuming an average demand growth of around 3% (keep in mind, long term historical averages have been close to 5%) and supply growth of ~1,5%, utilization will continue to tick higher for the years to come. Throw on top of that inefficiencies (port delays, COVID-related slowdowns, etc.) and the upcoming emission-related potential speed reductions, and the dry bulk upcycle can easily extend for a few more years.

Source: Braemar ACM

The rate level that future demand and supply will clear is unknown. Yet, as we reach new highs year after year, owners build up their confidence and are naturally asking for more. Vessels that currently change hands at increased asset prices will require higher rates to achieve their targeted rates of return, and thus more resistance will be built over time during weaker freight rate periods. Overall, as market participants become more comfortable with elevated rates, the potential for significant spikes becomes real and increases the optionality of holding a shipping asset (either physical or paper).

Although the near term outlook appears softer (looking just a few weeks out we remain cautious) this is part of the natural volatility of the industry. We believe we are in the “summer lull” period, and as we approach early August, trade activity for forward September loadings will pick up, and with that, spot rates will once again turn higher.

After all, what makes shipping trading attractive is the embedded volatility, and traders and market participants alike should remain vigilant and ready to take advantage of such volatility while keeping in mind the broader trend of higher highs/higher lows that should remain with us for the foreseeable future.