By Ulf Bergman

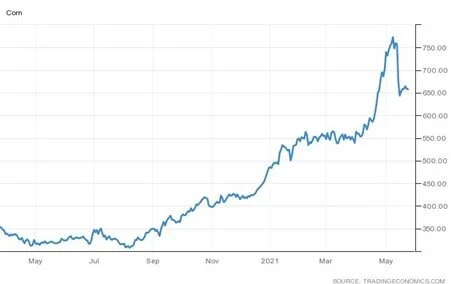

In the nine months between the middle of last August and the middle of May this year, the corn price was on an impressive trajectory and recorded an increase of close to 150 per cent when it hit an eight-year high two weeks ago. Since then, corn futures have dropped by around fifteen per cent, with investors losing some appetite for commodities following attempts by Chinese authorities to control surging commodity prices. Additionally, a recent report from the US Department of Agriculture (USDA) projected corn inventories to increase during the next agricultural marketing year, which begins in September. The forecast 250 million bushels increase, on the anticipated end of August levels of 1.26 billion bushels, during the 2021/22 year was above market expectations and contributed to the price correction. Likewise, soybeans retreated from their recent highs, albeit somewhat less dramatic, on higher harvest expectations for the recently planted crops following favorable weather forecasts for the US Midwest

Chicago Corn Futures – US Cents per Bushel

Despite the recent headlines that China has already sourced more than a third of the next agricultural marketing year’s expected corn imports from the US, the USDA is expecting US corn exports to face stiff competition from Argentina, Brazil, and Ukraine. The trio is expected to increase its combined exports by around 19.5 million metric tonnes in the coming year, which is expected to weigh on the US export volumes along with low inventory levels. However, the current poor weather conditions in Brazil’s major agricultural areas, with rainfall well below normal, could see yields dropping on the country’s second corn harvest and lend support to the volumes eventually shipped out of US ports. The USDA is anticipating China to import around 26 million tonnes of corn from its international suppliers during the year that begins in September, out of which 9.5 million tonnes have already been sourced from the US.

Perhaps a bit lost in the excitement over China’s recent buying spree of the coming US corn harvest, Ukraine reported that its farmers were nearing completion of the sowing process. The favourable weather conditions during the sowing season have led the county’s economy ministry to suggest that the grain harvest could reach at least 75 million tonnes this year, compared to the yield of 65 million tonnes last year. At the same time, Ukraine’s minister for agriculture, Roman Lyshchenko, suggested last week that the combined grain and oilseed harvests could reach 100 million tonnes during the year. A good harvest could further cement the nation’s position as the world’s second-largest grain exporter, after the US, a position it attained during the 2019/20 agricultural marketing year.

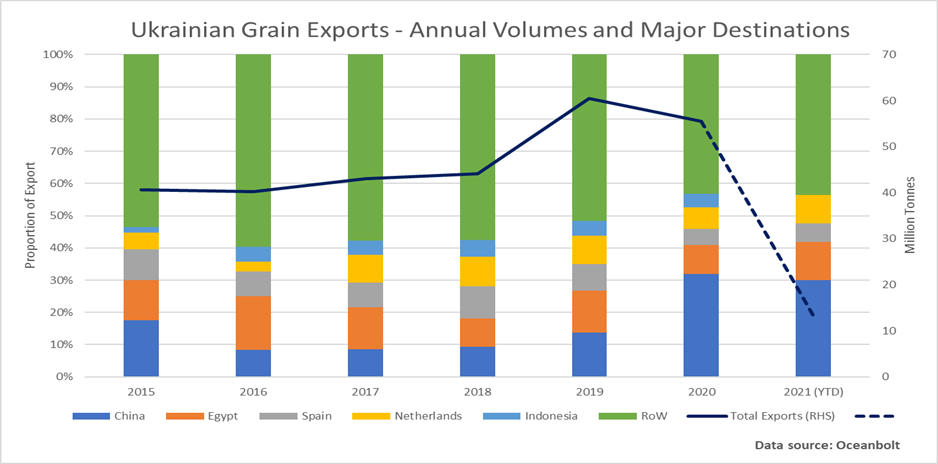

As Ukraine’s seaborne grain and oilseed exports have grown in recent years, the Chinese market has become increasingly important. According to data from Oceanbolt, Ukraine shipped 17.6 million tonnes to China last year, which was an increase of 113 per cent compared to 2019. A comparison with the preceding years provides even more impressive numbers. In the years prior to the sharp increase in export volumes to China, the destinations for Ukraine’s agricultural commodities were rather diverse without any market being dominant. However, last year and so far this year, grain shipments to China have accounted for approximately a third of the total seaborne exports, as the Asian nation has rebuilt its decimated hog herd.

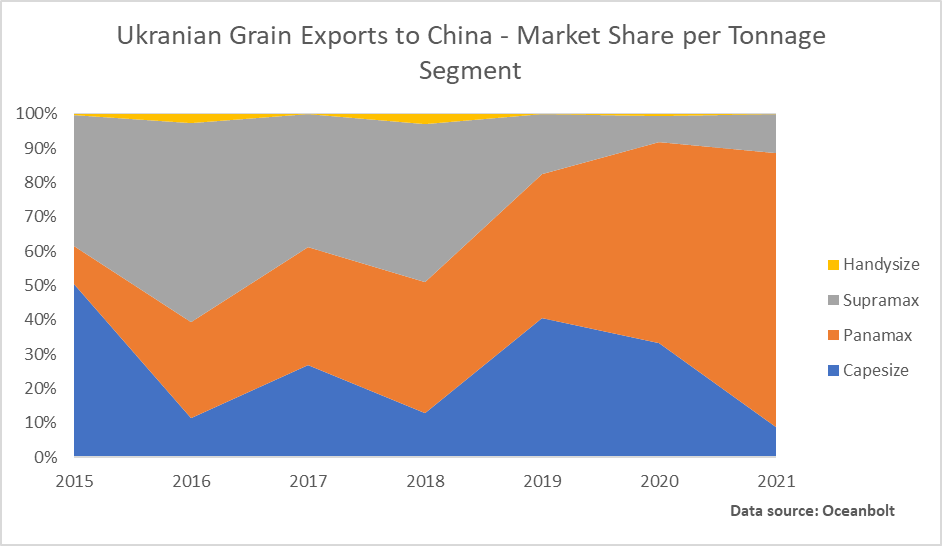

With the increasing flow of seaborne agricultural commodities from Ukraine to China, the nature of the trade has changed. The Panamax segment has become the tonnage of choice for many charterers and has edged out both Supramaxes and Capesizes, which previously handled large portions of the grain cargoes. While the evolution of the market shares may look dramatic, in absolute terms it is more a question of the Panamax segment growing while the volumes shipped on Supramaxes or Capesizes remaining fairly stable.

The retreating grain prices may be bad news for the farmers, but not necessarily for the dry bulk shipping sector. The demand outlook for grains and oilseeds remains solid, with the Chinese appetite unlikely to vanish anytime soon. The demand for livestock feed continues to surge and provides support for healthy seaborne volumes. The persistent strength of the container shipping sector is also likely to continue to drive many agricultural commodity consignments to the dry bulk sector, as a result of equipment shortage and high freight rates.