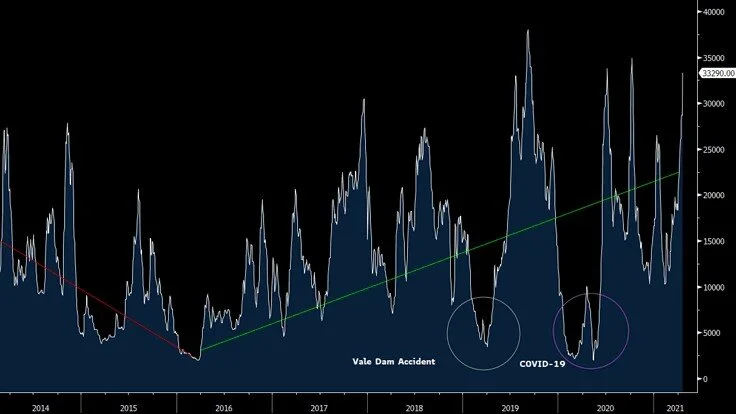

As the spot Capesize index propels past the 30,000 mark once again and the futures clearly pointing to this number pushing further over the next few weeks, the market seems quite skeptical of the recent rally keeping the futures close to spot and not getting overly excited about what’s next. This is not only understandable but also very welcomed. After all, buying futures at a steep contango is a dangerous game, especially as spot rates approach the high end of the historical range of the past decade. As always, views about the future are conflicting, but we believe there is a distinct disagreement over the direction of rates this time around that is unlike recent ones.

Capesize rates, Spot and 200 SMA; 2014-Present

The bullish camp is mainly focused on a broader reflation trade that is pushing commodities and economic growth higher as a result of the resumption of economic activity. Such a trend does not last weeks; rather, it is a longer term trend, and although one has always to remember that shipping is highly cyclical, such upturns last months, if not even years. The COVID-related downcycle was severe for most of the world ( ex-China) and now there is a combination of inventory rebuilding and real demand for bulk goods simultaneously boosting demand.

Such a push is coming on the back of record-high iron ore prices that have revived mining operations around the world, thus making the iron ore trade more diverse in terms of geographies. Such a trend also bodes well with China’s desire to diversify its commodities supply away from Australia as much as possible. With a higher dispersion of loading ports come higher tone-mile demand and less available tonnage at any give time, which also aids the strength of the current market. After all, if now there are a dozen parties competing for the same vessel, up from say half a dozen previously, even if the quantity of cargo is only marginally higher, the market “sees” more players chasing ships, thus adding more fuel (at least psychologically) to the current rally.

Then there is the camp that sees the current rally as temporary, fueled by sentiment on the back of a very strong activity in the sub-cape segments, something that will fizzle out soon. Such a view is supported by the main drivers of a rather dull Capesize market over the past few years, namely a relatively ample supply of vessels versus a low single digit growth in demand for such ships. Such a view is not necessarily wrong. The balance of the Capesize market has not changed dramatically (at least not yet). Iron ore exports are higher, but not meaningfully so, while coal trading is flattish so far this year, although the distance factor has changed due to the Australia-China trade dispute and the disruptions and lengthening of the average trip due to COVID-19 issues (see crew changes, port restrictions, etc.)

We think the reality lies somewhere in the middle. We believe there is a serious restocking cycle underway, mainly coming from ex-China consumers and producers. The logistical chain is a mess, not only in dry bulk but across shipping (see containers) and that is pushing the price of freight higher. New routes, longer waiting times and trip durations and a more diverse cargo base due to significant price differences (a great example is lumber prices across the world) are generating a very positive sentiment in the shipping cycles that is driving prices higher.

At the same time, a longer, slower trend is emerging that exacerbates the situation, albeit not to the extent that prices are pointing to. The fleet growth is slowing and will slow further in the next few years. This is a trend that will have a meaningful impact on the market balance, but understandably is not the reason for any movement in rates in the short term. Yet, with a gradually tightening market come higher lows and higher highs, and that should support the market for the years to come.

The tightening supply trend is not cyclical. It has to do with the broader, massive decarbonization trend that is affecting the global transportation markets, from passenger cars, to airplanes to ships. The efforts to reduce the carbon emissions will bring higher prices, not only for shipping but across the transportation chain, an inflationary trend that will also lead to higher freight prices. The rising cost affects not only the underlying fuel, but also the overall operations of a ship that makes it more expensive to run. Such a cost will inevitably pass to the charterer, or at least most of it, thus raising the cost of shipping over the next decade and beyond.

Do any of the above have any meangiful impact on the freight market over the next few months? Not necessarily. However, the shipping market clears through negotiating prices done by actual human beings. There is no electronic trading, computer screens, or algorithms in physical trading. That means sentiment and negotiating power tend to greatly affect prices. As owners sense the above trends, both short-term as well as longer ones, confidence increases even if the underlying drivers are not yet directly influencing the market balance.

The strength of the Capesize market feels well supported. Whether we get a correction or a further spike over the next few weeks is impossible to predict. However, the levels have clearly changed, and unless some major unexpected event comes, we support the view of higher lows/higher highs for the rest of the year.

Capesizes managed to climb above 30,000 without any significant effort. A positional tightness can propel rates much higher, and even if this is temporary, owner’s confidence will further increase, maintaining the never ending cycle of the current uptrend.